A Barchart report today shows unusually heavy trading in Oracle Corp (ORCL) put options ahead of its earnings due out next Wednesday, June 10, after the market closes. This may signal investors are bearish on ORCL stock, just as occurred last quarter.

ORCL is at $240.23, down over 3.2% today in midday trading. However, in the past month, ORCL stock has skyrocketed, up +48.8% since April 30 ($161.39). That could be another reason why there is heavy put option buying today.

ORCL stock - last 3 months - Barchart - June 2, 2026

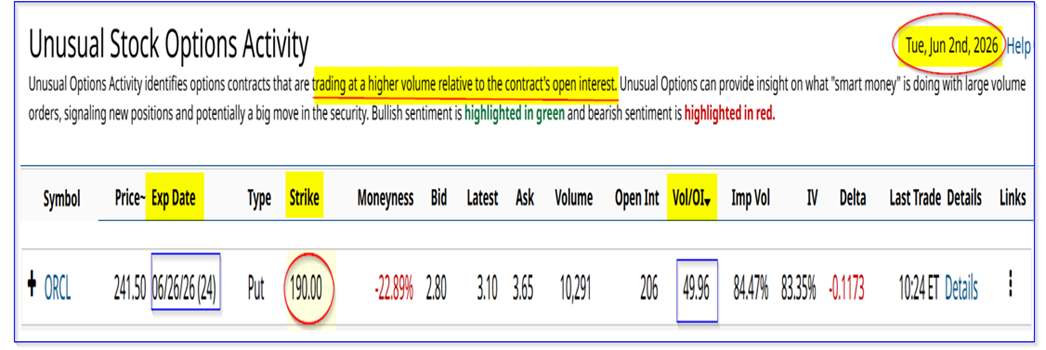

The Barchart Unusual Stock Options Activity Report today shows that almost 50x the normal outstanding number of put contracts have traded. This is for one deep out-of-the-money (OTM) ORCL put option tranche.

The report shows that over 10,000 put contracts have traded for ORCL puts with a $190.00 strike price expiring June 26, i.e., 24 days from now, but after the earnings release date.

ORCL puts expiring June 26 - Barchart Unusual Stock Options Activity Report - June 2, 2026

That strike price is over $50 below today's price, i.e., it is 20.9% "out-of-the-money" or OTM,

$190/$240.23 -1 = -0.209, or 20.9%

Buyers Viewpoint. Note that the premium paid by put option buyers is fairly high: $3.10 at the midpoint. That means ORCL will have to drop to $186.90 before this put contract has any intrinsic value (i.e., $190 - $3.10). That's 22.2% below today's price.

These put option buyers must really expect ORCL to tank in the next 3 weeks. More on this below.

Sellers ViewPoint. However, put option sellers get a nice yield. The $3.10 midpoint premium represents a short-put yield of 1.63%. They post collateral of $19,000 for one put “Sold to Open,” and the account immediately receives $310,

i.e., $310/$19,000 = 1.63%

That's an attractive return: 1.63%, repeated every 24 days for 3 months, represents a 6.11% expected return over that time period, or 2.036% per month.

Moreover, even if ORCL drops to $190, the investors have an attractive buy-in point: $186.90.

Let's look at what might happen.

