When we talk about inflation, the conversation usually centers on periods (like now) when inflation is especially high. Those are certainly problematic. But we can overlook a possibly bigger problem: other than a few short breaks, you and I have never seen a time when inflation wasn’t rising. Inflation isn’t some problem that pops up occasionally. Inflation has become normal – so normal we let it accumulate for years without complaint.

Think about that for a moment. The Consumer Price Index has risen 28.5% since January 2020 alone. That $100 bill you carried into the grocery store in January 2020 has the purchasing power of $77.82 today. Nobody voted for that.

And it is not just the years since COVID. Go back to 1913, when the Federal Reserve was created with a mandate to ‘maintain price stability.’ A dollar then is worth roughly three cents today. That is a 97% loss of purchasing power in a little over a century. If your bank gave you a savings account that lost 97% of its value over its lifetime, you would call it fraud. When the Federal Reserve does it, we call it monetary policy.

We don’t complain in part because inflation can be convenient for some of us. If we have a mortgage on a home, inflation generally means the home price goes up while the mortgage value stays the same. We like it when the price of assets that we own go up, forgetting that much of that price increase is inflation. It works for assets of all types.

Federal Reserve officials, for example, have long considered 2% inflation kind of handy. It gives them wiggle room to manage the economy the way they want. And since most of the academic economics profession is beholden to the Fed, that belief doesn’t get much pushback.

I don’t owe the Fed anything, so I’m free to push back. And I’m hopeful new chair Kevin Warsh will help change the Fed’s inflation-tolerating institutional culture. Early signs look positive. Today we’ll talk about how insidious inflation is and why those who think a little inflation is fine should have their heads examined. It is not fine… for anyone.

Compound Inflation

Let’s begin with a little math. Albert Einstein, who knew more than a little math, famously called compound interest “the most powerful force in the universe” (or words to that effect). This force unfortunately applies to inflation, too.

A 2% inflation target may sound small. Over time, it is not small. Ten years of 2% inflation adds up to 21.9% higher prices. Twenty years means the cost of living is 48.6% more expensive than it would have been without inflation.

Or, looking at it from the other direction, at 2% inflation the $100 you started with shrinks to $82.03 in 10 years and $67.30 in 20 years. That is not small, particularly since a 2% ‘official’ inflation rate probably understates actual inflation for most people.

Except we haven’t been living at 2% inflation. We have been living at 3%, 4%, and in some categories far higher. At the Fed’s preferred PCE measure, inflation ran at 4.1% year-over-year as of this week.

Yes, energy was a big part, and it will come down (hopefully). An outlier? Not really lately. Since January 2020, U.S. prices have risen approximately 25%, reflecting an average annual inflation rate of around 6% over this period.

Run 4% inflation for 20 years and your $100 becomes $46 in real purchasing power. Half. Gone. And since January 2020 alone, cumulative CPI inflation has already reached 28.5%. If your household income hasn’t kept up with that, you are poorer than you were five years ago. The math is not ambiguous.

