Oil Shock Deepens

The current market dynamic is being driven by two dominant forces that are overriding traditional cycles, namely the surge in capital directed toward artificial intelligence and the tightening of global oil supply linked to the conflict in Iran, with the former still providing enough support to keep US equities elevated even as the latter steadily builds inflation pressure beneath the surface.

Developments in the Strait of Hormuz remain central to the oil narrative, where President Donald Trump’s effort to offer safe passage to neutral shipping has coincided with renewed escalation, including missile strikes targeting the UAE, Oman, and vessels operating in the waterway.

Reports indicating that elements within the IRGC may have acted without full coordination from the Iranian government, and that Iranian President Pezeshkian has expressed strong opposition to those actions, highlight a fragmentation of command that complicates any path toward de-escalation. This lack of clarity around decision-making increases the risk premium embedded in oil markets, as it raises the probability of further uncoordinated actions that could disrupt supply or damage infrastructure.

At the same time, IRCG’s continued willingness to demonstrate its capacity to inflict damage suggests that it is not prepared to concede under pressure, leaving the United States facing a prolonged conflict scenario or a compromise outcome that may fall short of its strategic objectives.

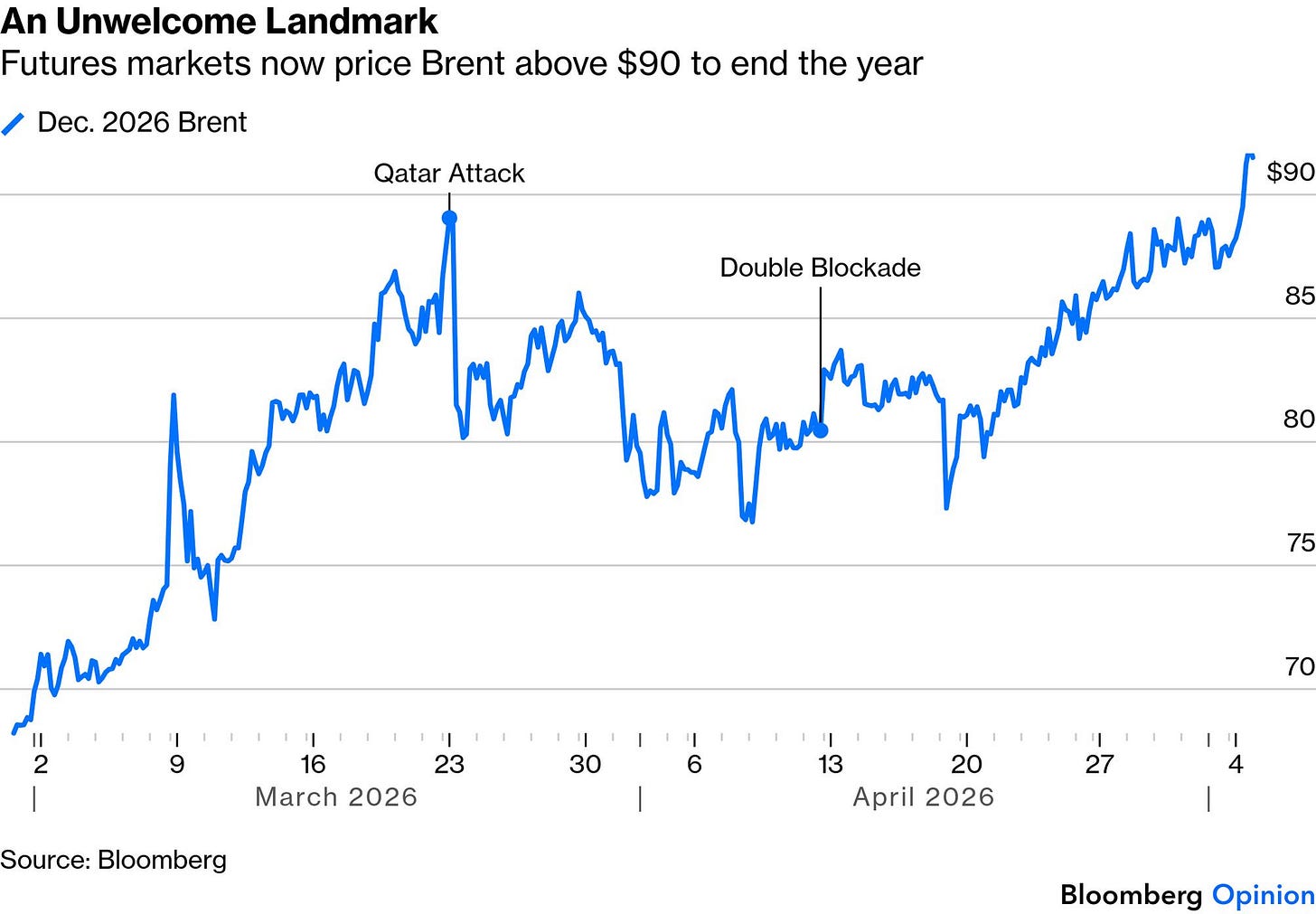

This evolving geopolitical backdrop is directly reflected in oil pricing, with Brent crude futures for year-end now trading above $90, surpassing previous highs reached earlier in the conflict and indicating that the market is increasingly pricing in a sustained disruption rather than a temporary shock.

The risk profile is further underscored by prediction market pricing, which now assigns a mere 40 percent probability that traffic through the Strait of Hormuz will return to normal by the end of June, a significant decline from roughly 90 percent just two weeks earlier. Indeed, the end of conflict optimism trade is no longer the default setting it once was, and the sense of enduring confidence that used to underpin market rallies is now far more fragile and conditional

The structure of the current oil market is drawing comparisons to the 2022 supply shock following Russia’s invasion of Ukraine, not because the events are identical, but because both represent supply-driven inflation impulses that are difficult to offset through monetary policy. In such environments, higher energy costs feed into production, transportation, and consumer prices more persistently, reinforcing inflation expectations over time.

