Introduction: The Paper Illusion vs. the Physical Reality

The oil markets possess an innate, historical tendency to overshoot to structural extremes before undergoing a violent turnaround, both on the upside and the downside. We are currently witnessing this exact psychological phenomenon play out in real time. Following a period where Brent and WTI crude peaked (on a closing basis) at the prominent psychological levels of $112 and $114 a barrel respectively, prices have undergone a precipitous, momentum-driven decline. Brent has collapsed more than 30% to $73 a barrel, accompanied by a symmetrical retreat in WTI down to $70 a barrel.

To the disciplined macro-observer, this aggressive sell-off reveals a profound, systemic disconnect between paper market participants and the unyielding realities of the physical oil complex. Paper traders appear to be operating under a naive, short-sighted assumption that the announcement of a peace framework means the regional crisis is permanently solved, the Strait of Hormuz will instantly reopen like a flipped light switch, and the global energy market will seamlessly revert to its pre-war status quo. Wall Street analysts have rapidly shifted their narratives, once again predicting a massive structural oil glut next year, perceiving the recent diplomatic headlines as the definitive end of the Middle East crisis.

In my opinion, this optimism is deeply flawed. A peace agreement is not a resolution; it is merely the starting line of a grueling, highly volatile, multi-month negotiation process. While speculative paper shorts push prices artificially low based on macro headlines, a forensic look underneath the surface reveals a stark reality: the developed world has entirely burned through its safety cushion of oil inventories and emergency reserves. The physical reality of the oil complex suggests that the market is severely underestimating the logistical lag in supply restoration and the sheer, unprecedented depth of the global inventory deficit. When these two forces collide later this year, the structural setup could lead to another aggressive, asymmetric spike in oil prices.

The Unprecedented Global Inventory Deficit

Headline oil prices are obscuring a more consequential development in the physical market. While financial positioning can influence short‑term price movements, inventories ultimately define the system’s resilience. By that measure, the global oil market is operating with materially reduced margin for error.

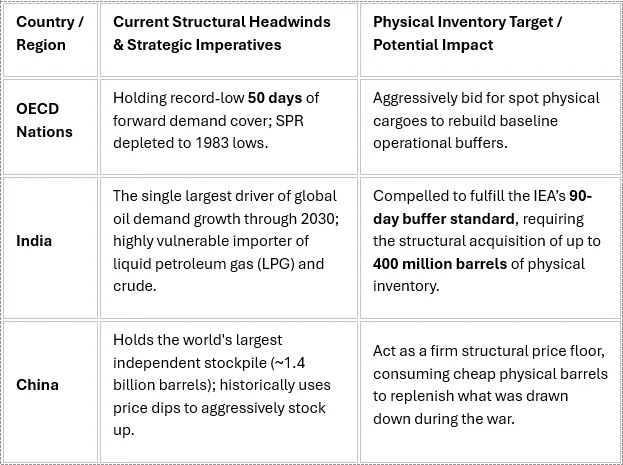

Prior to the conflict, OECD commercial inventories were expected to provide more than 70 days of forward demand cover. Since then, sustained drawdowns have compressed OECD coverage to roughly 50 days — near the lowest levels seen since the early 2000s.

A reduction of this magnitude meaningfully alters market structure. Lower inventory coverage weakens the system’s shock‑absorption capacity, increases sensitivity to incremental supply disruptions, and amplifies the potential impact of restocking cycles. The market is not broken — but it is tighter, more reactive, and more dependent on uninterrupted supply flows than headline prices alone might suggest.

The Domestic Anchors: SPR and Cushing at Critical Thresholds

Within the United States, the two primary storage buffers that dictate financial market pricing are flashing red.

The Strategic Petroleum Reserve (SPR): Following years of unprecedented releases utilized to combat inflation and geopolitical shocks, the federal strategic safety cushion sits at its lowest absolute level since 1983. I believe this means the government has effectively exhausted its capacity to intervene in the physical market to suppress future price spikes.

The Cushing Hub: Cushing, Oklahoma—the official physical delivery point for the NYMEX WTI futures contract—has seen its commercial inventories drained to a ten-year low. Historically, every single time Cushing inventories drop to the critical operational floor of 20 million barrels, the physical market panics due to systemic "tank bottoms" (the minimum volume required to keep pipelines and storage facilities functionally operating). This structural floor has consistently served as the launchpad for violent upward price squeeze events.

