VIX made its final swing low at weekly mid-Cycle support at 15.93 on Friday morning, making it the last support before its reversal. An aggressive buy signal (NYSE sell signal) may be confirmed with a rise above Long-term support/resistance at 18.30. A breakout above the neckline suggests a very robust follow-through rally that may last up to a month.

SPX retraces to the 4.3-year trendline.

The SPX rallied back to its 4.3-year trendline at 2009.13 before closing at the Fibonacci 61.8% retracement level at 1999.44 and just above it mid-Cycle support/resistance at 1993.04. This trendline was originally broken on January 6, in the decline to the January 20 low. Trendlines are important support areas that often attract, then repel the markets. Now that the attraction was satisfied, the reversal may begin.

(USAToday) U.S. stocks rallied Friday to log a third straight week of gains after the February jobs report came in stronger than expected, signaling that the economy continues to grow despite slowing growth overseas and early-year financial turbulence.

The Dow Jones industrial average also notched its first four-session winning streak since October. The blue chips ended up 63 points, or 0.4%. to 17,006.77, rising above 17,000 for the first time since Jan. 6. The broader Standard & Poor's 500 stock index gained 0.3% to 1999.99 and the Nasdaq composite climbed 0.2% to 4717.12.

The S&P has also not been above 2000 — a level it passed in intraday trading Friday — since Jan. 6.

NDX ends week beneath Intermediate-term resistance.

NDX challenged weekly Intermediate-term resistance at 4386.86 this week, closing just beneath it. Its retracement was a weaker 55% of its decline. Should it decline beneath weekly mid-cycle support at 4161.67, NDX may continue its decline to 3000 or lower.

(LATimes) Even in the volatile world of technology stocks, it was a stunning moment for investors.

Shares of the tech companies LinkedIn Corp. and Tableau Software Inc. dropped like an anvil from a cliff early this month after the firms reported disappointing growth forecasts. Their stocks plunged more than 40% in a single day and sparked a sell-off in other tech stocks as well.

"I don't remember seeing a reaction as violent as that since the dot-com bubble burst" in 2000, said Pat O'Hare, chief market analyst at Briefing.com, an investment research site.

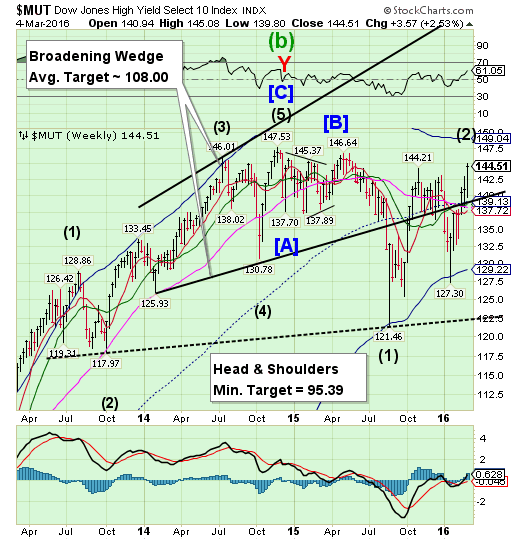

High Yield Bond Index may have completed its rally.

The High Yield Index took over 6 months to complete its 94% retracement of the August low. The retracement appears to be over and the decline about to resume. The next retracement will not be as generous..

(ZeroHedge) Two days ago, Credit Suisse reported something which had been rather visible in the markets: an onslaught of retail buying had entered the junk bond market in which institutions were delighted to sell to retail bagholders, in the process repricing the entire HY space if only briefly.

Overnight, fund flow tracking service EPFR confirmed this when it reported that US high yield funds recognized a $5.27bn (+2.8%) inflow for the week ended March 2nd, the largest ever in terms of $AUM and the 2nd largest on a percentage basis.

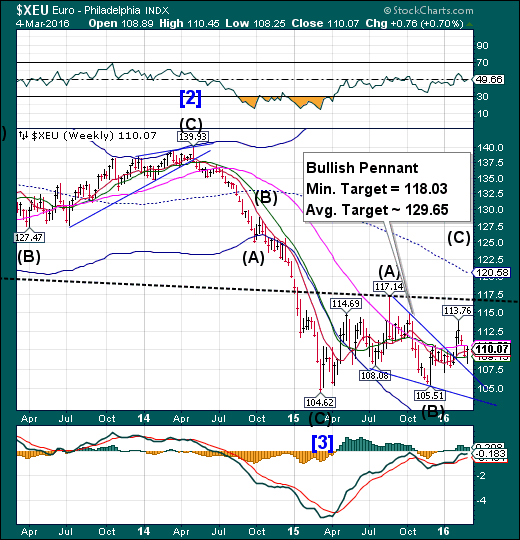

The Euro reverses course.