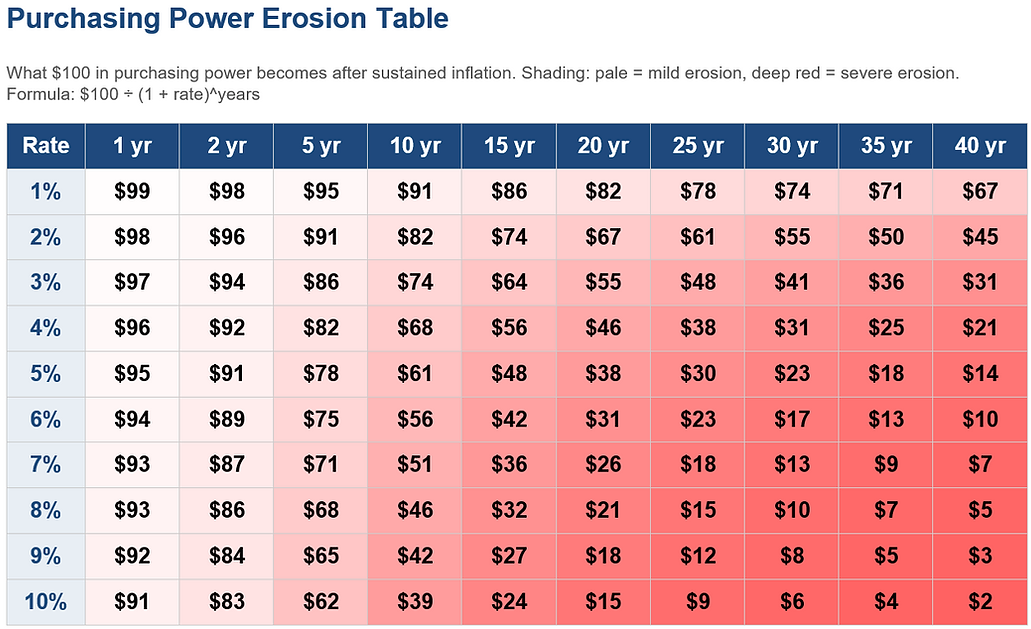

Here is a table that shows the effect of inflation over time. I show inflation rates and a year. While those of us in the US may say that won’t happen, there are many readers in many countries who have seen just that and more.

Source: Mauldin Economics

Yet as of now, 2% remains the Fed’s official goal. This month’s FOMC statement (first of the Warsh era) reiterated that point. But it also explicitly noted that inflation remains elevated relative to that goal. And the very last sentence was a flat-out promise of change: “The Committee will deliver price stability.”

Those are the most beautiful six words of any FOMC press release in my life. The market has placed an over 85% chance of at least one rate hike by the end of the year. Since I highly doubt that there will be a rate hike prior to the election, a rate hike would come at the December FOMC meeting.

As the above math shows, 2% inflation is not price stability. Warsh will have to change the FOMC’s target if he wants to deliver on that promise. Convincing the other members will probably take some time. But given this statement drew no dissents, maybe they are closer than we think. Warsh, at least, seems to understand how evil even 2% inflation rates are.

Who is Kevin Warsh, and why does his inflation focus matter? Warsh served on the Fed board of governors from 2006 to 2011. He was the youngest person ever appointed to that post. More importantly, he was one of the few voices inside the Fed warning that the post-2008 quantitative easing experiment would eventually create inflation problems. He resigned in 2011, partly out of frustration that his warnings were dismissed.

He has spent the years since writing and speaking about the need for the Fed to return to sound money principles. When he testified before the Senate Banking Committee for his confirmation as chair, he made clear that restoring the Fed’s credibility on inflation was his “north star.” I believed him then. I still believe him. Whether he can move a committee of 12 in that direction is a different question.

The Grocery Store Never Lies

There is no better place to feel inflation than a grocery store. Abstract economic statistics can be argued, revised, and seasonally adjusted into relative harmlessness. The checkout line cannot. According to FRED data from the Bureau of Labor Statistics, the CPI for food at home — groceries — rose 37.9% between January 2020 and March 2026. That is more than one-third more expensive for the same cart of food in six years.

The specific numbers are striking. Eggs have become a cultural flashpoint, with prices periodically tripling from pre-pandemic norms due to a combination of avian flu outbreaks, feed cost inflation, and supply chain disruptions. Ground beef is up roughly 30% from 2020 levels. Bread, butter, and cooking oils have all seen sustained double-digit increases. And while some individual item prices have pulled back from peak levels, the overall level of grocery prices has not. It has simply stopped going up as fast. That is not the same thing as relief.

Then there is shrinkflation, which is inflation’s sneakier cousin. Your bag of chips that used to weigh 16 ounces now weighs 13.5 ounces, same shelf price, less product. Your can of tuna that held 6 ounces now holds 5. The Brewers Association has documented the phenomenon in packaged goods across dozens of categories. The Bureau of Labor Statistics tries to adjust for this, but consumers feel it directly even when the statistics don’t fully capture it. Shrinkflation is inflation with a disguise.

Food inflation is also deeply regressive. A family spending $400 a month on groceries and a family spending $1,200 a month both face the same percentage increase. But for the lower-income family, that $150 in extra monthly grocery costs represents a much larger share of their budget. The USDA’s food security surveys show that the share of Americans who are food insecure, meaning they sometimes don’t have enough to eat, increased meaningfully during the inflation surge of 2021–2023. Those are real people, not data points.