The Global Multi-Decade Deficit

The depletion of energy reserves is entirely symmetrical to what we are seeing at Cushing and the SPR, but it is occurring on a grand, macroeconomic scale. Since the outbreak of the war and the subsequent closure of the Strait of Hormuz, approximately 14 million barrels per day (mbd) of Gulf oil production were effectively cut off from global sea lanes due to active hostilities.

To bridge this colossal structural chasm, the world was forced to draw heavily from its land-based storage. Audited data from the International Energy Agency (IEA) reveals that global inventories suffered an astonishing daily drawdown of 6.3 million barrels per day throughout the duration of the conflict. The vast majority of this operational burden was borne by developed economies.

Consequently, total OECD land-based liquid fuel inventories are projected to plummet to just under 2.3 billion barrels. This does not merely represent a standard cyclical low; it marks the lowest absolute inventory level recorded since 2003, the very year comprehensive global energy tracking frameworks were instituted.

The True Metric of Danger: Days of Demand Cover

Absolute barrel counts can sometimes sound abstract, which is why sophisticated macro analysts prioritize Days of Demand Cover—a metric calculating exactly how long current stockpiles can sustain domestic consumption if external supply lines vanish completely.

Prior to the outbreak of the conflict, the EIA expected the OECD to maintain a comfortable, insulated cushion of over 70 days of forward supply.

For context, prior to the war, China held the world’s largest strategic and commercial crude stockpile at approximately 1.4 billion barrels—an immense cushion representing over three times the total strategic reserves of the United States.

The unrelenting physical drawdowns forced by the war have systematically crushed OECD coverage down to exactly 50 days.

In my opinion, the developed world has now depleted its entire economic safety margin. Even under an optimistic scenario featuring a phased, peaceful reopening of regional chokepoints, global refiners may find themselves with zero operational buffers. They may be forced to enter the physical spot market simultaneously, competing aggressively and bidding up prices simply to restock these depleted, 2003-era inventory troughs.

The Physical Logistics Catch-22: Mines & Marine Lag

The paper market currently treats the signing of a diplomatic peace framework as if it possesses the magical ability to instantly materialize physical crude oil at refineries in Western Europe, Asia, and the U.S. Gulf Coast. In the harsh reality of maritime logistics and oilfield engineering, a physical chokepoint cannot be flipped on like a light switch. The normalization of energy flows faces an immediate, multi-month logistical bottleneck.

The Maritime Security and Insurance Bottleneck

Before a single commercial vessel can safely transit the Strait of Hormuz, international naval coalitions face a massive, non-negotiable operational hurdle: mine clearance and maritime security recertification. The waterway will require significant time for intensive naval mine sweeping, debris clearing, and hydrographic mapping to ensure that modern commercial shipping lanes are entirely free of explosive hazards.

Furthermore, international maritime insurance syndicates (such as Lloyd’s of London) operate on cold actuarial data, not political optimism. Insurers will likely completely refuse to write hull and machinery or protection and indemnity (P&I) policies for Suezmax and Very Large Crude Carrier (VLCC) multimillion-barrel supertankers until the waterway is formally certified as safe. Even once the initial ships pass through, war-risk insurance premiums may remain prohibitively high, adding a structural cost layer to every single physical barrel moved out of the Gulf.

The Infrastructure Ramp-Up Lag

The IEA has explicitly pointed out that even as the Strait incrementally reopens to traffic, ramping commercial transit back up to its pre-conflict baseline of 15 mbd will face an extended timeline. This operational friction is compounded by upstream realities: shut-in production wells across the major Gulf states cannot instantly restore flows without technical delays.

When an oil well is shut in or choked back for an extended period due to conflict, operators frequently encounter reservoir pressure changes, mechanical failures, and downhole scaling. Safely restarting and stabilizing these fields to pre-war output capacities likely requires weeks of engineering work. Consequently, the actual volume of physical crude arriving at global discharge ports may severely lag Wall Street's paper expectations until late this year or early next year.

The Coiled Spring of Pent-Up Demand

The extreme, war-induced price spikes experienced over the past year forced an intense wave of economic demand destruction. High prices and physical fuel scarcity coerced governments across Asia to restrict commercial operating hours, forced heavy industries to curtail production, and caused international airlines to radically alter and lengthen their intercontinental flight paths to avoid conflict zones. The IEA formally documented a temporary contraction in global oil demand of over 1 million barrels per day directly attributable to these extreme pricing pain points.

