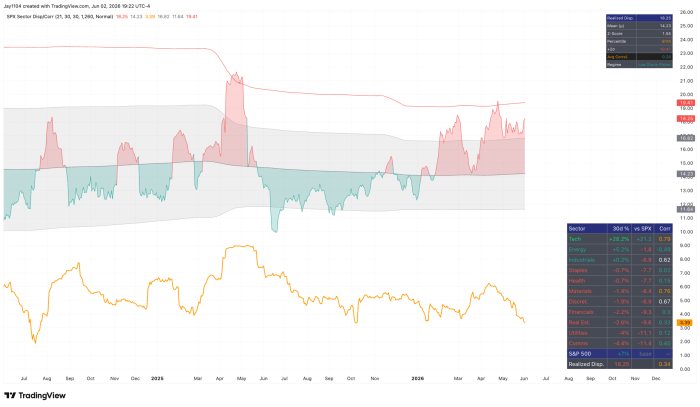

The S&P 500 finished slightly higher on the day, rising by around 13 bps. The index continues to churn beneath the surface, with semiconductors leading the charge. Over the last 30 trading days, the XLK ETF has outperformed the S&P 500 by 21.2%, while every other sector has lagged the index.

Of course, this is nothing new, as it has been the case since the March lows. However, I think it once again highlights the disparity within the index.

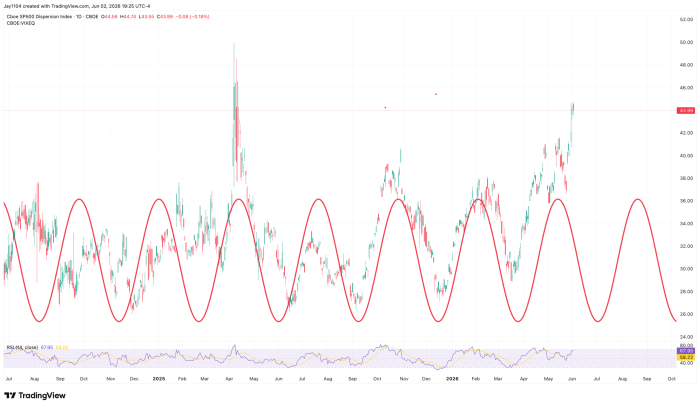

That is probably why the S&P 500 Dispersion Index is trading at levels not seen since the COVID crash and the tariff tantrum. However, the dispersion index declined slightly today. Given how elevated it has become, it seems well overdue for a rollover.

The decline in the dispersion index was driven by a drop in implied volatility across single stocks, as reflected in the VIXEQ. Even so, VIXEQ remains extremely elevated, and the spread between single-stock volatility and index volatility remains exceptionally wide.

In fact, that spread widened further today because the VIX fell more than the VIXEQ. Historically, these extreme divergences between single-stock and index volatility do not tend to persist for long and often retrace fairly quickly.