ORCL's Issues with Free Cash Flow

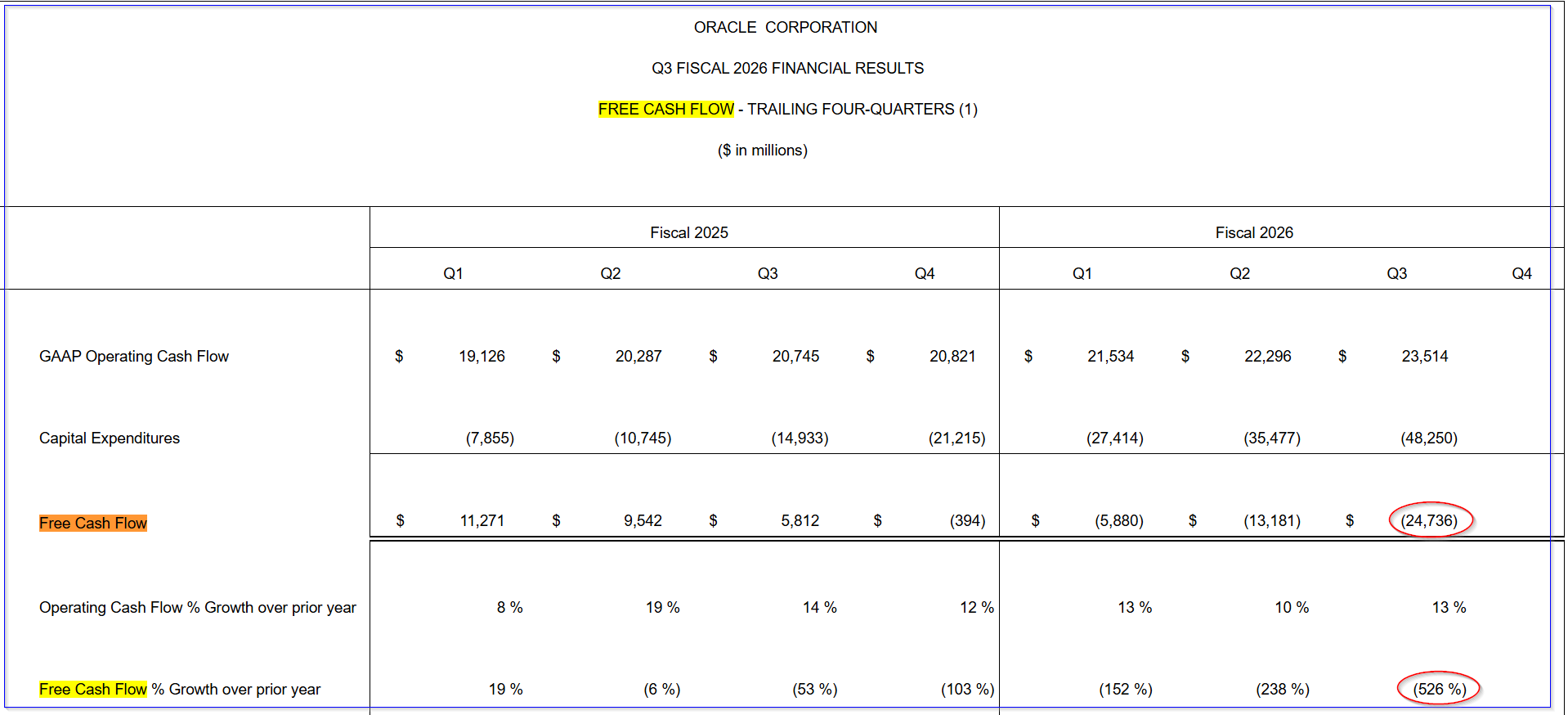

On March 10, Oracle reported a 22% increase in revenue YoY, but its free cash flow (FCF) tanked. For the fiscal Q3 to Feb. 28, it generated an outflow of almost $11.5 billion (i.e., negative FCF).

Moreover, for the trailing 12 months (TTM), which Oracle likes to report, its FCF had a negative outflow of free cash flow (FCF) of $24.736 billion. That was 87.7% worse than the prior quarter's TTM FCF of -$13.181 billion.

This was all due to heavy capex related to its AI initiatives. Moreover, the company is now borrowing heavily to afford these capex.

As a result, ORCL stock tanked over the next month. It fell from an initial rise on March 11 to $163.12 (likely a short-selling cover bump after earnings) to $138.09 a month later on April 10.

That 15.3% drop in ORCL stock could be one reason why there is heavy buying today in Oracle put options expiring on June 26 (see above). However, this assumes that Oracle will continue to show heavy capex related to its AI-related investments.

For example, management said in the March 10 press release that it expects $50 billion in capex this fiscal year to May 31. For the first 3 fiscal quarters to Feb. 28, it had spent $39.17 billion, implying $10.83 billion in Q4 capex. That's just slightly below the $11.484 billion in Q3 capex, according to Stock Analysis.

In other words, Q4 and its TTM FCF are likely to still be very negative.

However, the company has not yet said how much its capex will be in FY 2027 (ending May 31, 2027). It does project, however, a huge increase in revenue (i.e., $90 billion, vs. $67 billion forecast for FY 2026). Let's look at that more closely.

Forecasting FCF

Over the last 12 months to Feb. 28, Oracle generated $23.5 billion in operating cash flow (OCF) - see table above - on $64.077 billion in TTM revenue. That represents an OCF margin of 36.67%.

So, if Oracle can produce $90 billion in FY 2027 revenue, and its OCF margin stays at 37%, it could generate $33 billion in operating cash flow (OCF):

$90b x 0.3667 = $33 billion OCF

Moreover, if its capex stays at a quarterly rate of $10.83 billion, i.e., $43.32 billion annually, negative FCF could fall:

$33b OCF - $43 b capex = -$10b FCF

That also implies that in the following year, as its capex investments yield higher revenue, it could turn FCF positive by FY 2028.

Summary and Conclusion

That could be why the ORCL stock may have bottomed out here. That is also highly speculative.

For example, all of this depends on Oracle's capex flattening out from here. Its upcoming earnings release may shed some light on this. If management indicates that it will have capex over $50 billion next fiscal year, positive FCF could take longer to occur.

That would likely push ORCL stock lower. This shows why investors buying these OTM puts today are betting that it will occur.

Investors should be careful in copying this highly speculative put option purchase. The 1.63% yield for this deep out-of-the-money (OTM) short-put play for 3 weeks is a more conservative play.

Comments

Log in or sign up to join the conversation.