Key Market Outlook(s) and Pick(s)

On Monday, I joined Lauren Simonetti on Fox Business’ Mornings with Maria to discuss markets, the economy, outlook, rotation, Iran, the Fed, and more. Thanks to Maria Bartiromo, Cassie Loeloff, and Lauren for having me on.

On Tuesday, I joined the amazing Liz Claman on Fox Business’ The Claman Countdown to discuss markets, the economy, outlook, rotation, positioning, the consumer, PayPal (PYPL), Etsy (ETSY), and more. Thanks to Liz, Brooke Haliscak, and Jake Mack for having me on.

On Wednesday, I joined the great David Asman on Fox Business’ Varney & Co. to discuss markets, the economy, outlook, SpaceX (SPCX), Dentsply Sirona (XRAY), VF Corp (VFC), and a lot more. Thanks to Stuart Varney, Maggie Edwards, and David for having me on.

This week, I joined Phil Rosen on the Full Signal podcast to discuss markets, the economy, outlook, rotation, PYPL, VFC, ETSY, XRAY, and more. Thanks to Phil for having me on.

On Monday, I joined Lance Glinn on NYSE TV to discuss markets, the economy, outlook, rotation, positioning, Iran, the Fed, and more. Thanks to Lance and Mel Montanez for having me on.

On Tuesday, I joined Diane King Hall on the Schwab Network to discuss markets, the economy, outlook, positioning, rotation, the consumer, Baxter (BAX), Hormel (HRL), and more. Thanks to Diane and Kaitlyn Crist for having me on.

Bank of America (BAC) Fund Manager Survey Update

On Tuesday, we put out a summary of the monthly Bank of America Global Fund Manager Survey. This month, they surveyed 200 institutional managers with ~$517B in AUM:

Here were the 5 key points:

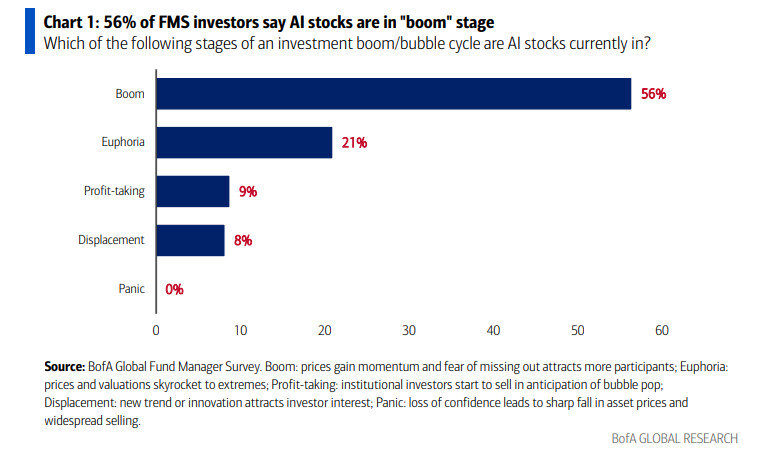

1) 56% of fund managers now describe AI stocks as being in the “boom” phase of the cycle, where momentum accelerates and FOMO draws in new buyers. Just 21% characterize the environment as euphoric, while not a single respondent views the trade as being in panic territory. We largely agree and continue to view AI as being closer to the middle innings than the ninth. That said, the trade appears increasingly due for a breather. With internal cash flow running dry and debt markets bumping against their practical ceiling, hyperscalers have transitioned from net buyers of their own stock to net sellers for the first time in many years, leaning more heavily on equity issuance to finance the AI arms race. The day management teams begin walking back capital spending commitments, potentially later this year if funding demand weakens, is when the real bargains will begin to surface in the AI trade. Until then, we continue to see better uses per dollar of capital in the neglected corners of the market, namely consumer-facing businesses and “boring” defensive names.

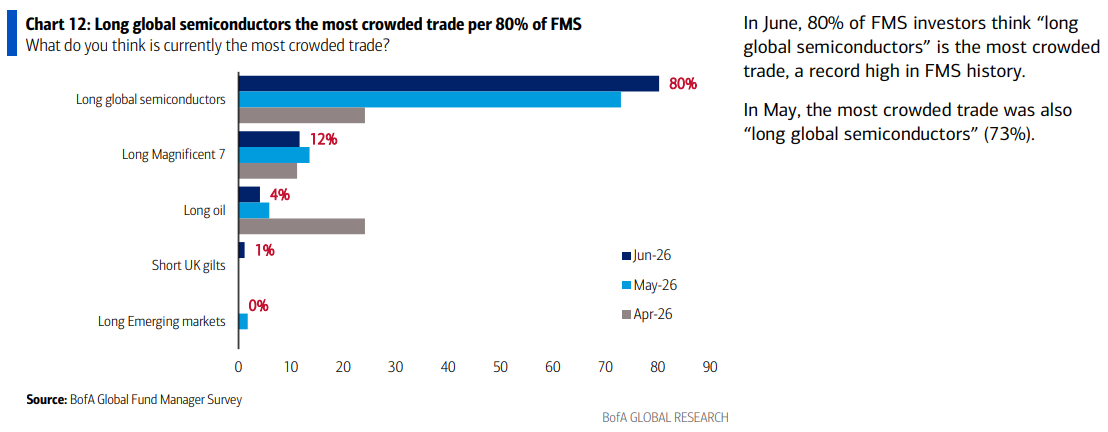

2) At a record 80%, “long global semiconductors” has become the most crowded trade in Fund Manager Survey history, up from 73% in May and dwarfing the next most crowded positions, long Mag 7 at 12% and long oil at 4%. When four out of five fund managers identify the same trade as overcrowded, that perception alone can become a self-fulfilling headwind and limit incremental upside.

