Ratcheting back down late Tuesday, after a very stand-up earlier recovery, S&P was essentially implying worries about inflation dominating the tone.

Or at least the market was pondering both 'end of month' action versus what sort of seems like the President threw the Fed Chairman under the bus today.

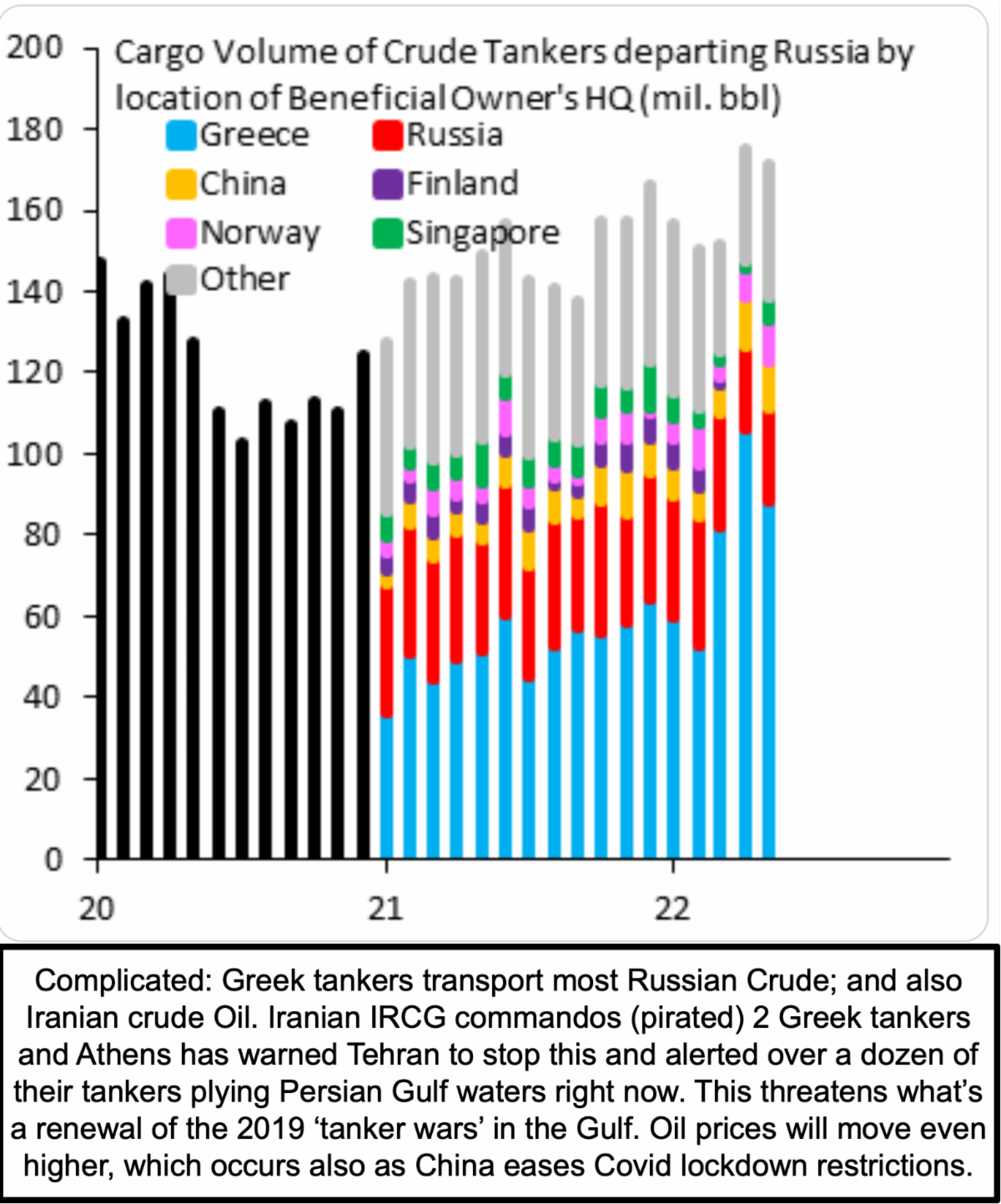

Hard to say because of conflicting concerns, and even volatile Oil prices with the combination of EU 'carve-outs' for pipeline-delivered Oil to Hungary (etc.?) versus embargoing tanker-delivered crude which accounts for the majority so the media can 'say' that Russia has been sanctioned, but all they need to will be ship more through pipelines, most of which transit Ukraine by the way.

However the financial focus here has to be the Fed Meeting. No we don't see Biden imitating Lyndon Johnson who reportedly literally put Chairman Martin, at the time, against the proverbial wall and asked why he wasn't printing more money to cover expenses of the then-Vietnam war.

