The market's newer 'troops' - will probably learn a lesson 'veterans' with any seasoned experience already know: never chase a big upside on so-called 'hot' IPO's. Time will tell if that's the case with the Rivian's (RIVN) grand start, but if history is a guide, the batteries fueling this initial run will deplete, and a period of introspection follows, requiring a period to... recharge its batteries.

This IPO took some of the rebound interest out of the general market today, but it's been expected to be defensive anyway, and straining to 'spark' upside of any potency. Essentially the 'mixed market' rotation, calling it a 'mosaic' is of course continuing, with prospects of more defense remaining ahead.

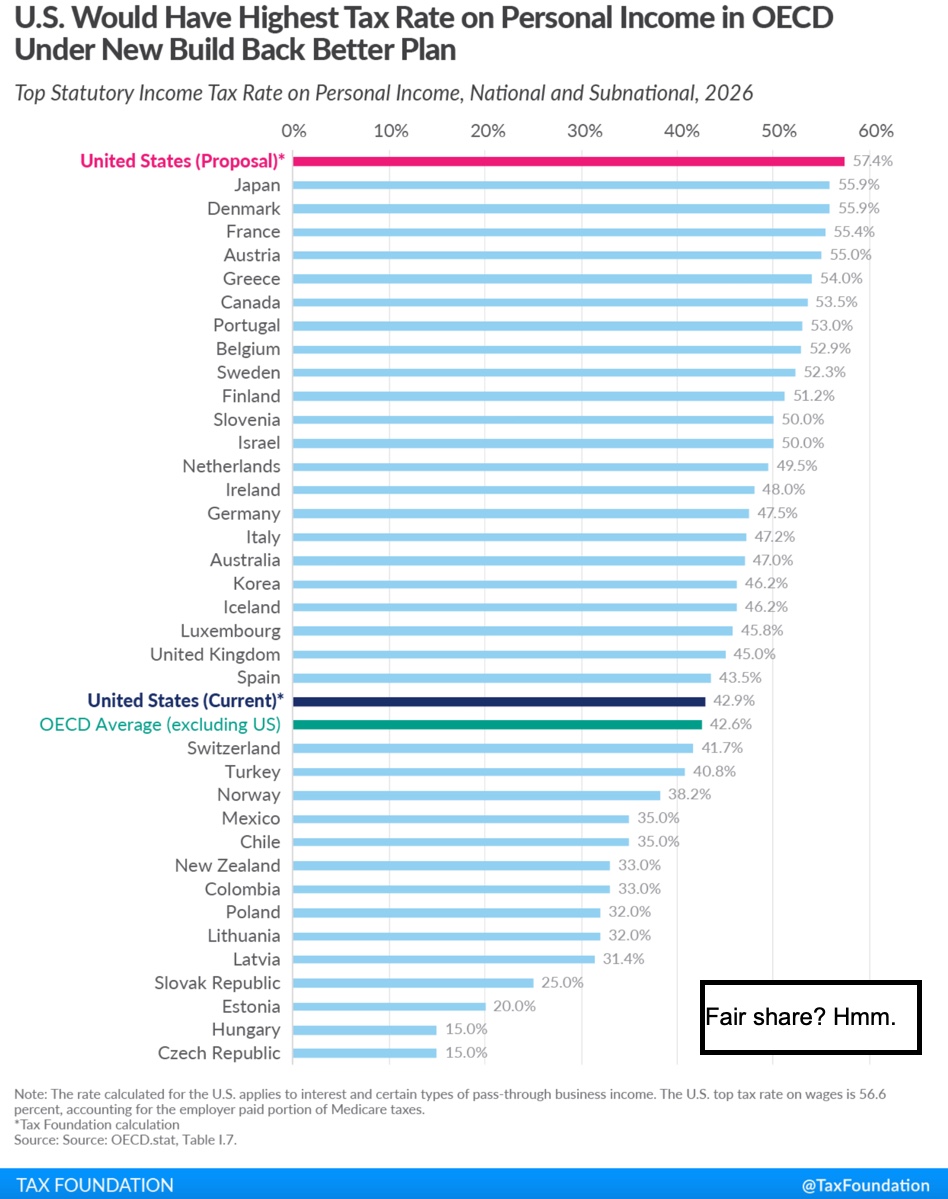

More significantly, the 'hot' inflation number (we expected that) coming just a week after the Fed's 'tapering' outline, reinforces defensive concerns that the Fed is behind the 8-ball so to speak (the Yield Curve) and will contemplate a more-rapid pace of tapering and higher rates over the next 2 years or so. Of course everyone will focus more on 'maximum' (possible) combined tax rates.

(And we have no idea of how these stack-up in other countries, aside known realities like most including some healthcare and some even education. So it is generally the case that perceived benefits are greater, but the taxation level may indeed be higher for low income workers, in some European countries.)

I'm not saying there's not arguments on both sides of this (there are plenty). I am saying that the 'pitch' that U.S. proposed taxes won't be higher than most in Europe are just not true (and most of their taxes 'include' healthcare plans, most crucially). So here's a breakdown as presented by the Tax Foundation.

