Affordability Has Ended Many Dreams of Living Alone

The Wall Street Journal reports Moving Back Home Used to Be a Sign of Failure. Now It Shows Financial Savvy.

Last year, 49% of adults under age 30 lived with a parent, up 12 percentage points from 2019, according to the Federal Reserve.

The trend of young adults living at home is now seen as financially prudent, transforming aspects of American society, including home design.

High living costs, including a national median home price above $400,000 and record rents, drive young adults home.

Living at home as a 20-something was once viewed as a failure to launch and even a source of embarrassment in a culture that places a premium on independence. That is no longer the case. Living at home is now often viewed as a sign of financial prudence, and for some, a long-term prospect.

Chronically high living costs are helping reshape the milestones of early adulthood in America. The national median home price hovers above $400,000. Rents are at record highs in cities across the U.S., and many recent college graduates are saddled with tens of thousands of dollars in student debt.

The Moved Home Aren’t Sorry

The New York Post reports More than Half of Young Adults Moved Back Home After Leaving.

Almost 60% of young adults have moved back home at some point, but they don’t see it as a failure to launch. They see it as financially savvy.

But adult children aren’t just moving back home. Unlike previous generations, when living with parents past a certain age carried a distinct stigma, these “kids” aren’t ashamed about their living-at-home status.

They Moved Home—and Aren’t Sorry

According to the survey, 3 in 4 young adults say living with family or in transitional housing (often with a roommate) is a “smart financial strategy,” not a setback, and 26% declared they moved home to deliberately save money.

A vast majority of the respondents—62%—said the harsh stigma around moving back home has faded compared with previous generations, and 63% say they personally no longer feel embarrassed or judged about their living situation.

While the most recent U.S. Census figures found that 33% of individuals aged 18 to 34 live with their parents, it is even higher in pricey states like New Jersey (44.1%), Connecticut (41.3%), California (39.1%), Maryland (38.5%), and Florida (36.6%).

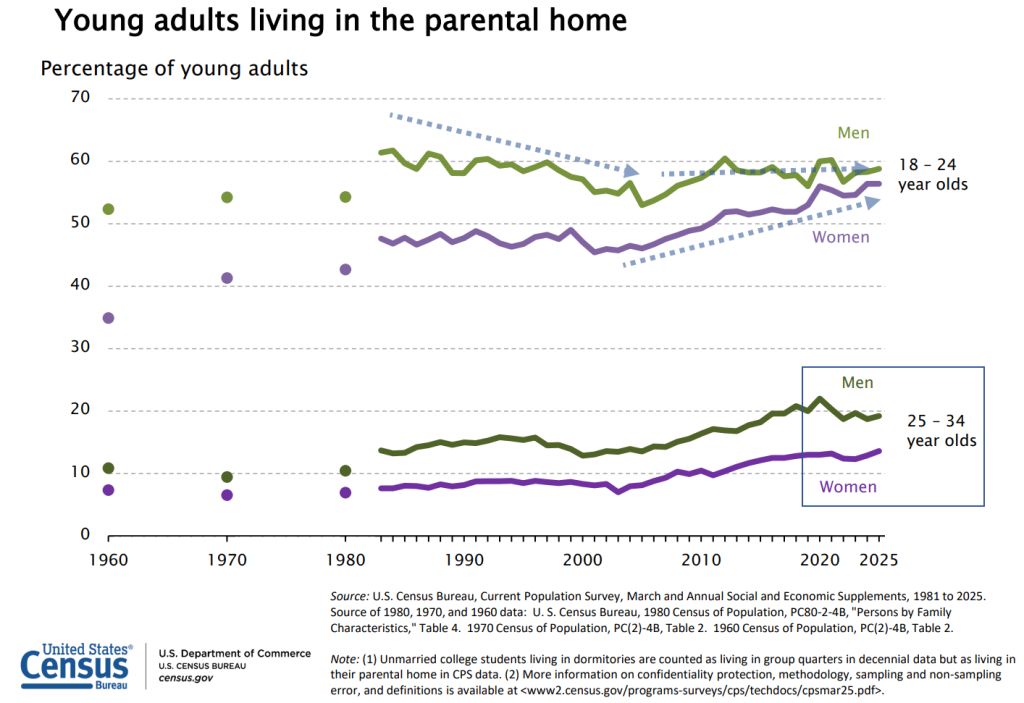

Trend Isn’t New

The lead chart, from the Census Department, shows the trend is not new.

Neither the Wall Street Journal nor the New York Post linked to the Fed report.

This is hardly surprising. Few sites link to anything external anymore.

