Sates are down. Inventory is high and rising, pressuring builders.

The Census Department New Residential Construction report for May 2026 is another homebuilder disaster.

New Home Sales

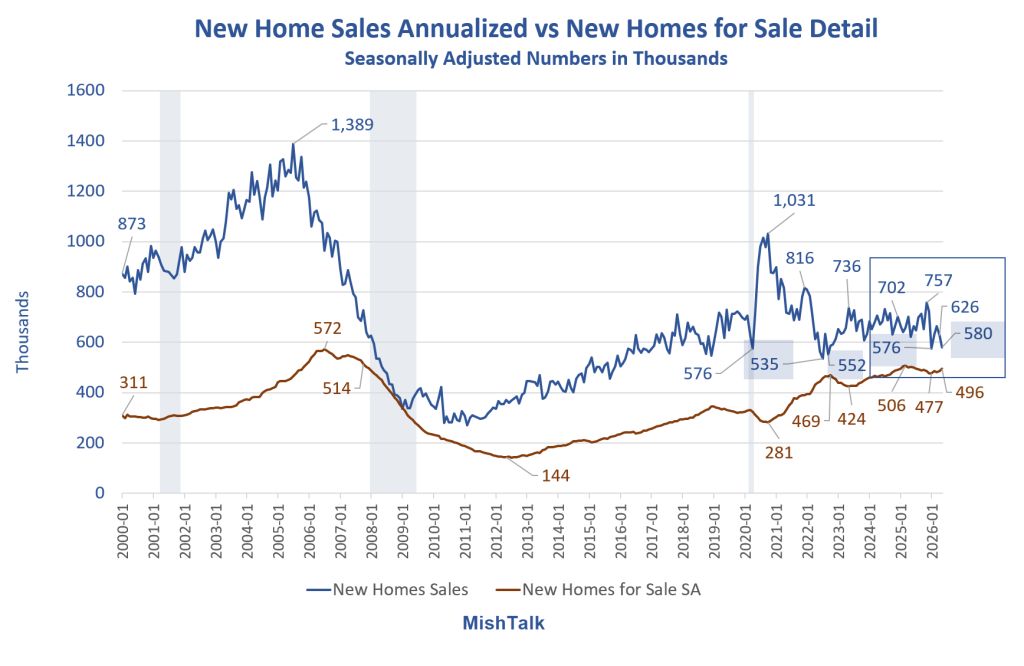

Sales of new single-family houses in May 2026 were at a seasonally-adjusted annual rate of 580,000

This is 7.3 percent (±13.3 percent) below the April 2026 rate of 626,000, and is 6.8 percent (±12.8 percent) below the May 2025 rate of 622,000.

For Sale Inventory and Months’ Supply

The seasonally-adjusted estimate of new houses for sale at the end of May 2026 was 496,000.

This is 2.3 percent (±1.2 percent) above the April 2026 estimate of 485,000, and is 1.4 percent (±3.3 percent) below the May 2025 estimate of 503,000.

This represents a supply of 10.3 months at the current sales rate. The months’ supply is 10.8 percent (±19.2 percent) above the April 2026 estimate of 9.3 months, and is 6.2 percent (±15.4 percent) above the May 2025 estimate of 9.7 months.

Sales Price

The median sales price of new houses sold in May 2026 was $424,900.

This is 2.0 percent (±10.8 percent) above the April 2026 price of $416,500, and is virtually unchanged from the May 2025 price of $424,800.

The average sales price of new houses sold in May 2026 was $540,600. This is 7.8 percent (±10.0 percent) above the April 2026 price of $501,400, and is 5.0 percent (±9.3 percent) above the May 2025 price of $514,800.

The sales price numbers are interesting but useless. They are skewed by sale to price insensitive buyers at the high end.

Also, the numbers mask lot size, the number of rooms, and amenities.

The lead chart and the detail below provide better views. Sales are declining while inventory is rising.

New Home Sales Annualized vs Homes for Sale Detail

Sales are flirting with the lowest number since 552,000 in September of 2022.

A Drop below 576,000 from the current 580,000 would do that.