However, demand destruction caused by artificial geopolitical supply shocks is highly elastic. The moment the paper market drags crude prices down into the low $70s, it could uncoil a massive spring of pent-up economic activity, particularly as the global market moves into peak seasonal travel.

The Global Race to Build Strategic Buffers

The market is entirely failing to account for a new, powerful class of physical buyers entering the market: sovereign nations seeking to insulate themselves from the next crisis. The Iran war has triggered a global race to build oil reserves, the import-dependent countries that paid the highest economic price during the shipping closures are actively shifting their inventory policies. The old "just-in-time" supply chain philosophy is dead; it is being replaced by an aggressive policy of structural hoarding.

This impending structural restocking demand could hit the global market at the exact same time that ordinary consumer travel demand snaps back, creating a powerful, compounding demand shock against an inelastic supply curve.

Technical Fragility of the Peace Framework

The prevailing narrative on trading desks seems to be that regional stability has been permanently achieved. In reality, the actual text of the agreement reveals extreme technical fragility. The market has priced in a comprehensive, permanent peace treaty, when the actual diplomatic document is merely a temporary, 60-day general waiver designed to establish a brief window for final-status negotiations.

The Structural Barriers to a Permanent Treaty

The historical reality of this conflict suggests that an enduring, frictionless diplomatic resolution is highly improbable. There is no modern precedent for a formal bilateral treaty between these primary combatants:

The Post-1979 Paradigm: Following the 1979 Islamic Revolution, the Iranian regime systematically reversed its pre-1979 posture. Under the Shah, Iran and Israel had maintained close, mutually beneficial, and highly covert diplomatic, economic, and military ties via the "Periphery Doctrine."

The Ideological Non-Starter: Post-1979, Tehran officially withdrew its recognition of Israel as a sovereign state, structurally defining it as an occupied territory. Because Iran’s constitutional state apparatus rejects the very legitimacy of Israel's statehood, a formal, bilateral peace negotiation has historically been treated as an ideological non-starter by Tehran.

The Zero-Buffer Market

The conflict has historically operated as an entrenched, decades-long proxy struggle interspersed with direct military exchanges. This fundamental dynamic has not changed. Recent diplomatic headlines highlighting friction—such as direct warnings from Washington to Jerusalem regarding continued escalations with Hezbollah in southern Lebanon—have already triggered sharp, intra-day price spikes.

The core takeaway is that the underlying geopolitical tinderbox remains entirely intact. Because the paper market has aggressively sold off and completely erased the geopolitical risk premium from the price of oil, it has seemingly left itself with absolutely zero margin for error. In a physical market that possesses an extremely low-inventory cushion and an OECD stock level scraping 2003 bottoms, any asymmetric proxy attack, any violation of the 60-day waiver, or any breakdown in diplomatic talks could instantly re-ignite a violent premium, forcing short-sellers to panic-buy a market completely devoid of physical liquidity.

Conclusion & Investment Implications

The current macro environment presents a textbook example of a market pricing the headline while completely ignoring the underlying plumbing. The paper markets seem to be valuing oil as if a structural supply glut is locked in, when in fact, the physical oil complex is running on empty. A fragile, 60-day diplomatic waiver cannot magically replenish an international inventory deficit that took a multi-nation war to create, nor can it bypass the rigid laws of maritime logistics. As global refiners are forced to step into the spot market to restock depleted 50-day OECD inventories, they may find that the physical oil simply isn't there yet due to the severe transit lag out of the Gulf. The risk/reward profile heavily favors a structural, "higher-for-longer" outlook in energy prices.

Portfolio & Tactical Allocation Approach

In the portfolio I manage, my focus is on financially strong energy companies that should benefit when prices remain at elevated levels. When supply becomes tight and demand increases, these companies are often in a good position to generate stronger cash flow. At the same time, I carefully size each investment so that no single position takes on too much risk within the overall portfolio.

I also invest selectively in companies that own and operate energy infrastructure, such as storage facilities and transportation networks. These assets play an important role in the energy supply chain and can provide steady revenue, even when markets are volatile.

In addition, I maintain exposure to precious metals and certain critical minerals as part of a broader diversification strategy. These investments can help provide balance during periods of economic or geopolitical uncertainty.

Finally, I avoid trying to chase short-term price swings in volatile commodity markets. Instead of attempting to predict day-to-day movements, I focus on long-term fundamentals, thoughtful position sizing, and risk management to help pursue sustainable results over time.

Comments

Log in or sign up to join the conversation.