Economic Well-Being of U.S. Households

Please consider the Fed report on the Economic Well-Being of U.S. Households in 2025 – May 2026

Living Arrangements and Care Work

The share of young adults who live with their parents has increased in recent years. In 2025, 49 percent of adults under age 30 lived with a parent. This share was up by 6 percentage points since 2022, and up 12 percentage points since 2019, just before the pandemic.

One-in-four parents with children under age 13 used paid childcare. Most families who paid for both childcare and housing spent at least 50 percent as much on childcare as on housing.

Income and Expenses

Forty-seven percent of adults ages 18 to 29 received help from someone outside their household to pay an expense in the prior 12 months. Money for a cell phone bill, for general expenses, and for housing costs—such as rent, mortgage or utilities—were the most common forms of help that people received.

A majority of adults (58 percent) said that changes in the prices they paid compared with the prior year had made their financial situation worse, but this share was down from 60 percent in 2024 and 65 percent in 2023.

Economic Hardships

Sixteen percent of adults did not pay all of their bills in the prior month, and 8 percent said members of their family sometimes or often did not have enough to eat. Both measures were similar to 2024.

Twenty-six percent of adults skipped medical expenses because of cost in the prior year, down from 28 percent in 2024.

Fifty-nine percent of adults had at least one type of major, unexpected expense in the prior 12 months. The most common unexpected expenses were a major vehicle repair or replacement (30 percent of adults), followed by a major house or appliance repair and unexpected major medical expenses (22 percent and 21 percent, respectively).

Credit

Since 2023, total credit card balances increased more for individuals currently experiencing financial difficulty. Using merged credit bureau data, average balances increased by more than 35 percent among those who said they were “finding it difficult to get by.”

Credit card ownership continues to be lower among Black and Hispanic adults; however, carrying a balance on a credit card was more common among these groups.

Buy Now, Pay Later (BNPL) use edged up 1 percentage point to 16 percent of all adults. Eleven percent of BNPL users had a payment trigger an overdraft or non-sufficient funds (NSF) fee from their bank in the prior year.

Twenty-three percent of adults with student loans had recent payment difficulty. Slightly more than three-quarters of those experiencing payment difficulty said it was due to reasons related to affordability.

Housing

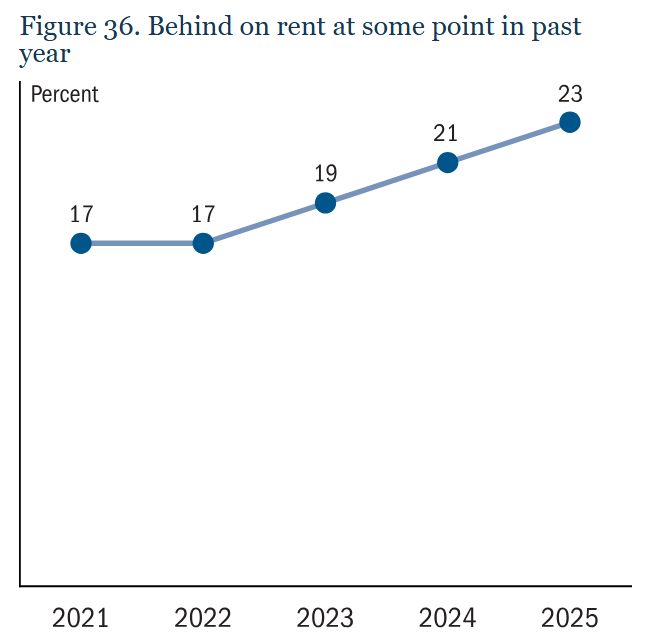

Challenges paying rent increased compared with the prior year. Twenty-three percent of renters reported that they had been behind on their rent at some point in the past year, up 2 percentage points from 2024 and 6 percentage points since 2021.

The cost of homeowners insurance affected homeowners in several ways, leaving some at increased financial risk. Six percent of homeowners went without homeowners insurance entirely, a majority because of cost. Among owners who had insurance, 20 percent said they could not afford as much coverage as they wanted, while 14 percent said they struggled to afford the premiums.