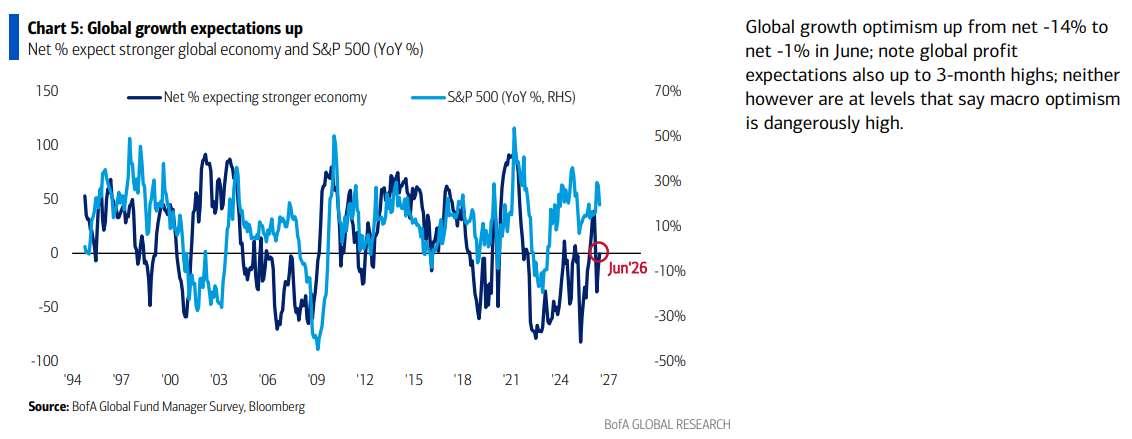

3) Global growth optimism climbed from a net -14% to a net -1% in June, with global profit expectations pushing to three-month highs, yet both readings remain near neutral territory and leave plenty of room for sentiment to improve further. With energy prices rolling over, inflation expectations easing, and rate hike expectations shifting back toward cuts, conditions remain ripe for the “everything trade” and the return of the prewar playbook we have been pounding the table on, setting the stage for a broadening rally that takes the torch from narrow AI leadership.

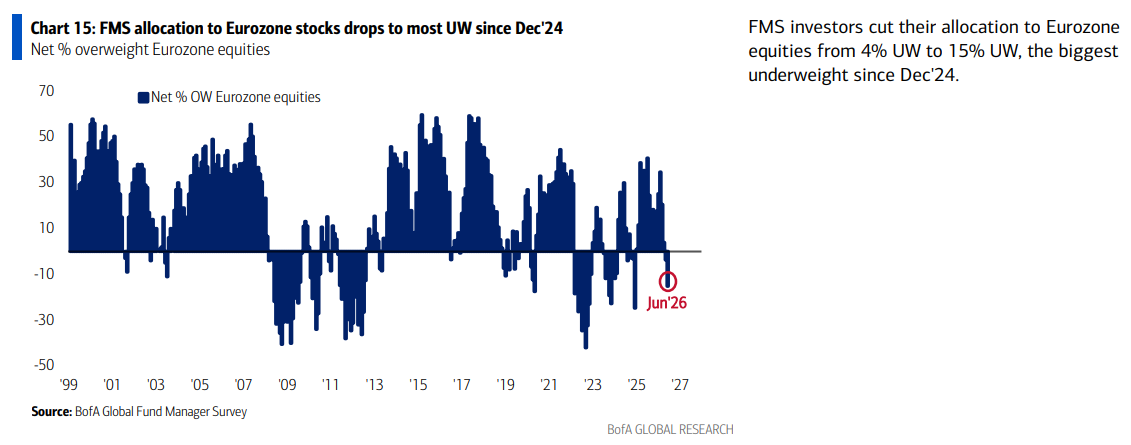

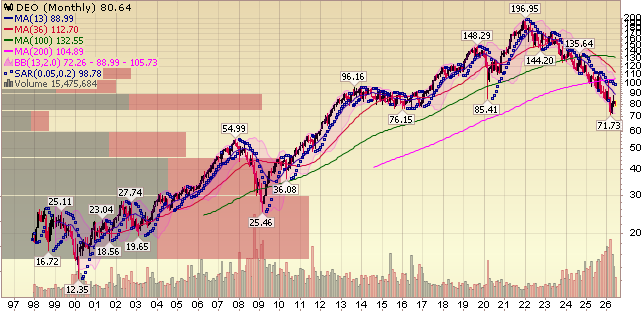

4) Fund managers slashed their Eurozone equity allocation from a net 4% underweight last month to a net 15% underweight in June, marking the largest underweight position since December 2024. Europe is being left for dead once again, which is precisely when investors should start paying attention. We remain constructive on both European equities and the broader weaker-dollar thesis, expressed through European holdings such as Diageo (DEO) and U.S. multinationals with heavy European revenue exposure like GXO (GXO), Estée Lauder (EL), and Dentsply.

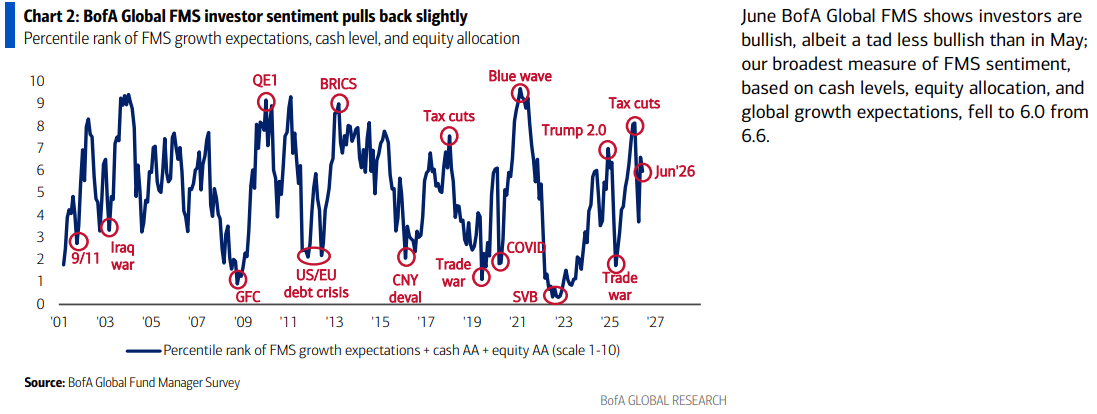

5) BofA’s broadest sentiment gauge, which combines cash levels, equity allocations, and global growth expectations, declined modestly to 6.0 in June from 6.6 in May. While sentiment certainly remains elevated, it is still well below the stretched levels that have historically accompanied major market tops.