The Euro challenged Intermediate-term support at 109.15but bounced back, closing short of Long-term resistance at 110.52. The Cycles Model suggests a period of strength has begun and may last approximately three weeks with the minimum Pennant target in reach.

(ZeroHedge) The nominal trade-weighted dollar index, against major currencies, is now just 4% higher year-over-year as the index has recently fallen from an approximately 13-year high of 95.6 to 92.4. The slow down in the rate of change is important since at one point in 2015 the nominal trade-weighted dollar index was increasing at a 22% year-over-year pace. While we still think its early to call the end of the dollar bull market that has been in place since July 2011, its apparent that the world is currently not in as broad of a dollar bull market as we were in last year.

EuroStoxx reaches resistance.

EuroStoxx probed its February high resistance level this week, completing a 45% retracement of its decline. Crossing beneath Short-term support at 2947.48 reinstates a probable sell signal. The Head & Shoulders neckline defines the magnitude of the decline..

(MarketWatch) European stocks closed higher Friday, getting a lift from a mostly encouraging U.S. jobs report and giving the market a third weekly win in a row.

The benchmark Stoxx Europe 600 SXXP, +0.70% rose 0.7% to end at 341.80. The index bumped up by more than 1% just after the data on U.S. nonfarm payrolls, but came off its session high.

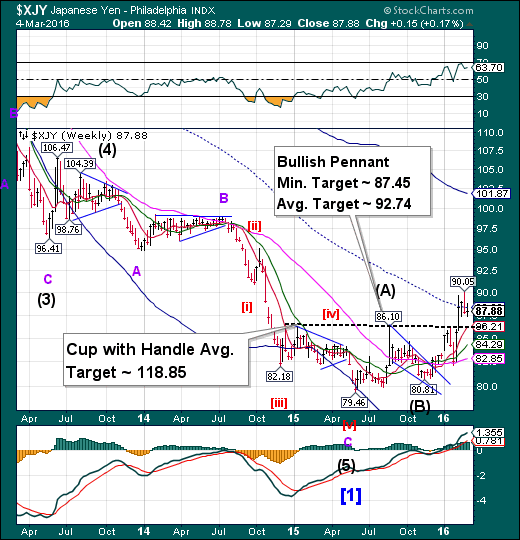

The Yen is still consolidating.

The Yen continued to consolidate in a narrow trading range. The Cycles Model has been indicating a very strong period of strength in the next week, with another probable episode of strength at the end of March. The immediate implication of a breakout is a probable rise to an average near 92.74 or higher. The (short-term) pennant target may come in a matter of a week, while the Cup with Handle target may take up to a month to develop.

(WSJ) What do Donald Trump, Hillary Clinton and the Dutch finance minister have in common?

Answer: They have all recently expressed concern about the way Japan is handling the yen—much to the consternation of policy makers in Tokyo, as they struggle to revive the country’s economy with ever-looser monetary policy.

For the two front-runners in the U.S. presidential race, Japan’s moves—including setting negative interest rates on some bank reserves for the first time in late January-- amount to currency manipulation. Mrs. Clinton last week referred to Japan as a long-term culprit.

.The Nikkei rally is complete, or nearly so.

The Nikkei retracement from the February 12 low has nearly attained mid-Cycle resistance at 17319.37. This clarifies the location of the Head & Shoulders formation neckline. The Cycles Model suggests that the rally may be over with at least two weeks of decline ahead.

(Bloomberg) Japan’s Nikkei 225 gauge is tracing chart patterns seen in the 12 months through April 2008. A series of Federal Reserve rate cuts that began in September 2007 appeared too late, Norihiro Fujito, a strategist at Mitsubishi UFJ Morgan Stanley Securities, says in an interview today. The Nikkei fell 36% in the remaining eight months of 2008. The “eerie” parallel is unnerving, and may continue should U.S. and Japanese policy makers take the wrong actions, he said, referring to the recent Fed rate hike and a planned increase in Japan’s consumption tax.