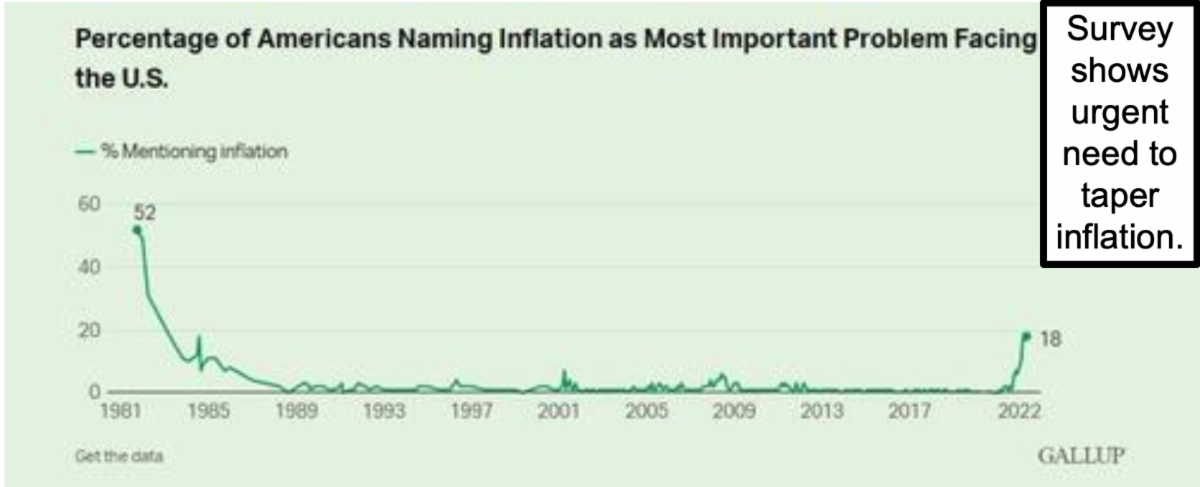

It does seem like Biden, with the subtle Op-Ed in today's Wall St. Journal, was shifting responsibility (blame?) to the Fed and even off-of Putin a bit. Well let's again note (as we often have) that the Fed was 'behind the curve' as inflation was percolating long before Biden took Office (especially wages and even Oil prices), however all these rose exponentially one Putin's war started, and yes, I had bemoaned the Fed's tardy action for many months, but also Congress in regard to poorly-allocated stimulus and other funding that has been seamless through the Administrations and the war as well.

In-sum:

The market was sobered this afternoon, after being levitated from an initial sell-off, as is fairly normal behavior for Tuesday of a short trading week.

You had pluses and minuses, ranging from China gradually opening business again (higher Oil), Iran making threats after hijacking 2 Greek tankers (again more tension and higher Oil), to dispatching far longer-range (40 miles vs. 20) artillery to Ukraine, to inflation raging with confusing comments by President Biden (somehow managed to bring Medicare costs into the discussion), while really there's plenty of blame to go around while inflation 'starts' to peak a bit.

Stable growth isn't really feasible yet, which the President's remark saying he is giving 'space' to the Fed (code word: 'respects the Fed's independence') is a bit of an off-loading of his political admonition to fight high prices, but let's do face one reality: before Putin's war, it really was the Fed that set this up and is in the position we warned they would be, unable to easily extradite from it too.

Suffice to say: Chairman Powell seems beholden to an idea that the Fed can't surprise the markets too much, whereas President Biden is content to spend trillions, and probably knows not much can be done about Fed policy short of screaming at Powell and demanding lower rates (something Trump is said to have done). If there's one thing that bothers me is that neither of these guys are likely to shift the world of inflation much for now. It can ease if we get any sort of 'peace' or ceasefire in Europe, combined with China really speeding-up it's re-opening, and inflation can worsen if war comes to the Persian Gulf, 'or', a significant hurricane comes to the Gulf of Mexico and knocks out a refinery.

Am I saying Oil prices have more to do with this than policy or politics? Yup. I suspect consolidate a bit, rally further, at least for now, news dependent.

An 'abbreviated' trading week often invites traders to enter the first dip, so that made the Tuesday's turnaround not only unsurprising but anticipated. Sure, of course the debate persists if this is or was 'merely' a 'bear market rally' or just a bit more. The bearish crowd is convinced it has no chance for success.

That's too simple. Bears should try to control their emotions, due to significant variables present in this market environment. For instance: S&P doesn't have to adhere to older bear market 'playbooks', as this market's been bearish for 18 months or so, with distribution under-cover of the S&P upside overrun last year. Note such wasn't the case with those projected catastrophic1999-2000 or 2007-2008 breakdown (debacles) which were broader and not limited to a handful of 'grand dame' stocks. At least they were basically 'in-sync', whereas nothing could be further from the case now.

Bears will argue that we're only a few months into decline, but they're wrong. I agree with them about a typical ending being more like a year into decline, but note the broad market is there for some months, so already it wasn't 'classic'. Sure, internally a resumption of heavy selling for this market (if indeed that will even happen) would be a final catharsis. But you'd have to crash the already mortally wounded majority of stocks.

Odds of that happening? Hard to handicap. Clearly it relates to inflation, or the perception that the 'world and economies' can do much of the Fed's work for them, minimizing the number of perceived hikes forthcoming, regardless of an embrace of multiple hikes beyond just a couple, that some suggest. All that is essentially meaningless 'if' the Ukraine war comes to an end, and Oil declines (and yes Oil is just as important to almost everything as long contended).

Meanwhile there is a 'possibility' that the bears of today will capitulate 'if' many things start going 'right', such as an opening of Ukraine ports to grain shipping one way or another. Moves toward peace and avoiding famine are important.

So the stage is set for another effort to sell-off early Wednesday, but based on trader sentiment (and willingness to short too readily), odds favor a rebound in mid-session, unless key news developments (like peace talks in Turkey being more than an offer, but an agreement to hold them) stimulate optimism earlier in the day. Could the S&P recover what it surrendered? Yes. Could whatever it recovers than be surrendered later on, sure. Depends on the news flow with technicals becoming only extended hourly, and pretty neutral on a daily basis.

Comments

Log in or sign up to join the conversation.