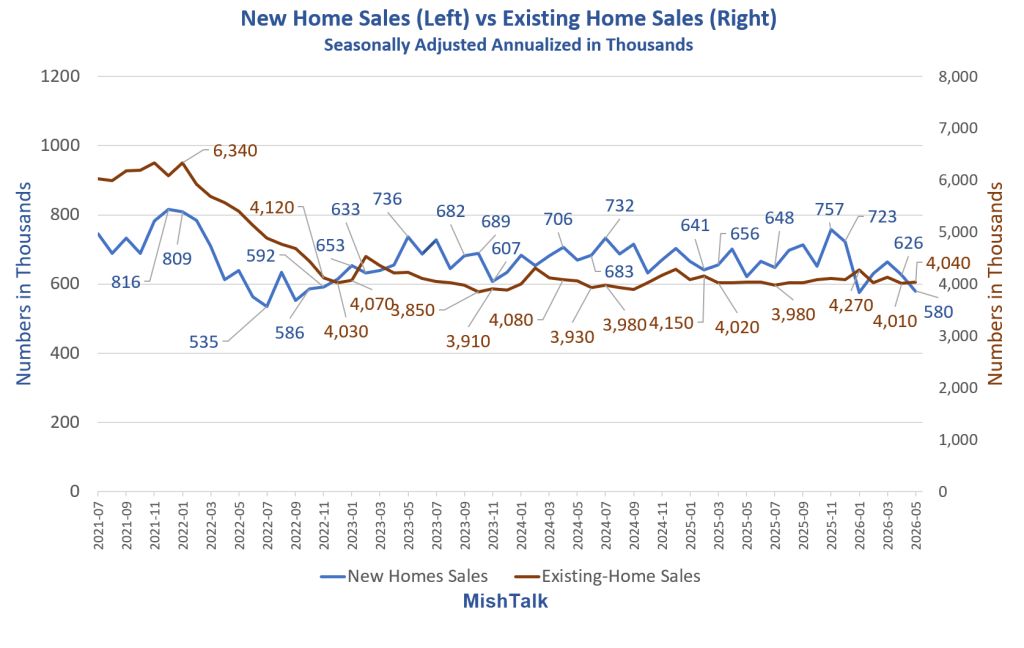

New Home Sales vs Existing Home Sales

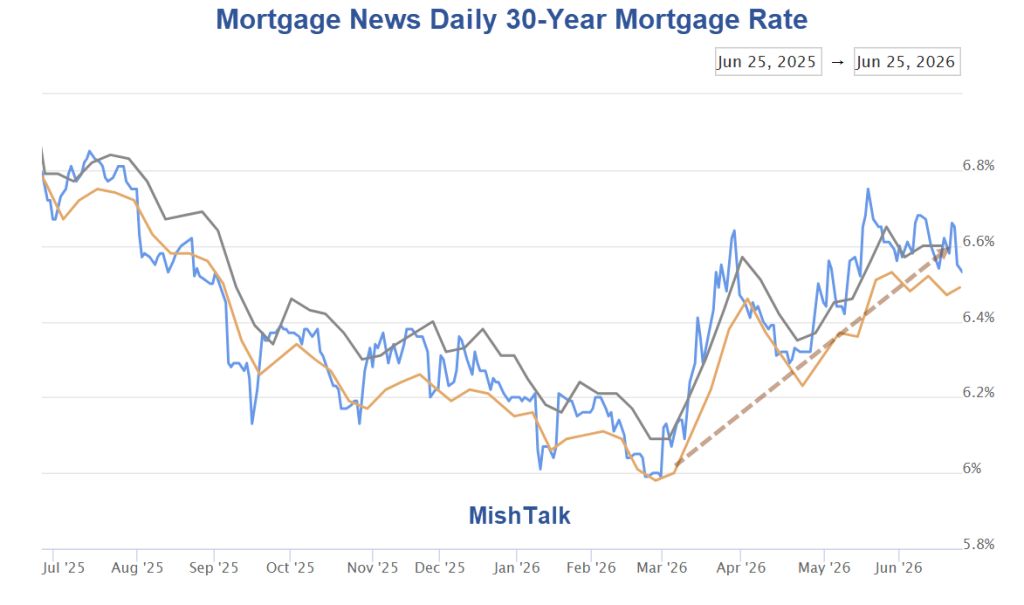

Mortgage News Daily 30-Year Fixed Mortgage Rates

Complete Stagnation

There has been complete stagnation in new and existing home sales since late 2022.

No one wants to trade a 3 percent mortgage for a 6.5 percent mortgage and renters cannot afford either new or existing home prices.

If you couldn’t afford to buy at 6.0 percent then without big price declines you cannot afford to buy at 6.5 percent.

How the Fed Broke the Housing Market

In the Covid Pandemic, the Fed lowered its base lending rate to zero percent.

As a result, mortgage rates dropped below 3.0 percent for a sustained time.

Nearly all existing mortgage holders refinanced.

This put extra money in mortgage holder’s pockets to spend, and they did.

This extra spending cash was on top of three rounds of highly inflationary free money Covid stimulus

The Fed did not see that coming either.

Free money plus low rates stimulated a massive price boom and competition for houses.

When the price of homes rose, so did homeowner’s insurance rates, cost of repairs, flood insurance, and property taxes.

Now all but price insensitive buyers are stuck.

No Apologies

With no apologies ever offered, that’s how the Fed broke the housing market.

The Fed still defends slashing rates to zero.

And the Fed offers nothing but excuses as to how and why it missed the highly inflation impacts of mortgage stimulus on top of three rounds of Covid stimulus, the last of which never made any sense at all.

Housing Starts Crash 15.4 Percent

In case you missed it, please see Housing Starts Crash 15.4 Percent on Top of Steep Negative Revision

Compared to the unrevised April number, starts decline 19.7 percent.

Related Posts

January 30, 2026: Dear Zoomers, Trump Says He “Wants to Drive Up Housing Prices”

Somehow, I doubt Gen Z will like this message.

May 26, 2026: Consumer Credit Stress Is Comparable to the Great Recession

Auto delinquencies are at a new record and credit cards are near record high.

Thank you Fed.

Comments

Log in or sign up to join the conversation.