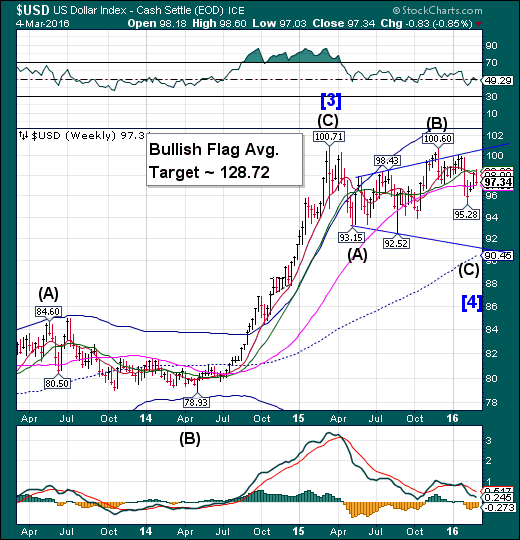

U.S. Dollar reverses from Intermediate-term resistance.

USD challenged Intermediate-term resistance at 98.36 again this week before reversing back down to Long-term support at 97.07. The Cycles Model suggests a long decline may follow, lasting through mid-May. It may finally turn traders bearish the dollar..

(Reuters) The U.S. dollar fell, hitting one-week lows against the euro on Friday after a drop in U.S. wages in February overshadowed strong jobs growth and supported views that the Federal Reserve was in no hurry to hike interest rates.

Average hourly earnings fell 3 cents in February, data from the Labor Department showed. Analysts said traders were fixated on that drop even as nonfarm payrolls increased by 242,000 jobs last month.

The dollar was set to post its first weekly decline against the euro in three weeks.

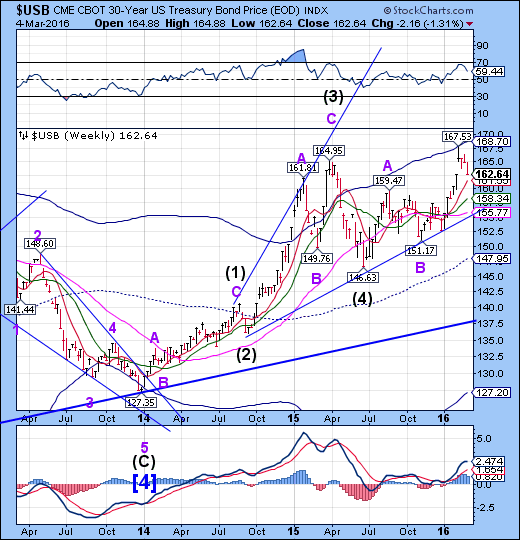

USB completes its retracement.

The Long Bond may have completed its retracement above Short-term support at 161.55. The pullback may be a prelude to a very strong probe to or above the Cycle Top, due by the end of March. Over the next several weeks we’ll be looking for the 34.4-year high in Treasuries. The long Treasuries trade is getting very crowded.

(ZeroHedge) Yesterday morning we noted a very disturbing trend: over the past three days, a shortage of 10 Year treasury paper has manifested that has grown more and more acute with every passing day, until the repo rate hit as low as -2.95% yesterday morning just shy of the "fails" -3.00% minimum rate, the lowest on record, and suggesting that the marketwide treasury shortage has never been worse as a result of a huge short overlay.

As we also noted yesterday, some such as Stone McCarthy were hopeful that the shortage would cease following yesterday's auction schedule announcement by the Treasury. We were more skeptical:

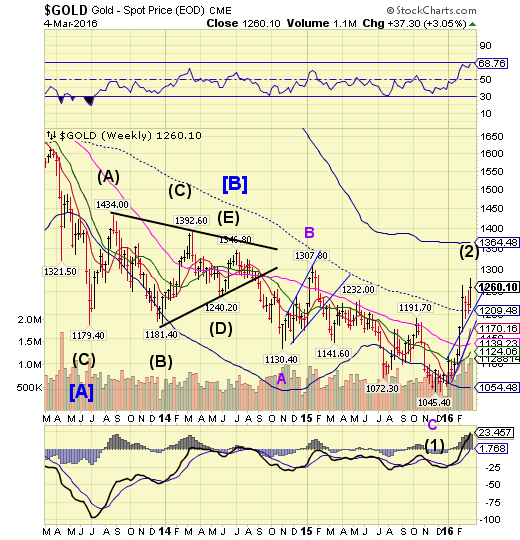

Gold broke out higher.

Gold broke out higher against its February high at 1263.90. However, closer analysis shows the rally may be limited beneath 1300.00. In addition, the period of strength may run out in the next week. Once complete, Ending Diagonals are completely retraced, leaving this move as a potential false breakout within the downtrend.

(Bloomberg) As global stocks enter a bear market, gold is on the verge of bull status.