(Similarly, we don't know income thresholds and deductibles as may prevail in any other Country, but we do know they generally include more 'benefits'.)

Executive summary:

- It's necessary to view individual stocks individually, as well as assess the prospects of their being impacted by seasonal factors like tax-loss or this year, even tax-gain selling, given the looming higher-tax 'possibilities'.

- If one has confidence or willing to speculate on certain companies under pressure this time of year as likely to see initially relief rallies in or into the early part of 2022, as well as have promising fundamentals of interest, it's perfectly normal (with patience) to gradually add to or accumulate stocks.

- None of this applies if you believe the Fed is about to accelerate 'tapering' dramatically, which they are loathe to do at the moment, but ultimately will as is at least logical to anticipate, it's a threading-the-needle challenge.

- Janet Yellen doubled-down on her 'it's going to be transitory' argument in an interview, and President Biden sort of freaked-out and ordered National Economic Council efforts to lower rising prices (presumably in energy), at the risk of questioning how they plan to accomplish that.

- What makes more sense is a move by France to increase nuclear power plants (at least exploring the prospect), which the U.S. likely should too, it might even drive business and assure stamina, which wind & solar can't, especially in winter, until we get to the reality of massive storage capacity.

- And that's been my point: alternative energy is fine, but politically relying on it before capacity or capability exists is counterproductive, something a few countries in Europe have already experienced, so we could learn.

- Europe has also been dealing with increasing COVID cases (as noted), so there is the prospect of cases increasing in the wake of renewed travel.

- COVID is still an issue, and so many believe vaccines relegated COVID to the history bins, but unfortunately that's not the case, with testing really emerging as the most important aspect to validate the already-vaccinated limited protection, as well as who would benefit from upcoming 'Pills'.

- Speaking of: California Governor Newsom reappeared, claiming his kids did an intervention so he would go 'trick & treating' with them (really?), so Halloween was 10 days ago, and the Climate Summit is still ongoing, for sure it's more likely he had a bad reaction to the vaccine booster shot.

- Even though recovered, one reporter showed his before and after videos to a neurologist and a dermatologist, and both thought tell-tale signs after having had Bell's Palsey (a possible side-effect).

- Glad that he recovered, but we'd prefer candor to the public as in a sense it would be reassuring if people knew the partial paralysis is temporary (he did go to the elite Getty wedding that Nancy Pelosi officiated at, but skipped the reception..).

- The EV sector got most of the discussion, not 'power grid' infrastructure shortcomings, except in France, which wisely considers more nuclear.

- We are 'not' interested in Rivian into strength, might not be in weakness either, but that's to be determined after lock-up period transpires.

- I've heard the argument that repeat sequential Amazon orders for trucks will make Rivian the next Tesla (TSLA), that's premature to say at least, at worst is ridiculous, Ford (F) was a serious beneficiary of this as the profits will be helpful to fill-out their EV product line, which is far-broader than Rivian.

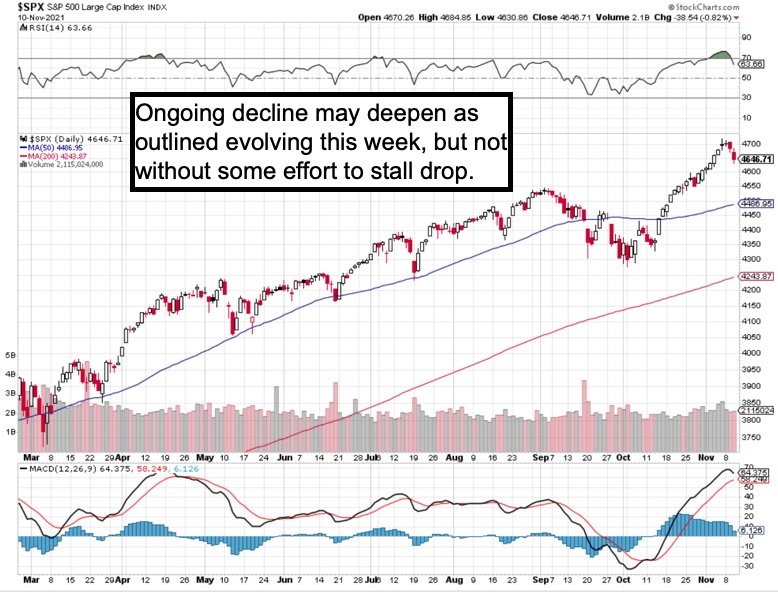

- Today was a defensive day in-line with the recent general warnings.

Bottom-line: massive realignments in some of the big groups, with erosion a characteristic of smaller ones. Some late session comeback but still remains defensive overall, as it should late this week. Thursday will probably see a rebound effort earlier, then the struggle resumes with probably repeated skirmishes shy of a flat-out breakdown.

Comments

Log in or sign up to join the conversation.