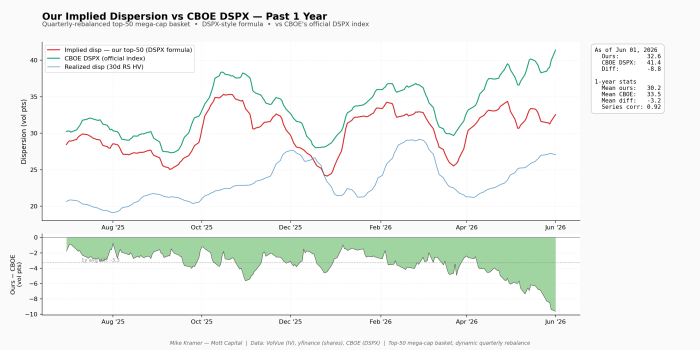

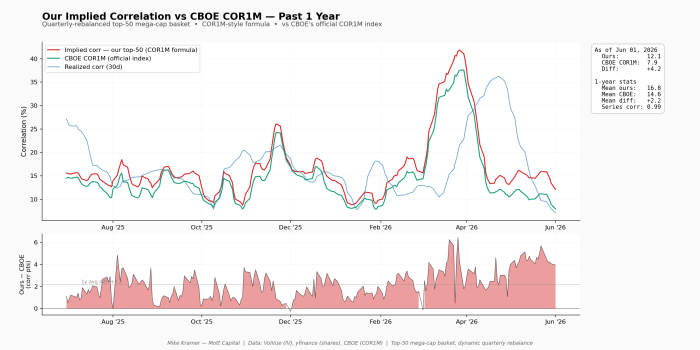

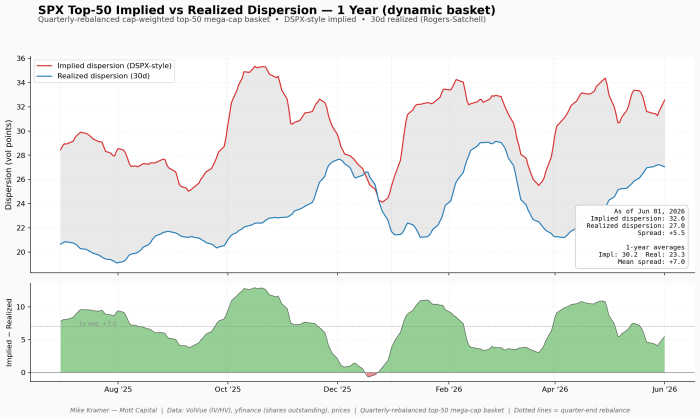

Maybe I have too much time on my hands, or maybe I just feel there is a point that needs to be proven. Whatever the case, I worked with Claude Code today to create my own dynamic implied correlation and implied dispersion indexes that can be measured against realized values for the top 50 stocks in the S&P 500. Both the correlation and dispersion proxy measures appear to track the official indexes fairly closely in terms of trend.

The CBOE dispersion index is actually curving higher than my measure at this point, but for the most part, the results look pretty solid.

Meanwhile, the 1-month implied correlation proxy also appears to track fairly well, although the actual reading is currently trending somewhat lower.

The point is that the one-year average dispersion spread is around 7 points, whereas today it is only about 5.5 points. As a result, implied dispersion is probably fairly valued, or perhaps even slightly cheap compared to realized.

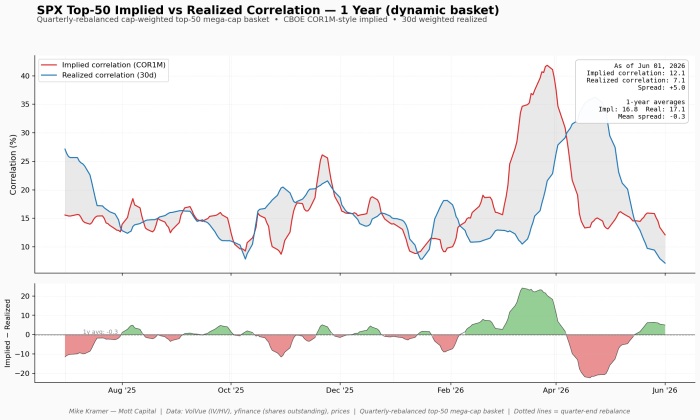

The spread between correlations is wider by +5 points than the average of around 0.3 over the past year. This is very wide when comparing implied versus realised, and implied is more expensive.

So, if I am thinking about this within the correct framework, the options market is pricing the current market environment appropriately with respect to dispersion. However, the concern appears to be around correlation snapping back higher, meaning stocks suddenly begin trading together again.

Generally, when stocks sell off sharply, correlations tend to rise as investors react to the same macro forces. In fact, a macro shock would likely drive index-level volatility higher, narrowing the gap between index and single-stock volatility and causing dispersion to decline.