Global stocks slumped Thursday as investors shunned risk worldwide amid concern that central-bank efforts to support economic growth are losing potency. Federal Reserve Chair Janet Yellen yesterday told Congress that market turbulence may weigh on the outlook for the economy if it persists. The metal jumped as much as 5.8 percent to $1,263.90 an ounce, the highest since February 2015, and the gain was the biggest intraday advance since 2009.

Crude broke out above resistance.

Crude broke out above its prior high at 34.82, closing above weekly Intermediate-term resistance at 36.23. The Cycles Model suggests the period of strength may only last until mid-week, so the rally may be limited to the Flag trendline or Long-term resistance at 44.26. Crude may then resume the decline through late March, with Cycle Bottom Support continuing to fall away at 15.83, supporting the target analysis of the Bearish Flag. Analysts won’t be calling for a bottom when it finally arrives.

(OilPrice.com) Despite domestic production declining and demand surging, the EIA reported oil inventories surge by more than 10 million barrels, or more than three times what was expected.

The 10.4 million barrel increase was mostly due to a near record increase in imports of 490,000 b/d (3.4 million barrels weekly) and an adjustment swing of 352,000 b/d (2.5 million barrels weekly) by the EIA. The latter has been a repeated pattern to exaggerate the levels of inventory, a pattern going back to 2015.

Shanghai Index bounces off January 27 low.

The Shanghai Index declined to its January 27 low on Monday, then bounced near the top of its consolidation range. This weekend appears to be a key Trading Cycle Pivot, suggesting a decline through the month of March may follow. The Cycles Model calls for a decline that may shock investors.

(ZeroHedge) Back in October, the latest credit impulse in China just rolled over and died.

Ahead of the actual news, MNI said “one source familiar with the data said new loans by the Big Four state-owned commercial banks in October plunged to a level that hasn't been seen for many years."

Sure enough, when the numbers hit, it wasn’t a pretty picture. RMB new loans came in at just CNY514bn in October - consensus was far higher at CNY800bn. That was down 6.3% Y/Y. Total social financing fell 29% Y/Y to CNY447 billion, down sharply from September’s CNY1.3 trillion print.

So what, did China do you ask? Well, they unleashed massive fiscal stimulus:

The Banking Index completes a retracement.

-- BKX completed a 48% retracement of its decline to the February 12 low in three weeks. The Cycles Model now suggests a probable three week decline that may exceed this year’s initial decline. .

(ZeroHedge) Just stunning.

German newspaper Der Spiegel reported yesterday that the Bavarian Banking Association has recommended that its member banks start stockpiling PHYSICAL CASH.

Europe, of course, has been battling with negative interest rates for quite some time. What this means is that commercial banks are being charged interest for holding wholesale deposits at the European Central Bank.

In order to generate artificial economic growth, the ECB wants banks to make as many loans as possible, no matter how stupid or idiotic. They believe that economic growth is simply a function of loans. The more money that’s loaned out, the more the economy will grow.

This is the sort of theory that works really well in an economic textbook. But it doesn’t work so well in a history textbook.

(ZeroHedge) US financials are tumbling after The Fed proposed a rule that would limit banks with $500 bln or more of assets from having net credit exposure to a “major counterparty” in excess of 15% of the lender’s tier 1 capital. Bloomberg reports that The Fed's governors plan to vote today on the proposal. The implications of this are significant in that it will force some banks to unwind exposures and delever against one another (most notably with potential affect the repo market which governs much of the liquidity transmission mechanisms). Guggenheim's Jaret Seiberg warns the proposal is likely to be "stringent," though less onerous than the Dec 2011 proposal.

(CNBC) Wall Street banks are driving off with the auto lending finance business — but automakers, who vastly expanded their financing capabilities in the years since the global financial crisis, are backing more borrowers, as well.

By the end of 2015, banks — the primary source of credit to car buyers who need to borrow — expanded their market share to more than 35 percent, according to Experian's State of the Automotive Finance Market report for the fourth quarter. Banks control more of the auto financing market than any other entity, the report said.

(ZeroHedge) Once again we find that it is only after they leave their official posts that central bankers finally tell the truth.

Last night, it was Alan Greenspan who blasted the state of the economy, saying that "we’re in trouble basically because productivity is dead in the water" and when asked if he is optimistic going forward, Greenspan replied "no, I haven't been for quite a while."

Then on Sunday, the former head of the BOE, Mervyn King, warned that another aspect of the global economy, namely the financial system whose structural problems remain untouched since the financial crisis have been untouched, is "certain to have another crisis."

Have a great weekend!

Comments

Log in or sign up to join the conversation.