“More Expensive in Every Way”

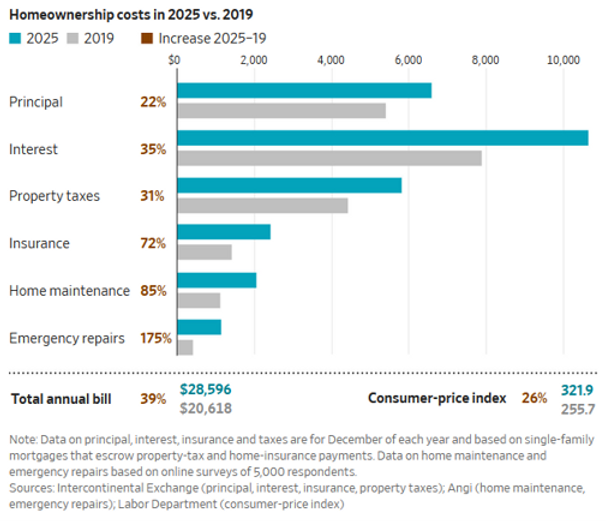

Housing costs are the biggest inflation burden for many American families, though not necessarily the most obvious. Homeowners with fixed rate mortgages don’t experience higher payments in the same way renters can see their monthly costs go up at renewal every year or two.

Yet principal and interest payments aren’t the only costs of homeownership. There’s also insurance, property taxes, HOA fees, routine maintenance and emergency repairs. These are a growing challenge. A recent Wall Street Journal report showed the all-in costs rose almost 40% between 2019 and 2025. It was appropriately headlined, “See How Owning a Home is Getting More Expensive in Every Way.”

Source: The Wall Street Journal

Percentage wise, repairs and maintenance are the fastest growing costs, followed by insurance. All three of those have a lot to do with construction material and labor cost inflation. According to survey data from Angi, the average household spent almost $12,500 on home improvement, maintenance and emergency repairs last year. Many spent much more.

The homeowner insurance crisis deserves special attention. Across Florida, California, Louisiana, and increasingly Texas and the Gulf states, major insurers have stopped writing new policies or exited the market entirely. State Farm, Allstate (ALL), and Farmers have all pulled back from high-risk markets. Homeowners who can still find coverage are seeing premiums double and triple. The American Property Casualty Insurance Association reported that homeowners’ insurance underwriting losses exceeded $15 billion in 2023, a trend that has continued. This isn’t speculation about the future. It’s happening now, in markets that represent tens of millions of American homeowners.

Higher mortgage rates are an even bigger culprit. They made a big jump in 2022 and have held in the roughly 6% zone ever since. WSJ notes this makes a huge difference in purchasing power.

“A buyer with a $2,500 monthly budget and a 20% down payment can afford to buy a $517,500 home at a 3% mortgage rate, according to real-estate brokerage Redfin. At today’s rate around 6.5%, that same buyer can only afford a $384,000 home.”

This is why so many homes aren’t selling. The number of buyers who can afford to pay the prices sellers want (and often need) to get is limited. And that’s if you assume all the other stars line up: the home is in a desirable community, local policies are friendly and so on. This is not always the case… even if the sellers don’t want to admit it.

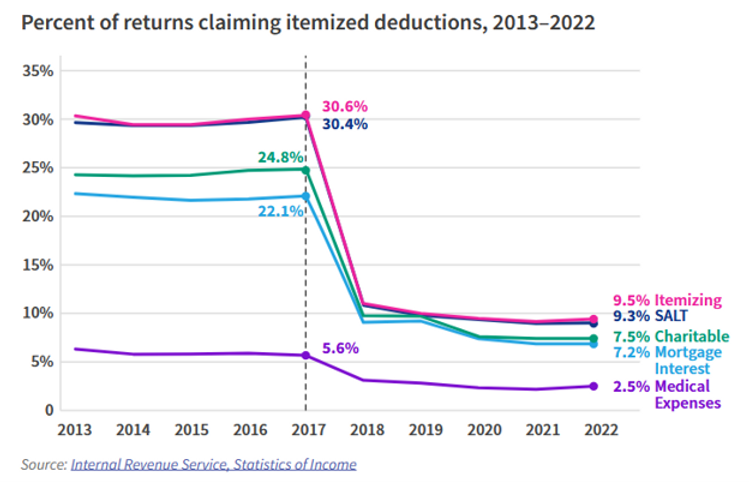

But there’s another, less noticed factor in housing prices. Homeownership used to be heavily subsidized by tax policy, i.e. the mortgage interest deduction. Getting that help requires you to itemize deductions. This became much less common after the 2017 tax cuts raised the standard deduction for everyone.

