Kraft Heinz Company (KHC) stock has been treading water over the last 3 months, despite the new CEO's turnaround plan, designed to raise sales. Analysts still haven't raised their revenue forecasts or price targets. One play is to short out-of-the-money (OTM) KHC puts.

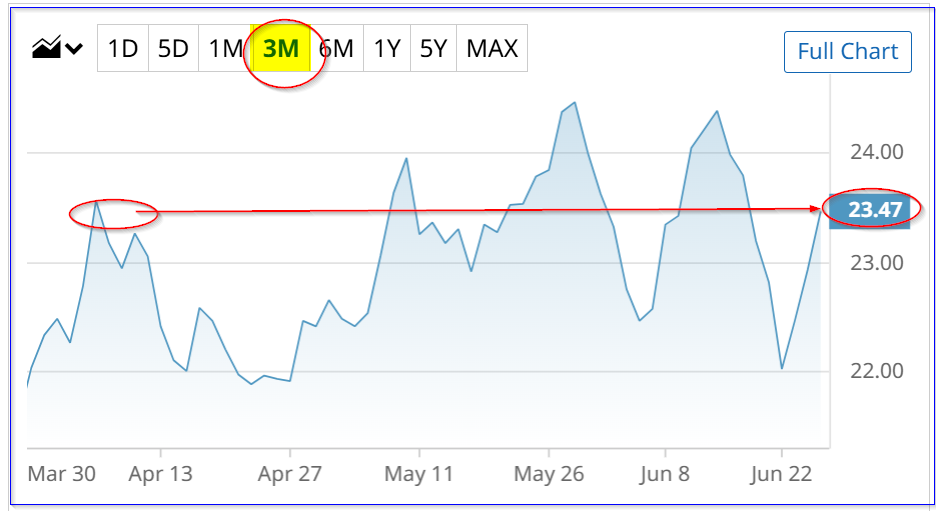

KHC closed at $23.47 on Thursday, June 25, about where it was two and a half months ago on April 6 ($23.57).

KHC stock - last 3 months - Barchart - June 25, 2026

So far, the market is not impressed with the CEO's initiatives. I discussed this in a recent Barchart article on June 3, “Unusual Trading in Kraft Heinz Call Options After CEO Interview - Is KHC Stock a Buy?”

I showed that KHC stock might not generate significantly more free cash flow (FCF). This is despite the CEO's attempt to raise sales through a $600 million investment in higher-protein and low-sugar products. Some of these products will be sugar-free Heinz Zero ketchup and protein-infused Mac & Cheese, etc.

I suggested that it might only generate $4.0 billion in future FCF, based on analysts' revenue estimates of $24.55 billion next year. Since that article came out, analysts' revenue estimates have stayed flat, which is not usual. Typically, analysts will tend to raise their forecasts, as evidence of higher revenue growth appears.

As a result, using a 14.3% FCF yield metric (which is the same as multiplying FCF by 7x), KHC stock would be worth $27.5 billion:

$4b x 7x = $28 billion fair market value

That's only slightly over its existing market cap of $27.8 billion, according to Yahoo! Finance (i.e., +.6%).

That sets its price target at just $23.61 (i.e., $23.47 x 1.006).

So, no wonder institutional investors are not piling into KHC stock.

Nevertheless, this is still a very low multiple. For example, AI-related tech stocks are trading at over 100x their forecast FCF (i.e., 1.0% FCF yields).

As a result, it makes sense for patient, long-term investors to set a lower buy-in price by selling out-of-the-money put options.

Shorting OTM KHC Puts

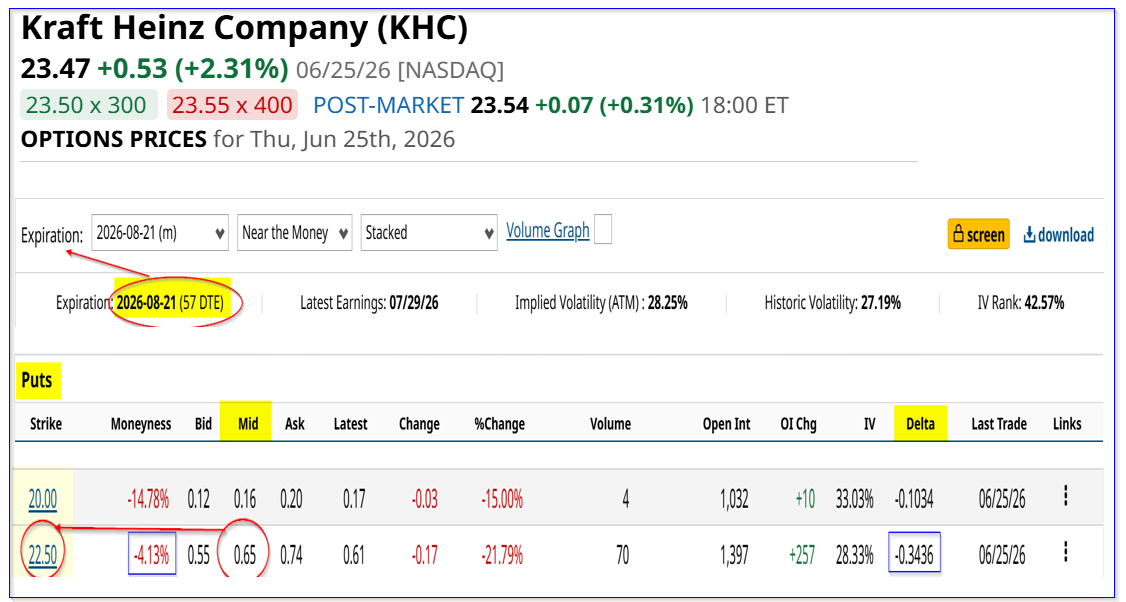

For example, look at the August 21, 2026, expiry period option chain. That is about two months from today. It shows that the $22.50 put option strike price, just over 4% below KHC's trading price, has a 65-cent put option premium.

That implies a short-seller of this put strike price can earn a two-month income yield of 2.889% (i.e., $0.65/$22.50 - 0.02889).

How To Do This

Here is what this means from a practical standpoint.

First, the investor posts $2,250 in cash or buying power with their brokerage firm. This acts as collateral to potentially buy 100 shares at $22.50. Then, the investor can enter a trading order to “Sell to Open” 1 put contract at $22.50 per share.

This allows the investor's account to immediately receive $65.00 (i.e., $0.65 x 100 shares per put contract).

Lower Breakeven Point

So, for the next two months, as long as KHC stays over $22.50, the collateral will not be assigned to buy 100 shares at $22.50. But, even if that happens, the investor's account has a lower breakeven point:

$22.50 - $0.65 = $21.85 breakeven

That is 6.9% below its trading price. Note that this strike price has a relatively high delta ratio (34.4%). That implies there is a good chance KHC could drop 4% to $22.50.

The point is that this is a relatively easy way for value investors to set a lower potential buy-in point and, as well, earn income while waiting.

Moreover, if an investor can repeat this trade every 2 months for a year, assuming KHC stays relatively flat, the expected return is attractive:

2.889% x 6 = 17.334% expected return

Theoretically, that's the same as buying KHC stock and seeing it rise to $27.54 per share (i.e., $23.47 x 1.17334). As it turns out, this may be the easiest way to play KHC stock, for patient value investors.

Comments

Log in or sign up to join the conversation.