Fed 'credibility' is actually diminished by their headlong dash to reclaim it. By that I simply suggest that they're moving from an extreme (too low for long) to over-compensating by throwing the country into deeper Recession (as I've believed we're already there, while talking ourselves into it even faster).

The impact of global tightening on the global economy is what matters here in my view, not our worked-up Fed moving to restore their 'perceived' control of inflationary forces. Of course they contributed to those inflationary forces and now they are contributing very little to easing that, since other factors followed the Fed's ease (which prompted our 'Inger Bottom' March 23rd 2020 Call) and in a similar way their being 'asleep at the switch' a year ago contributed to our warning of building risk as buybacks dominated the excess S&P upside, as it also led to the assessed historical insider selling into strength back then.

The Fed is powerful, and the market listens. And this approaches negates the very 'soft landing' the Fed wants. The market says what I've been saying: they cannot gain credibility by doing it this way, it won't be one or two big hikes and then 'softish' (which I preferred), although there is one way to do it.

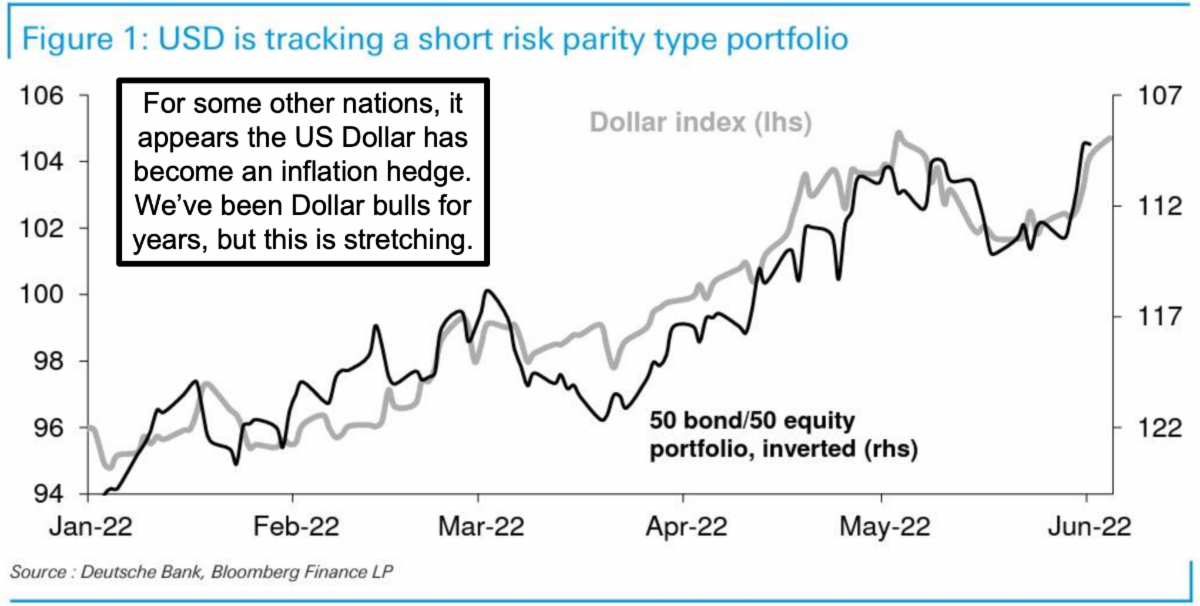

That way to a softish landing is to avoid financial 'events' (such as a financial or similar international failure as I mentioned regarding Italy or Japan again in the 2nd video), avoid 4 or 5 standard deviation events, stop a trend to hedge foreign problems by buying the Dollar assets (and I've been the Dollar Bull for years), and end the war in Ukraine one way or another (I prefer that Ukraine prevail, but it possibly a mistake to attempt to beat Russia in ground battles in the East), and avoid global food shortage or regional famine in the process.

In-sum:

The forces of war, of supply-chain inhibition, of alternating extremes in interest rate policies, and intertwined with higher-than-need-be Oil prices, all combine to be destabilizing toward global stability, much less growth, for now.

At the end of the day we'll get through this, but there's no doubt that heat this Summer can be more than dry, more than stormy, and more than navigable, if central bankers don't back-away from their hubris, and realize it takes efforts on the diplomatic side to achieve what they want on the financial side. That is not a call for dominant globalism, but for reasonable policies that work with as well as not against, the global order. Otherwise it unravels further.

Historically, these kind of inflations combined with regional conflicts, lead not to peace but to greater war, famine, revolution and general upheaval. Hence the goal ought to be unity not division, peace not war, and a good harvest, not starvation. In environments like that, stability would lead to growth, prosperity not frivolous excess, to return, and appreciation of the brotherhood of man as opposed to the petty goals of those fostering division rather than harmony.

Comments

Log in or sign up to join the conversation.