Diageo Update

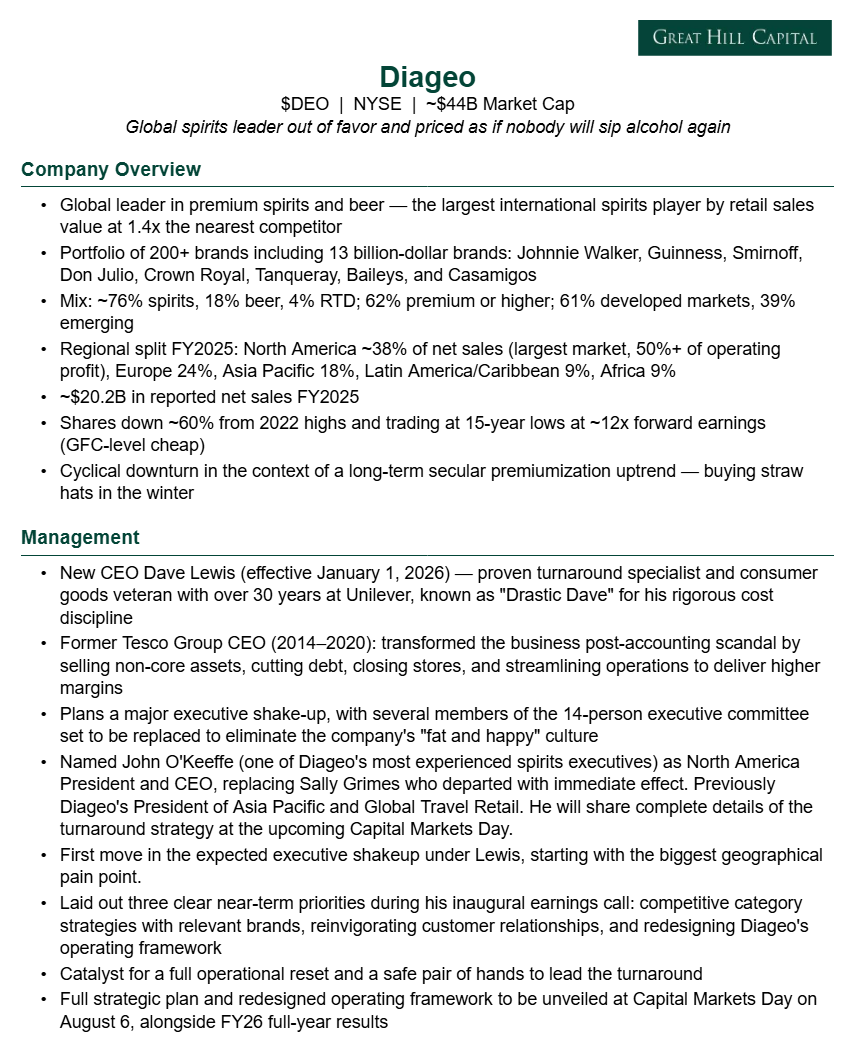

For newer readers, here’s a brief overview of the key drivers behind our thesis on Diageo, the world’s largest premium spirits company priced as if nobody will ever sip alcohol again as the market mistakes a cyclical hangover for permanent impairment:

