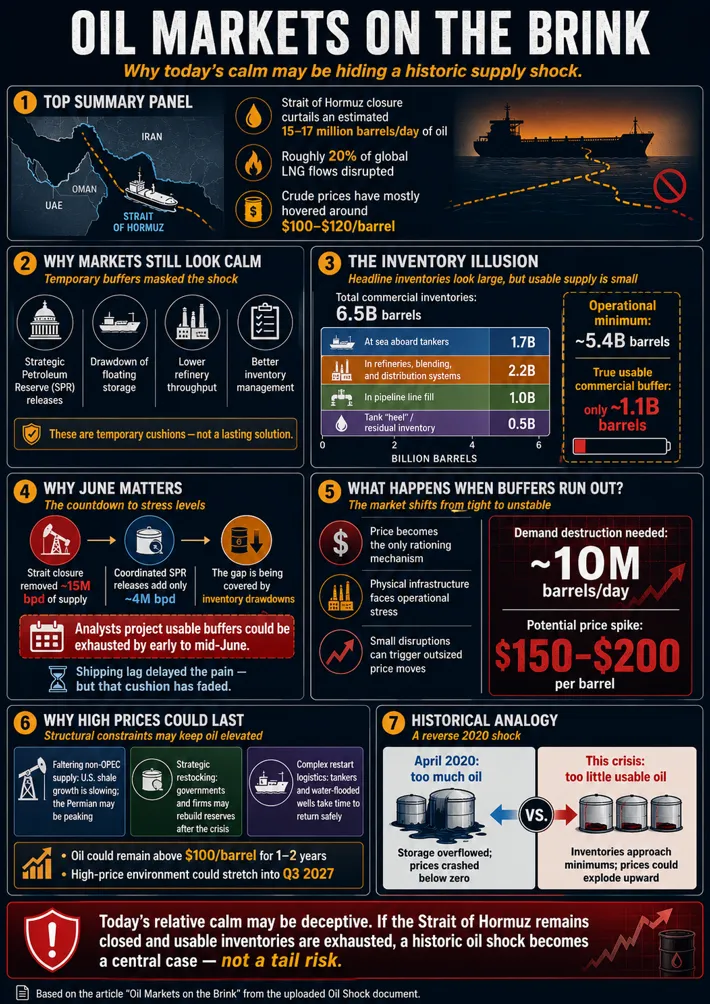

Global energy markets appear relatively calm on the surface, but that calm may be misleading. Despite the ongoing closure of the Strait of Hormuz, which has reportedly curtailed an estimated 15 to 17 million barrels per day of oil supply and disrupted roughly 20% of global liquefied natural gas flows, crude oil prices have largely remained in the $100 to $120 per barrel range. At first glance, markets seem to be treating the crisis as temporary, assuming the Strait will reopen soon and global supply will quickly normalize.

That assumption may prove dangerously optimistic.

The current price stability has not come from a healthy supply-demand balance. Instead, it has been supported by temporary emergency buffers, including coordinated releases from Strategic Petroleum Reserves, the drawdown of floating storage, reduced refinery throughput, and improved inventory management. These measures have delayed the full impact of the supply disruption, but they have not solved it.

The central concern is that these buffers are now being exhausted. Analysts estimate that global commercial oil inventories are rapidly falling toward the minimum level required to keep the petroleum system functioning. Once inventories approach that operational floor, the market may no longer be able to absorb the shortage through stockpile drawdowns. At that point, price becomes the primary mechanism for rationing demand.

Why the Market Has Not Fully Reacted Yet

When the Strait of Hormuz first closed, the full effect was not immediately visible because of what analysts describe as a “shipping lag.” Tankers that had already departed the Persian Gulf before the closure continued traveling to their destinations. These vessels took several weeks to arrive, which temporarily masked the physical supply loss.

By mid-April, however, those last pre-closure cargoes had largely arrived. Since then, ports and refineries have increasingly relied on domestic inventories and emergency reserves. This has created the appearance of stability while the underlying inventory cushion has steadily deteriorated.

Another reason the market may be misreading the situation is the way global inventories are reported. Headline commercial stockpile figures may suggest that the world has ample oil available, but much of that oil is not truly usable surplus. A large portion must remain in the system simply to keep tankers, pipelines, refineries, blending facilities, and storage tanks operating properly.