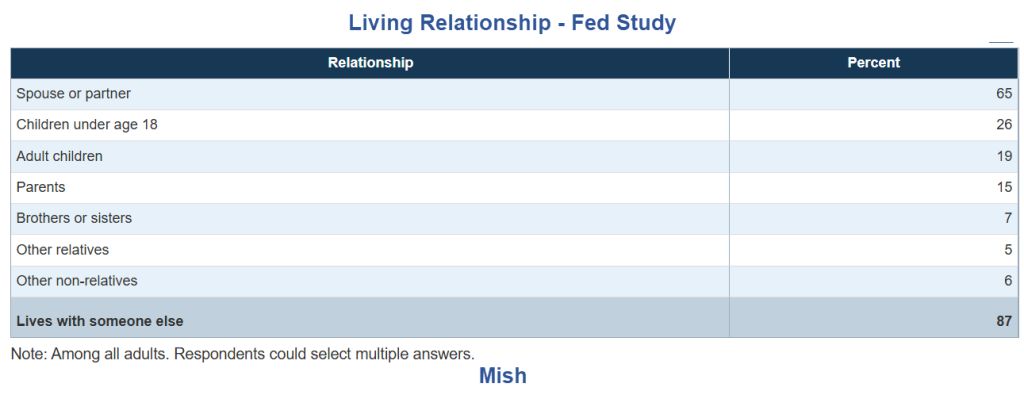

Living Relationship Fed Study

Given that multiple answers are allowed, one cannot just add up the numbers.

In this representation, 19 percent of of households report living with adult children.

Only 15 percent report living with parents.

There is no breakdown, at least that I can find, by age.

I do see this telling statistic on rent.

Falling Behind on Rent

A separate chart shows 31 percent of those making less than $50,000 per year have fallen behind.

Falling behind on rent is certainly not good. And those falling behind are apt to consider other living arrangements including moving back in with parents.

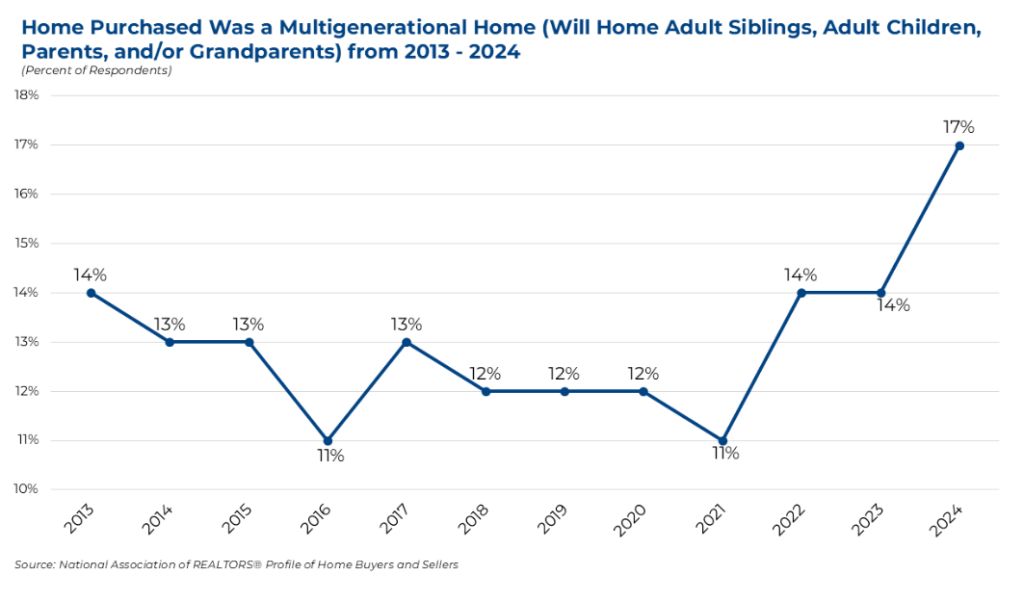

One Big Happy Household

A May 27, 2025 study by the NAR comments One Big Happy Household: How Families and the Data Are Shaping Multigenerational Living

The latest edition of NAR’s Profile of Home Buyers and Sellers report revealed that multigenerational buying was at an all-time high, with 17% of homes purchased last year being a multigenerational household. Multigenerational homes are defined as households that with more than one generation, such as adult siblings, adult children, and/or grandparents.

In 2024, a notable 36% of homebuyers cited “cost savings” as the primary reason for purchasing a multigenerational home—a significant increase from just 15% in 2015. We have also seen a rise in adult children residing with their parents, contributing to the increase in multigenerational home buying. Twenty-one percent of respondents in 2024 mentioned children over the age of 18 moving back into the house as a reason for their multigenerational home purchase, up from 11% in 2015. Additionally, in 2024, 20% of respondents reported that their adult children or relatives had never left home, compared to 7% in 2015. These shifts underscore the rising popularity of multigenerational living arrangements, driven by both economic factors and family dynamics. Adult children may continue living at home seeking financial stability due to high living costs, student loan debt, and difficulties in finding well-paid jobs.

SpareFoot Report

On June 4, 2026, SpareFoot reported Moving Out Isn’t What It Used to Be

Moving out used to feel like a clear line between “before” and “after.” You saved up, signed a lease, and started your next chapter. In 2026, it’s rarely that simple. For many young adults, leaving home is less of a one-time move and more of an ongoing process. Costs are higher, timelines are longer, and the path forward often includes detours, from living with family again to relying on short-term setups between leases.