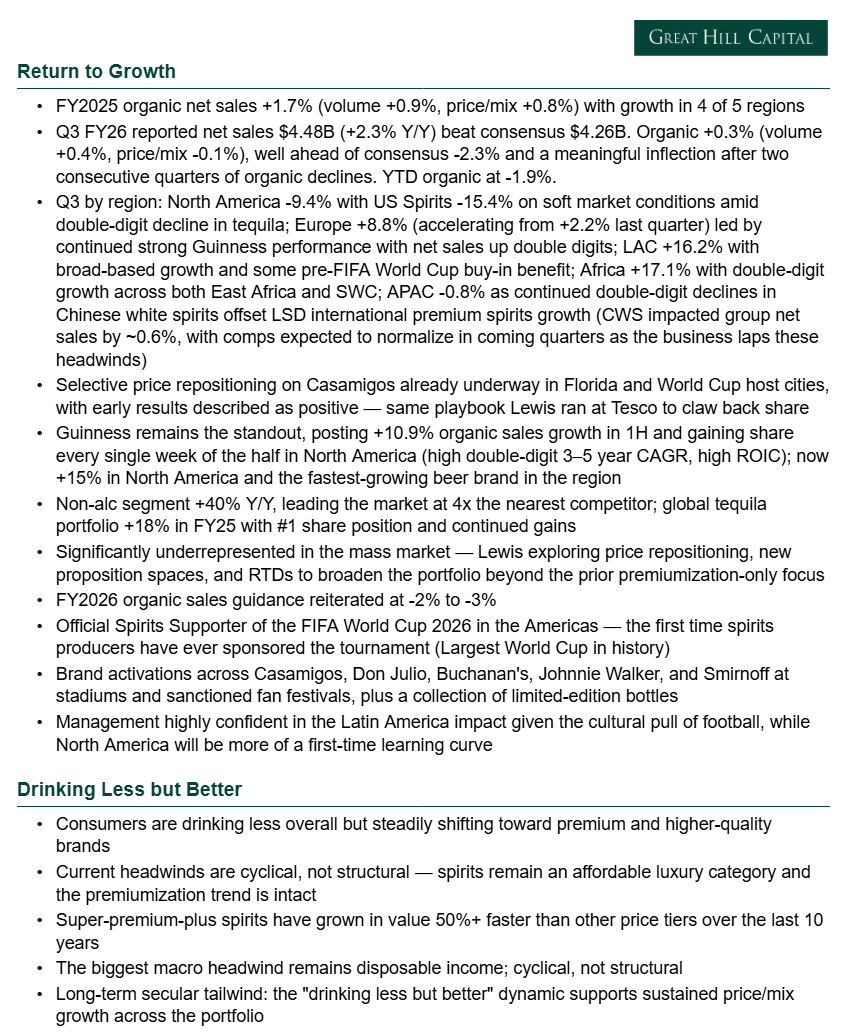

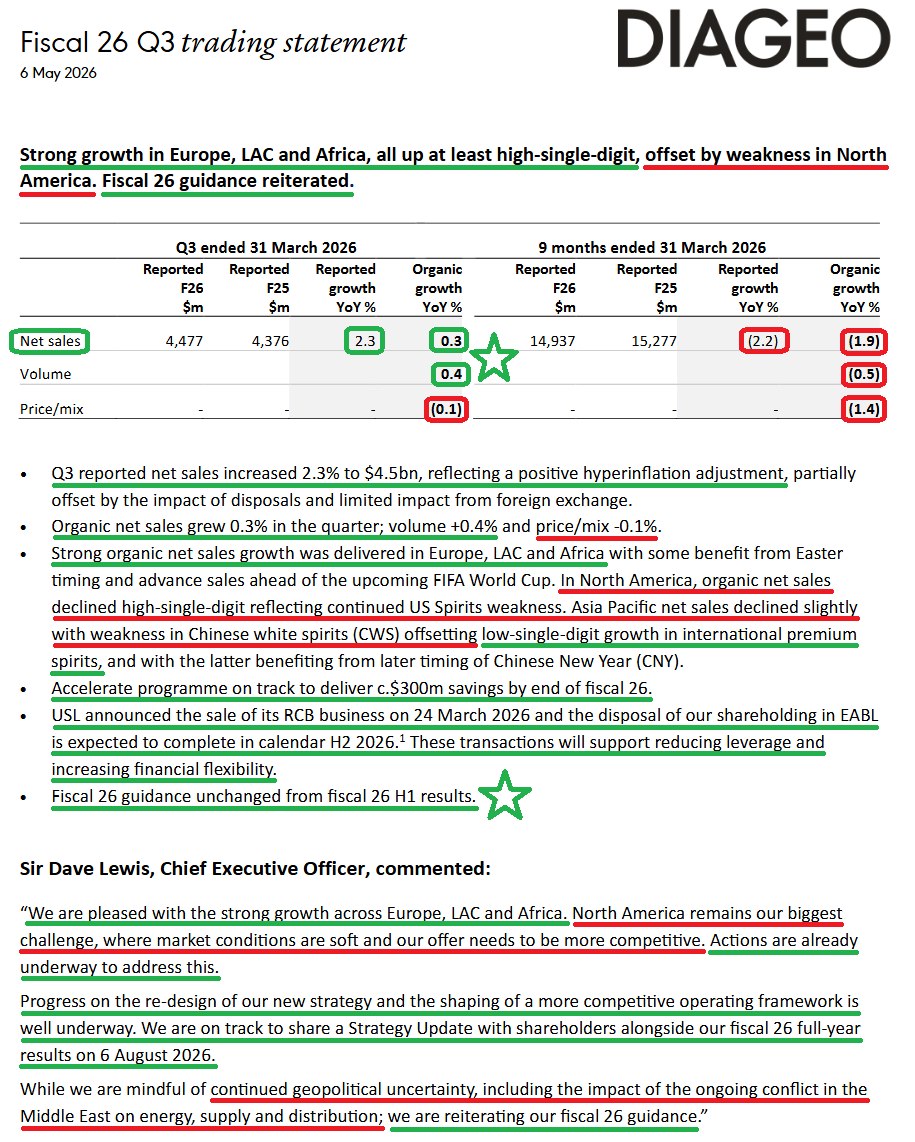

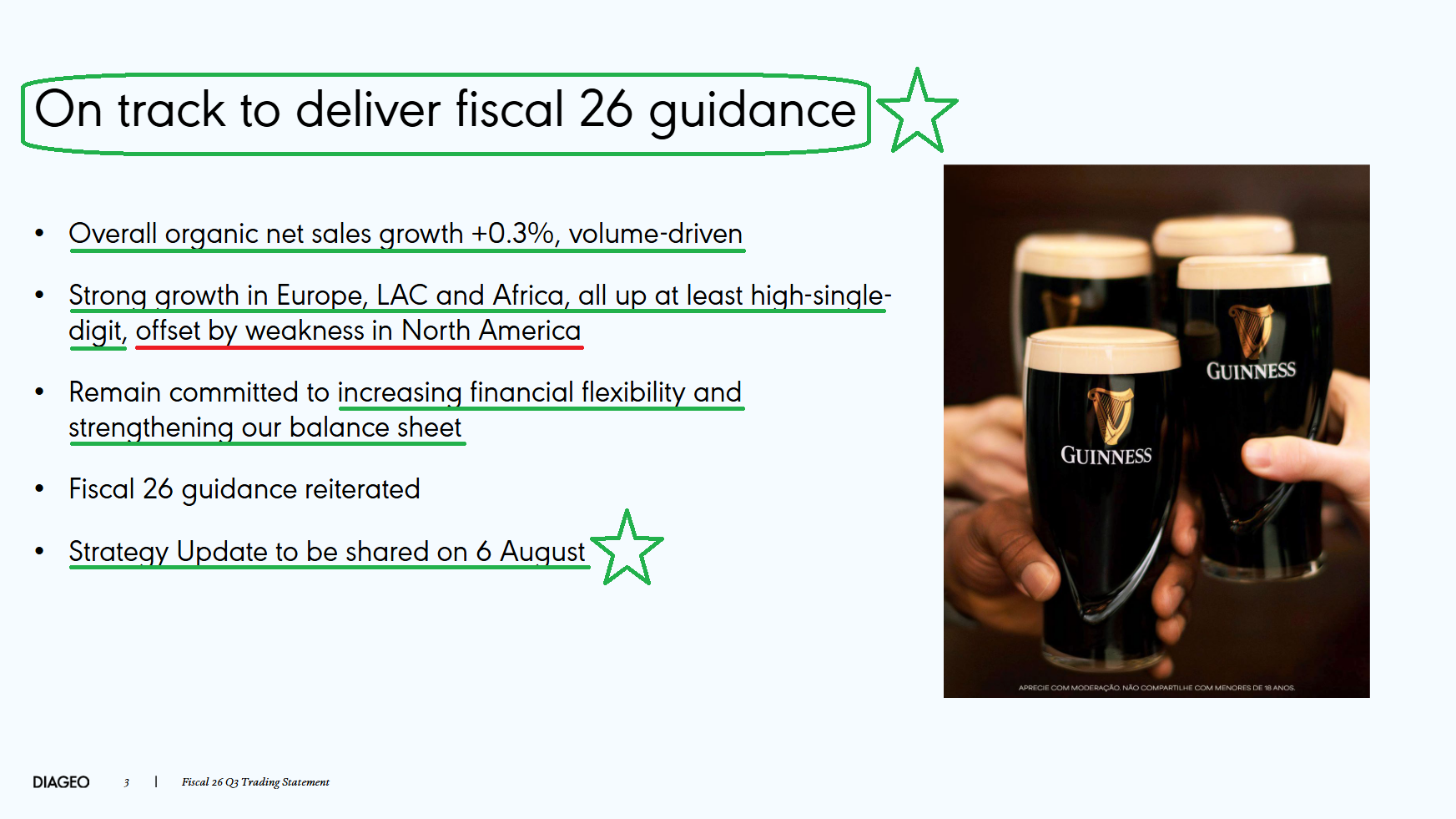

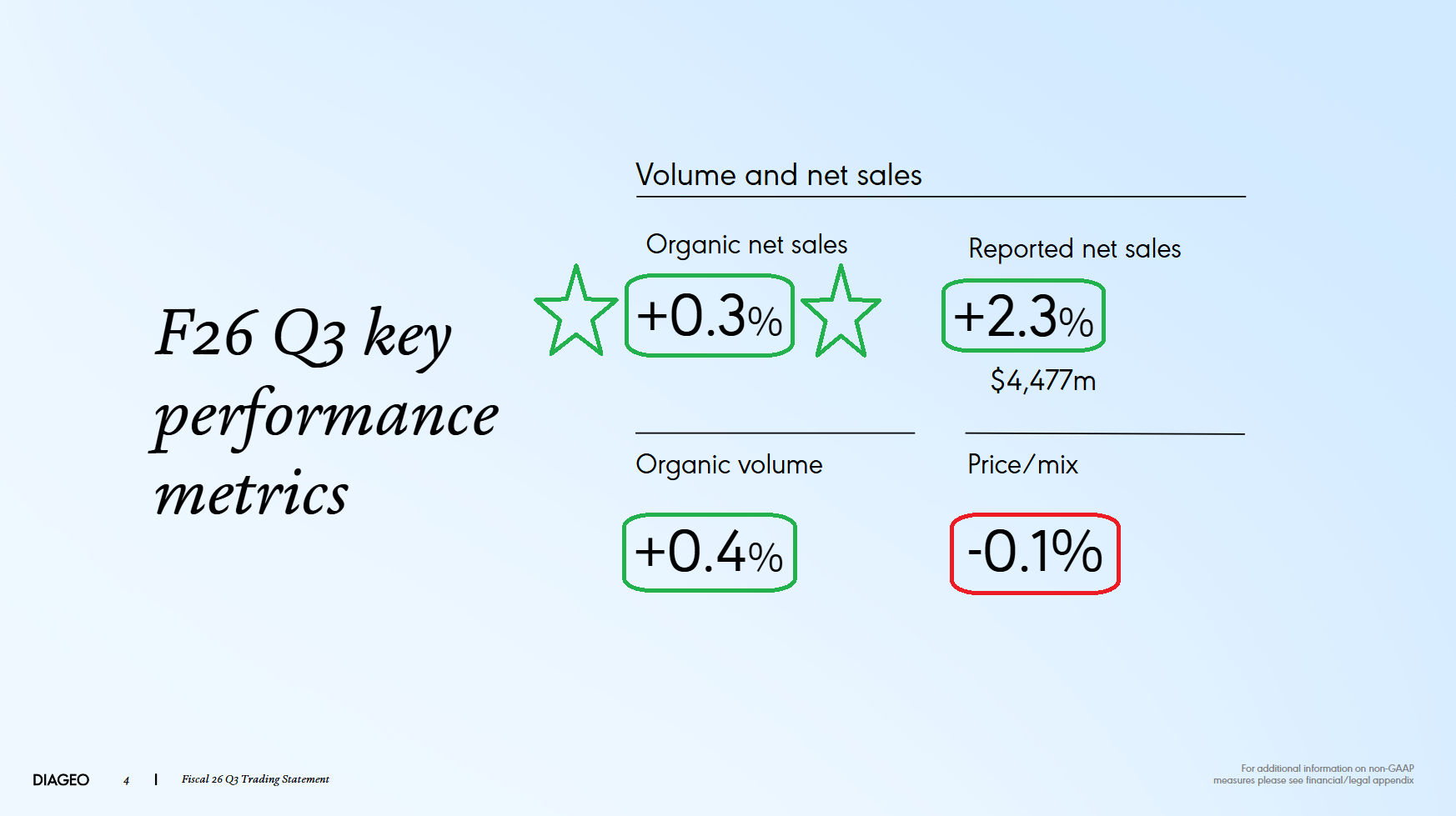

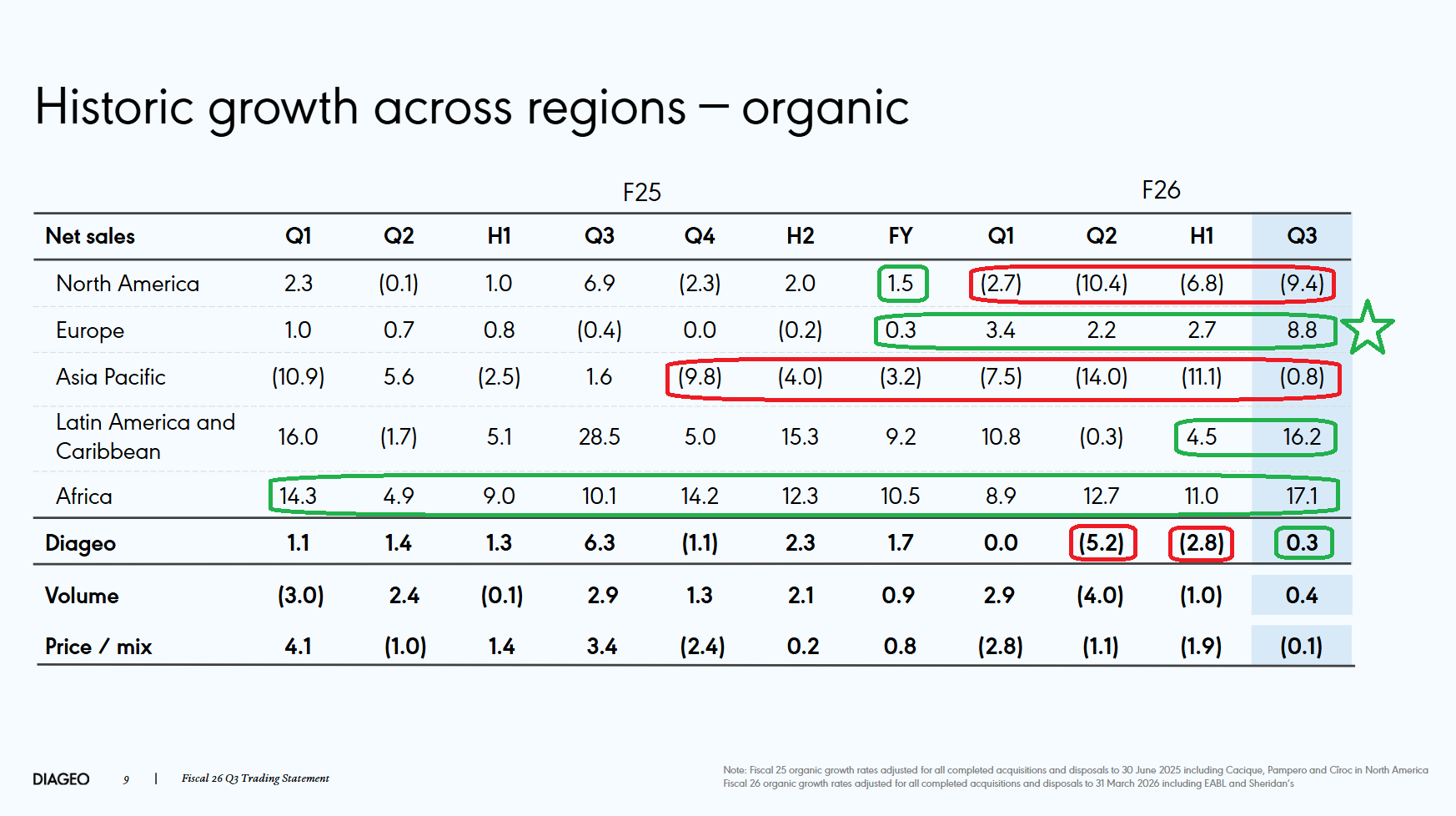

After booking the initial kitchen-sink quarter where new CEO Dave Lewis cut the dividend and aired every shortfall under prior management to reset expectations, it took just one quarter for the first green shoots to emerge. Diageo’s Q3 FY26 results snapped a two-quarter run of weak organic growth (Q2 -5.2%, Q1 flat), with organic net sales rising +0.3%, well ahead of the -2.3% decline feared by consensus.