Source: USAFacts

In effect, the extra tax deduction that once went only to homeowners is now available to everyone. Did it make a huge difference? Maybe not, but it made some difference. Now it doesn’t.

What happens when a once-subsidized industry loses its subsidy? Supply falls and prices will rise unless demand also declines. To be clear, the tax cuts were good and helpful in other ways. But they were also inflationary for housing prices.

The idea that inflation helps debtors, while true, misses the fact that the cost simply gets transferred to someone else – namely lenders. That doesn’t mean faceless institutions. The underlying lenders in today’s economy are frequently retirees and others who own bonds or bond funds. They depend on their interest income to pay their own bills. Reduce the burden on homeowners and you also reduce the older generation’s spending power. This trickles through the economy.

Let me be direct about who inflation hurts most. It is not the wealthy, who own real assets that inflation often inflates right along with everything else. It is not even, primarily, working-age people with job skills they can leverage into higher wages. Inflation’s cruelest victims are retirees and others on fixed incomes. Social Security’s COLA adjustments, the cost-of-living increases, are based on the CPI. But as many retirees have noticed, the CPI basket doesn’t look much like how a 72-year-old actually spends money. Healthcare and housing consume a much larger share of a retiree’s budget than the CPI weights suggest. A 2022 study by The Senior Citizens League found that Social Security benefits had lost 36% of their purchasing power since 2000. That is not a small number for someone living on a fixed benefit check. Nobody at the Fed is optimizing policy for them.

And it is just as insidious for lower income families, who work in jobs that need less skill and lower pay.

Can AI Help?

Financial markets are beginning to anticipate inflation no matter what. Here’s Apollo’s Torsten Slok last week.

“The narrative in markets is changing from ‘lower oil prices mean lower inflation’ to ‘lower oil prices mean more demand in an already overheating economy, which means higher inflation.’

“This breakdown in the correlation between rates and oil prices can be seen in the chart below.

“Driven by the strong April CPI, hot May non-farm payrolls and a hawkish Fed, the market narrative now suggests that the reopening of the Strait of Hormuz will further overheat the economy, forcing the Fed to raise interest rates soon.”

Source: Apollo

The scariest part about inflation is it becomes self-generating. Prices rise until consumers and businesses begin expecting prices to rise, which then allows prices to rise even more. We seem to be reaching that point.

The University of Michigan’s Consumer Sentiment Survey shows long-run inflation expectations — the 5-to-10-year outlook — rising to levels not seen in decades. That matters enormously. When workers expect 4% inflation, they demand 5% wage increases to stay ahead. When businesses expect input costs to keep rising, they raise prices preemptively. When landlords expect rents to rise, they bake it into lease renewals. This is the wage-price spiral that Fed chair Arthur Burns failed to contain in the 1970s and that Paul Volcker eventually broke only by driving interest rates above 20%, unemployment to 10.8% and sending the economy into severe recession. Nobody wants to repeat that. Which is why inflation expectations cannot be allowed to become unmoored. Warsh understands this, I believe. The question is whether he acts quickly enough.

All that said, there are other possibilities. To borrow the old math joke format, is AI inflationary or deflationary? Yes.

The argument that AI will be deflationary over the long term makes a lot of sense. Higher productivity and improving inefficient business processes will give businesses room to cut the price of many goods and services. But before we get there, the extraordinary costs make the AI buildout itself inflationary.

I discussed this with Ken Rogoff earlier this year. Prior technological shifts took generations to play out, giving workers time to adapt. AI won't give us that luxury. If an AI system can reliably do the work of a $200,000-a-year research associate, the baseline value of certain knowledge work changes overnight. This is what Joseph Schumpeter called “creative destruction.” It is going to create massive opportunities, but the transition will be difficult for people who aren't prepared.

Comments

Log in or sign up to join the conversation.