That shift is now evident in rate markets, where the 10-year SOFR has risen to 4 percent, up from approximately 3.5 percent prior to the escalation in Iran. This move has been accompanied by a rise in 10-year breakeven inflation to around 2.5 percent, indicating that the increase in nominal yields is being driven primarily by higher inflation expectations rather than a change in real rates. The 4 percent level in the 10-year SOFR represents an important threshold for market participants, as it has historically marked the point at which discussions about receiving fixed rates become more active. Previous cycles saw peaks at progressively lower levels, including 4.6 percent, 4.4 percent, and 4.3 percent, suggesting a pattern of diminishing yield highs even as the market continues to test the upper range.

From a strategy perspective, the current environment presents a dual framework. In the near term, there is a rationale for positioning toward higher yields, as the combination of ongoing geopolitical uncertainty and rising inflation expectations suggests rates could continue to move modestly higher, with an additional 10 to 20 basis points plausible. This supports a tactical bias toward short-duration positioning. At the same time, the 4 percent level begins to offer an attractive entry point for longer-term strategies that involve receiving fixed rates, particularly if the expectation is that the Federal Reserve policy rate will average below this level over time. Historically, the federal funds rate has averaged closer to 3 percent over longer horizons, implying a positive carry opportunity for investors entering at current levels.

However, the outlook remains sensitive to further developments in the oil market. Continued escalation or evidence of sustained supply disruption would likely push inflation expectations higher, placing additional upward pressure on nominal yields. In a more extreme scenario, yields could rise toward 4.5 percent or higher, although such levels would likely prompt a policy response to stabilize financial conditions. Overall, the interaction between oil prices and inflation expectations is now the key driver of rates, with the 10-year SOFR acting as a barometer for how the market is pricing the persistence of the current supply shock.

Comments

Log in or sign up to join the conversation.