According to the estimates in the source material, the world began the crisis with approximately 6.5 billion barrels of non-SPR commercial inventory. However, roughly 5.4 billion barrels of that total may be required as operational inventory. This includes oil needed at sea, in refinery and distribution systems, in pipelines, and as residual “heel” inventory at the bottom of storage tanks. That leaves only about 1.1 billion barrels of truly usable commercial buffer.

Why June Is Critical

The math becomes increasingly severe if the Strait remains closed. The source material estimates that the closure has removed roughly 15 million barrels per day from the market. Even with emergency SPR releases contributing around 4 million barrels per day, the world is still facing a major daily deficit.

That shortfall is being covered by drawing down commercial inventories. If the drawdown continues at the current pace, analysts expect usable buffers to be depleted by early to mid-June. Once that happens, the petroleum system moves from a tight market into a potentially unstable one.

The key issue is that oil markets do not become stressed in a smooth, linear fashion. As inventories approach operational minimums, small disruptions can produce outsized price effects. Refiners, distributors, airlines, trucking companies, and industrial users all compete for barrels that are no longer readily available. When physical supply is insufficient, prices must rise high enough to force demand destruction.

Demand Destruction and the Risk of $150 to $200 Oil

To balance the market, analysts estimate that roughly 10 million barrels per day of global oil demand may need to be eliminated. That kind of demand destruction is difficult to achieve without a severe price shock.

The source material projects that crude prices may need to rise to the $150 to $200 per barrel range to force the necessary reduction in consumption. At those levels, energy costs become punitive enough to affect consumer driving behavior, airline operations, industrial activity, and broader economic demand.

This would not simply be a financial-market event. It would be a physical supply crisis. When inventories fall too low, pipelines and refineries can struggle to operate efficiently because they require minimum volumes and pressure to function. The risk is not just higher prices, but operational stress across the entire petroleum system.

A Mirror Image of April 2020

Analysts compare the current risk to the oil market collapse of April 2020, but in reverse. During the COVID-19 lockdowns, demand collapsed and storage filled rapidly. With nowhere to put excess crude, prices briefly plunged below zero.

In the current scenario, the bottleneck would occur in the opposite direction. Instead of too much oil with nowhere to store it, the market could face too little usable oil to keep the system running normally. If that happens, prices could spike violently upward as buyers compete for scarce physical barrels.

Structural Problems Could Keep Prices High

Even if the Strait of Hormuz reopens, the crisis may not end immediately. Several structural constraints could keep oil prices elevated for an extended period.

First, non-OPEC supply growth appears increasingly fragile. The U.S. shale boom, which supplied much of the world’s non-OPEC growth over the past 15 years, is showing signs of slowing. Production growth has stalled across several major shale basins, and the Permian Basin may be approaching a peak.

Second, governments and corporations are likely to reassess their strategic stockpile policies. If the crisis exposes serious vulnerabilities in energy security, many countries may rush to rebuild or expand Strategic Petroleum Reserves once supply routes reopen. That rebuilding process would add persistent demand to the market.

Third, restarting disrupted production is not instantaneous. Even after a peace agreement or reopening of the Strait, empty tankers would need time to return to the Gulf. Some oil fields, particularly complex water-flooded wells in countries such as Kuwait and Iraq, could take weeks or months to restart safely.

Because of these factors, analysts forecast that oil prices could remain above $100 per barrel for one to two years, with elevated conditions potentially lasting into the third quarter of 2027.

The Bottom Line

The oil market’s current calm may be deceptive. Prices around $100 to $120 per barrel suggest that traders still expect a temporary disruption followed by a rapid return to normal. But the physical market may be telling a different story.

If the Strait of Hormuz remains closed into June, the world’s usable commercial inventory buffer could be exhausted. Once that happens, emergency reserves and logistical workarounds may no longer be enough. Price would become the only remaining tool to ration demand.

The result could be a historic oil shock, with crude prices potentially surging to $150 to $200 per barrel. More importantly, the crisis could expose deeper structural weaknesses in global energy supply that persist long after the immediate geopolitical event is resolved.

We reduced our energy exposure early in the Iran war because we did not expect the conflict, or the closure of the Strait of Hormuz, to last as long as it has. The prolonged disruption has likely extended the period of elevated energy prices well into next year, materially changing the economics for energy companies. As a result, we have begun rebuilding energy exposure in client portfolios and expect to continue doing so in the coming weeks.

Comments

Log in or sign up to join the conversation.