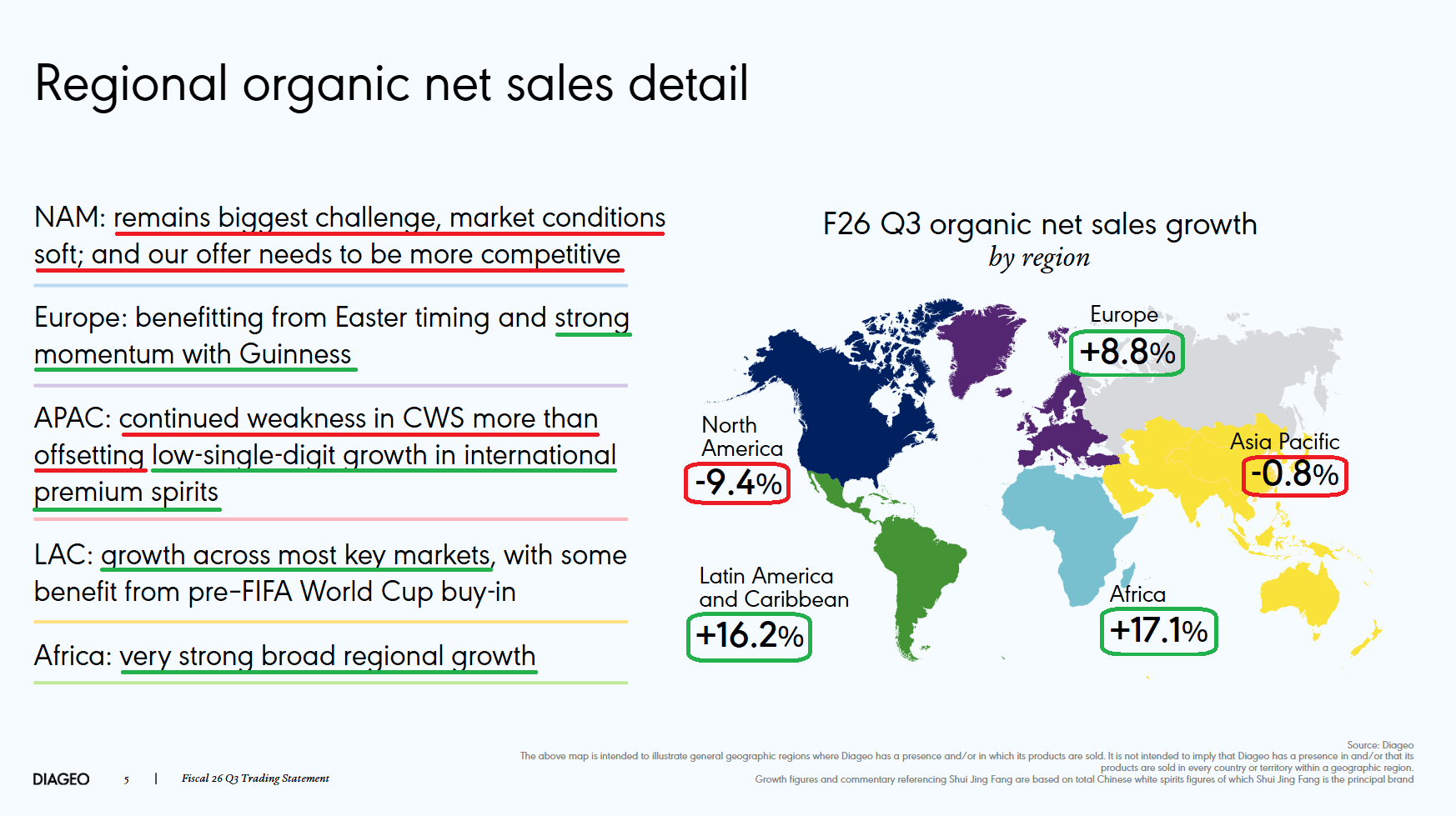

Strength was broad-based across the portfolio, with three of five regions delivering at least high-single-digit organic growth. Europe led the charge at +8.8%, accelerating from +2.2% last quarter, driven largely by continued double-digit growth in Guinness across Great Britain and Ireland. At a time when most beer players are struggling to find a pulse, Guinness remains a bright spot as the fastest-growing major beer brand in the world. Management expects that momentum to continue into the back half and beyond as new capacity comes online across both its largest markets and those where penetration remains relatively low.