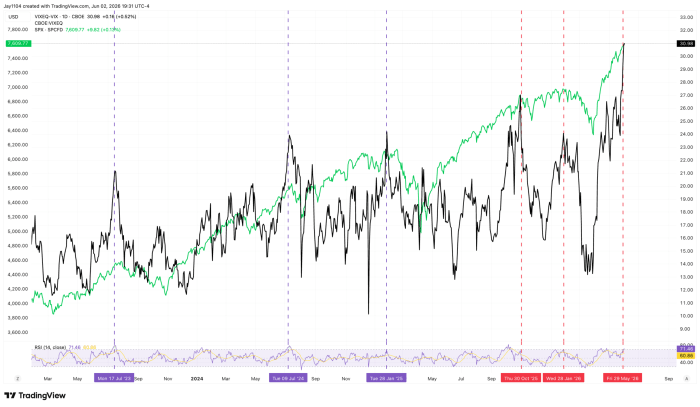

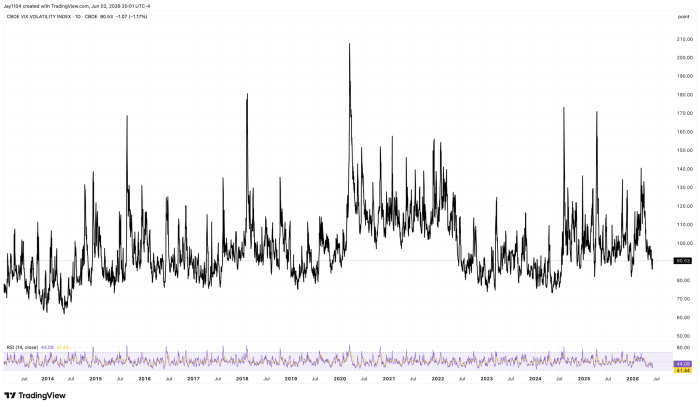

In essence, this suggests that index volatility remains relatively cheap. The VVIX at 90.5 is essentially sending the same message.

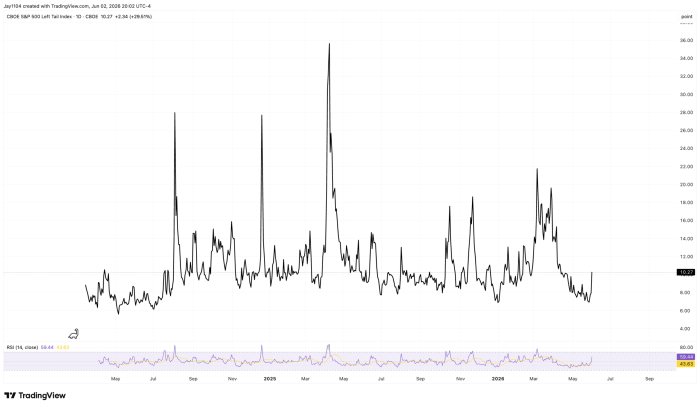

Someone is paying attention because today the Left Tail Index jumped 29% to 10.3.

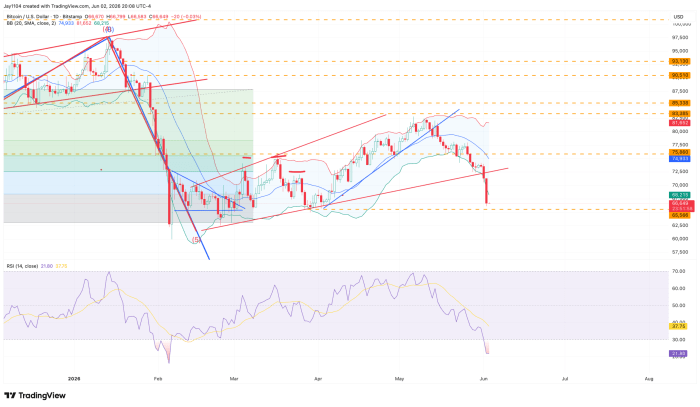

Today was a settlement day, and to no one’s surprise, Bitcoin (BTC.X) fell 6.5%. It likely has further downside for now, with more liquidity set to leave the market on Thursday. A break below support at $65,000 would likely push it beneath the February lows near $62,000.

Comments

Log in or sign up to join the conversation.