SpareFoot Key Takeaways

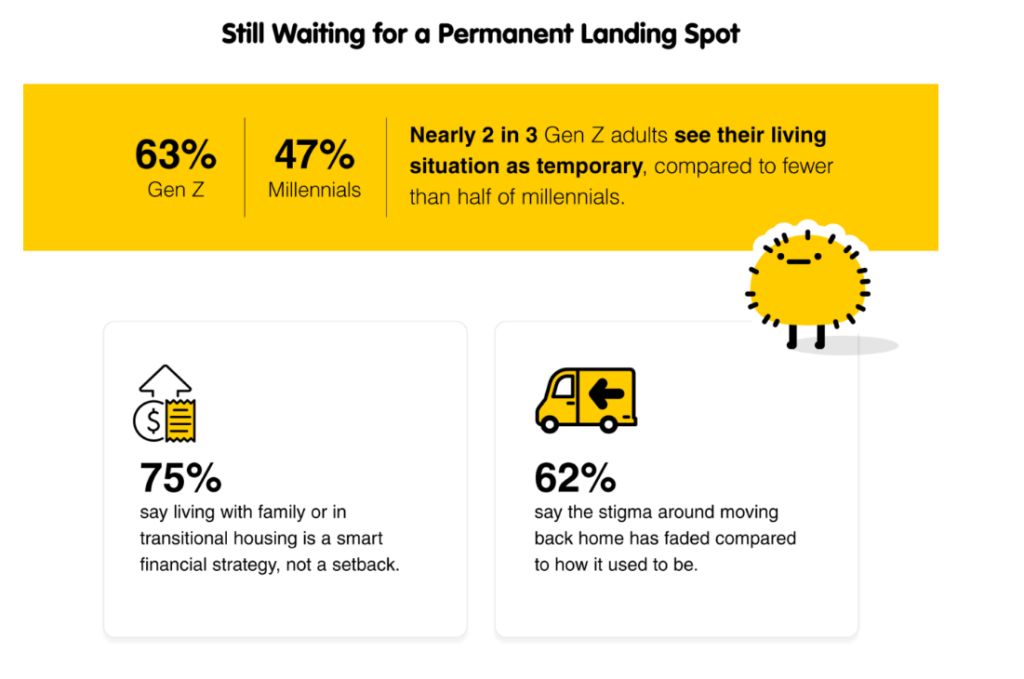

7 in 10 young adults have raised their move-out savings target in the past year, pushed by tariffs, inflation, and rising rents. Gen Z (71%) and millennials (70%) are nearly identical in their financial urgency.

2 in 3 young adults (66%) have delayed or turned down at least one major life milestone because they couldn’t afford to move out, including career opportunities (26%), higher education (21%), serious relationships (19%), and a personal fresh start in a new place (37%).

The median young adult says they need $10,000 saved to realistically move out, but puts their minimum “move out tomorrow” floor at $7,250.

Nearly 3 in 5 young adults who have lived independently (58%) have moved back home at least once, with 15% doing it more than once. The boomerang generation is no longer an outlier. It is the norm.

3 in 4 young adults say living with family or in transitional housing is a smart financial strategy, not a setback, marking a clear cultural shift in how the path to independence is perceived.

Nearly 2 in 5 young adults (39%) have used a storage unit during a move, upon returning home, or during an in-between period, making self-storage a standard tool in the modern moving playbook rather than a last resort.

I cannot find any of the quotes The New York Post or the Wall Street Journal mentioned as coming from the Fed report.

However, the Census chart and the SpareFoot report tells the story. Living alone sure isn’t what it used to be.

Related Posts

May 26, 2026: Consumer Credit Stress Is Comparable to the Great Recession

Auto delinquencies are at a new record and credit cards are near record high.

June 16, 2026: Housing Starts Crash 15.4 Percent on Top of Steep Negative Revision

Compared to the unrevised April number, starts decline 19.7 percent.

June 25, 2026: New Home Sales Drop Another 7.3 Percent, Builders Struggle with Rising Inventory

Sales are down. Inventory is high and rising, pressuring builders.

July 5, 2026: Case-Shiller National Home Price Index Hovers Near All-Time Highs

Home prices remain in the stratosphere, transactions in the gutter.

July 9, 2026: Existing-Homes Sales Decline 2.4 Percent in June Following Hopeful May

The Spring sales season ends with a thud. Affordability is in the gutter.

Yet, NAR chief economist Lawrence Yun says affordability is rising.

What a hoot.

Comments

Log in or sign up to join the conversation.