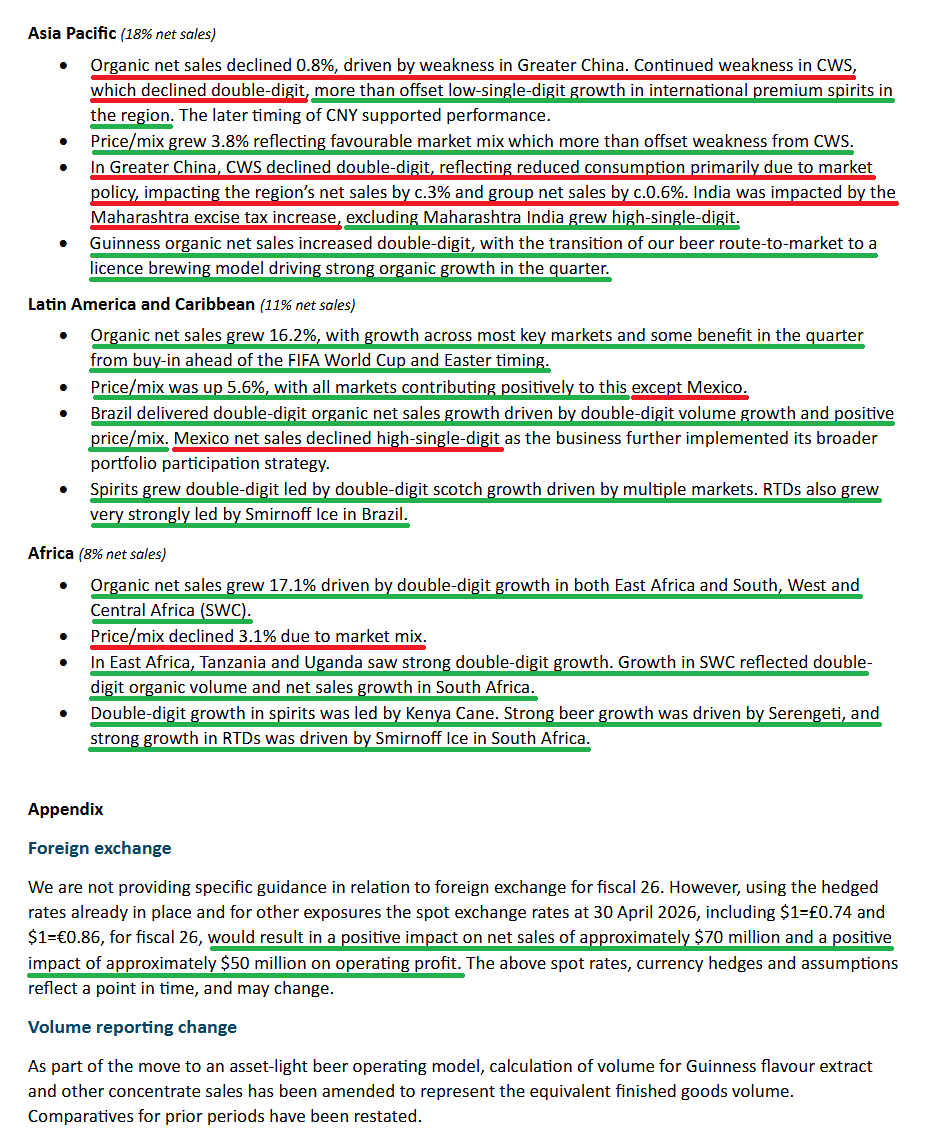

Beyond Europe, Latin America and the Caribbean grew +16.2% on broad-based strength and some early FIFA World Cup buy-in, while Africa posted +17.1% growth, driven by double-digit gains across both East Africa and South, West and Central Africa. APAC declined a modest -0.8%, with the weakness largely outside of Diageo’s control. A shift in Chinese government policy drove a >20% decline in Chinese white spirits, masking what was otherwise a healthy quarter that saw low-single-digit growth in international premium spirits. As those policy headwinds are lapped over the coming quarters, the underlying strength of the APAC story should begin to re-emerge.

That leaves North America as the final pain point left to address. At ~38% of net sales and more than 50% of operating profit, this remains the engine of the business and the heart of the DEO turnaround story. On that front, there is still plenty of work to be done, with North America organic sales declining -9.4% as the U.S. spirits portfolio fell -15.4%, driven by another quarter of double-digit declines in tequila.

Unlike prior management, Lewis isn’t the type to sit on his hands, make excuses, and wait for the macro to bail him out. Under his leadership, Diageo is back on offense, focusing on the levers within its control rather than simply riding out the cycle in its largest market.

The plan to fix North America is already underway across three fronts:

First is an executive overhaul that has installed John O’Keeffe, one of Diageo’s most experienced spirits executives, as North America CEO, alongside the planned departure of the North America CMO and additional changes across the senior leadership team.

Second, selective price repositioning across the portfolio to better target the mass market, an area that had been largely neglected under prior management. In many cases, Diageo’s own brands within its 200+ brand portfolio were effectively competing with one another at the premium end of the market. The first example of this repositioning is already playing out with Casamigos in Florida and other key World Cup host cities, where early results have reportedly been highly encouraging. These are still the early innings of the same playbook Lewis ran at Tesco: narrow price gaps, recapture share, and allow volume growth to more than offset modest margin pressure.

