The S&P 500 fell by roughly 40 bps on the day, which seems like a relatively mild reaction to the spike in rates and oil prices amid renewed tensions in the Persian Gulf. WTI finished the day higher by 2.6% to close above $105, while Brent crude rose by more than 4% to finish near $114.

At least on a rolling generic price chart, Brent appears to be nearing what could be a major breakout from an extension of a falling wedge, or potentially a large bull pennant pattern. A move above $114 would likely signal that something more significant is unfolding, and with the RSI at just 63, there is still room for prices to move higher without becoming overbought.

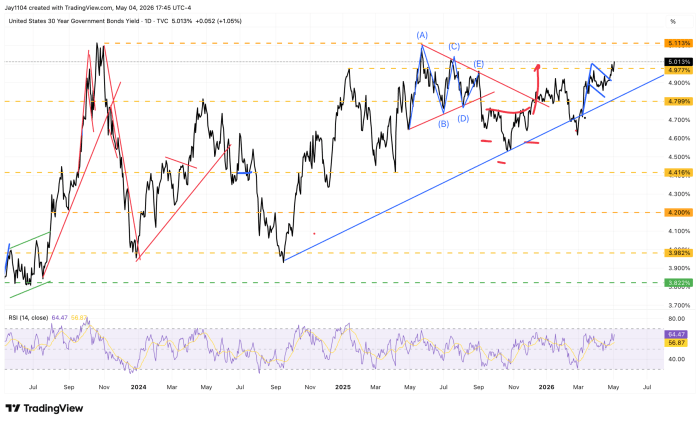

Today, the 30-year Treasury yield closed above 5% for the first time since July, suggesting that the breakout in the long end is beginning to take hold. The RSI is only around 65 and, like oil, still has room to move higher, potentially allowing yields to challenge the highs seen in the fall of 2023.

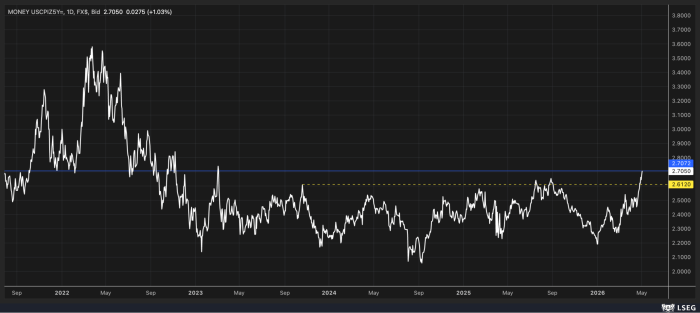

Additionally, the 5-year CPI swap rose to 2.7% today, closing at its highest level since March 2023. Ultimately, this helps explain why rates are moving higher, and if inflation expectations continue to rise, they are likely to push rates even higher over time.

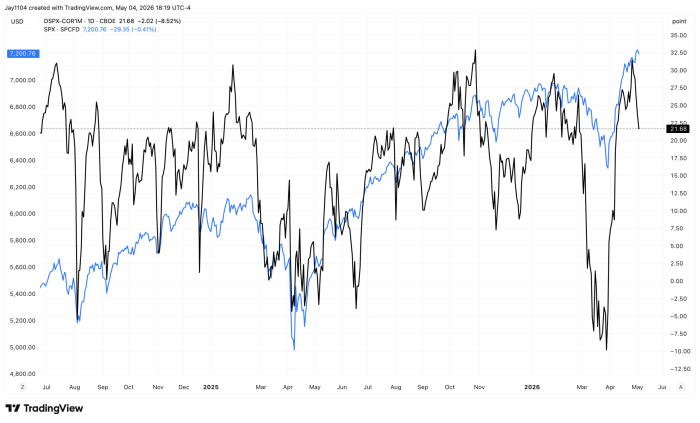

Equity prices are unlikely to sustain recent gains if oil prices continue to rise, particularly as the dispersion unwind plays out. The dispersion index minus the 3-month implied correlation index declined again on the day, as implied correlations moved higher. This is all part of the post-earnings volatility dispersion unwind, which should continue over the coming weeks.

Finally, the Treasury released its borrowing estimates today and is now looking to raise $189 billion for the remainder of this quarter, $79 billion more than previously projected, assuming a TGA balance of $900 billion. Meanwhile, for the September quarter, it expects to borrow $671 billion, assuming a TGA of $950 billion.

The increase in the TGA was somewhat surprising, as were the borrowing estimates for the remainder of this quarter. It would not be surprising if borrowing needs for next quarter are revised higher in due course, but that remains to be seen.

The settlement calendar should begin to shift back toward bill net new issuance, with supply likely to increase next week.

Comments

Log in or sign up to join the conversation.