Nowcast from Atlanta Fed plus tracking from GS out today.

(Click on image to enlarge)

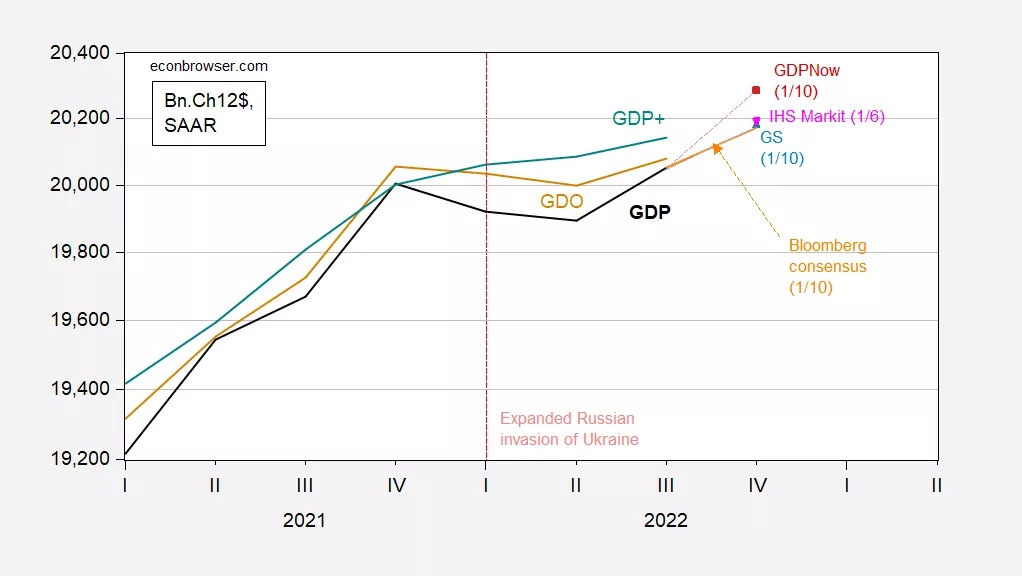

Figure 2: GDP (bold black), GDO (tan), GDP+ (green), GDPNow for Q4 (red square), Goldman Sachs (sky blue triangle), IHS Markit (inverted pink triangle), Bloomberg consensus as of 1/10 (orange line), all in billions Ch.2012$, SAAR. GDP+ level calculated by iterating on 2019Q4 GDP (when GDP and GDO matched). Source: BEA (Q4 3rd release), Federal Reserve Bank of Philadelphia (12/22), Federal Reserve Bank of Atlanta (1/10), Goldman Sachs (1/10), IHS Markit (1/6), Bloomberg, and author’s calculations.

GDPNow is substantially higher (4.1%) vs Bloomberg consensus (2.4%), as well as recent readings from Goldman Sachs and IHS Markit.

IHS Markit/S&P Global view as of 1/6 [not online]:

Despite solid headline growth in the fourth quarter, according to our estimate, the narrative of our near-term outlook for the US is still one of mild recession beginning in the first quarter of 2023, with a peak-to-trough decline in GDP of 0.6%.

Mark Zandi(Moody’s) and Heather Boushey (CEA) have indicated that a “soft-landing” is possible, while Jan Hatzius has in the past indicated a likely soft landing, which he interpreted as more likely given the employment situation release for December.

More By This Author:

How Far Off Is the Establishment Survey Nonfarm Payroll Employment Series?The Jobs Worker Gap In November

ADP Release, And The Flat Employment Growth In Q2 Thesis

Comments

Log in or sign up to join the conversation.