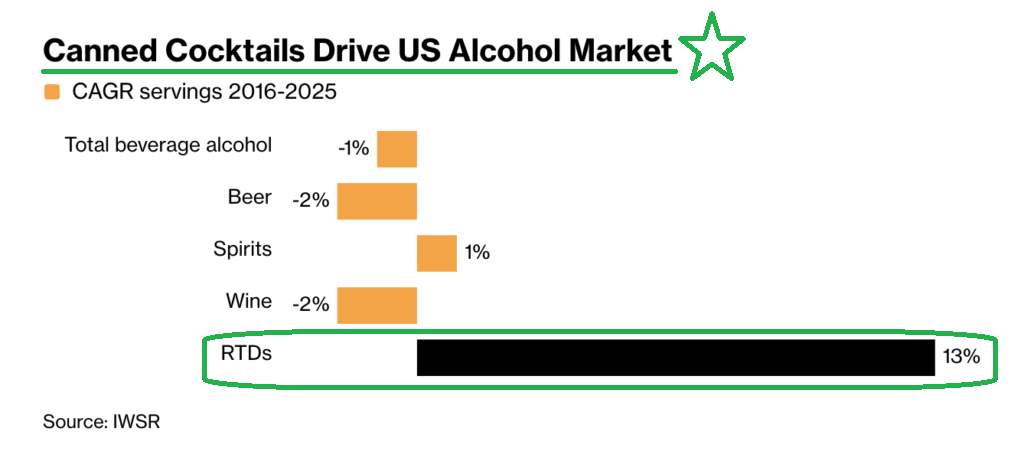

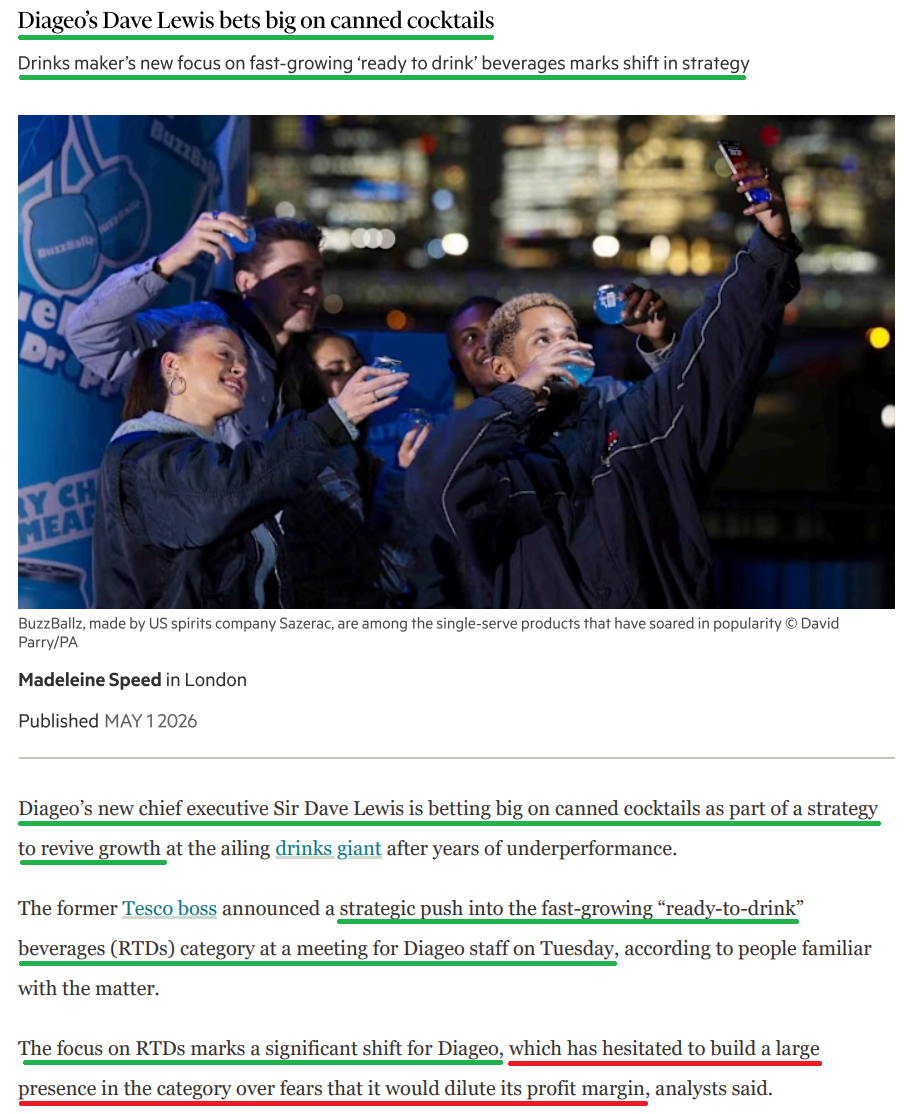

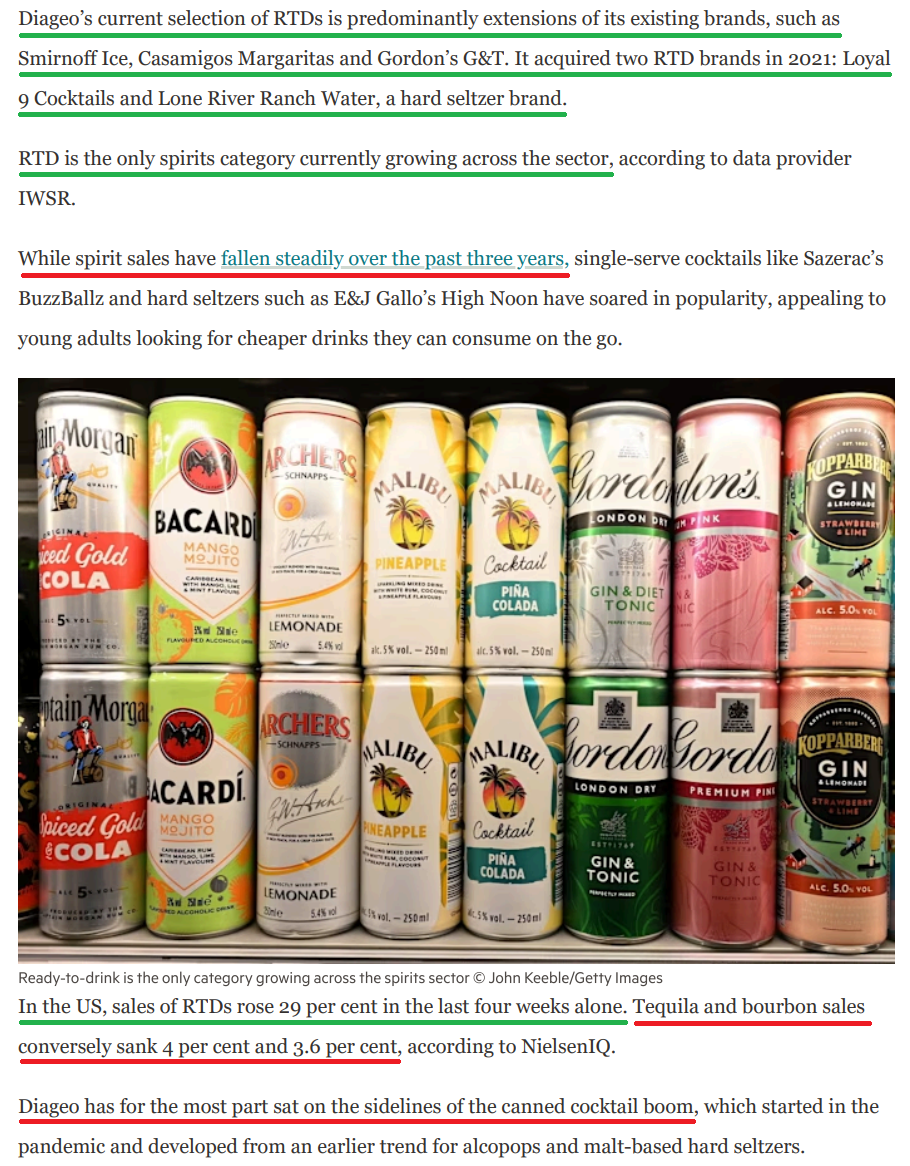

Third, and perhaps most strategically important, is a long-overdue push into ready-to-drink (RTD) cocktails. Canned cocktails are one of the few categories driving growth in the U.S. market today, and Diageo has largely been sitting on the sidelines. This was an area effectively abandoned under prior management’s pursuit of premiumization at all costs, largely due to concerns around margin dilution. Yet RTDs have been the standout performer through the broader alcohol downturn, growing at a 13% CAGR since 2016 versus beer at -2%, spirits at +1%, and total beverage alcohol at -1%. We expect that to change under Lewis, with a formal RTD strategy likely to be unveiled at the upcoming Capital Markets Day.

Layered on top of these self-help initiatives is what may be the most important near-term catalyst of all: the FIFA World Cup.

Diageo will serve as the Official Spirits Supporter in the Americas, marking the first time a spirits producer has ever sponsored the tournament. With 104 matches played over six weeks versus 64 in prior tournaments, this will be the largest World Cup in history. And with more games comes more alcohol. Industry estimates suggest the expanded format could drive more than 1 billion incremental pints of beer consumed over the course of the tournament.

Guinness, as the world’s fastest-growing major beer brand, should capture more than its fair share of that demand, while activations across Casamigos, Don Julio, Buchanan’s, Johnnie Walker, and Smirnoff at stadiums and fan festivals will place these brands directly in front of consumers at scale. If executed properly, this is the type of catalyst that can drive momentum well beyond the tournament and the current quarter.

Looking beyond the World Cup, the long-awaited Capital Markets Day is scheduled for August 6, when Lewis is expected to unveil the company’s full strategic roadmap and redesigned operating framework alongside FY26 results. After several years of strategic drift and underwhelming execution, this is the reset investors have been waiting for.

Just two quarters into his tenure, Lewis is already providing the first tangible evidence that our cyclical-not-structural call is beginning to play out. At the end of the day, this remains the highest-quality name in global spirits, supported by a portfolio of iconic brands, industry-leading margins, and now a proven turnaround operator at the helm.

While the voting machine remains focused on near-term noise, we’re more than content to let the weighing machine catch up to the earnings power this business is capable of generating on the other side of the current downturn.

Q3 Earnings Breakdown

10 Key Points

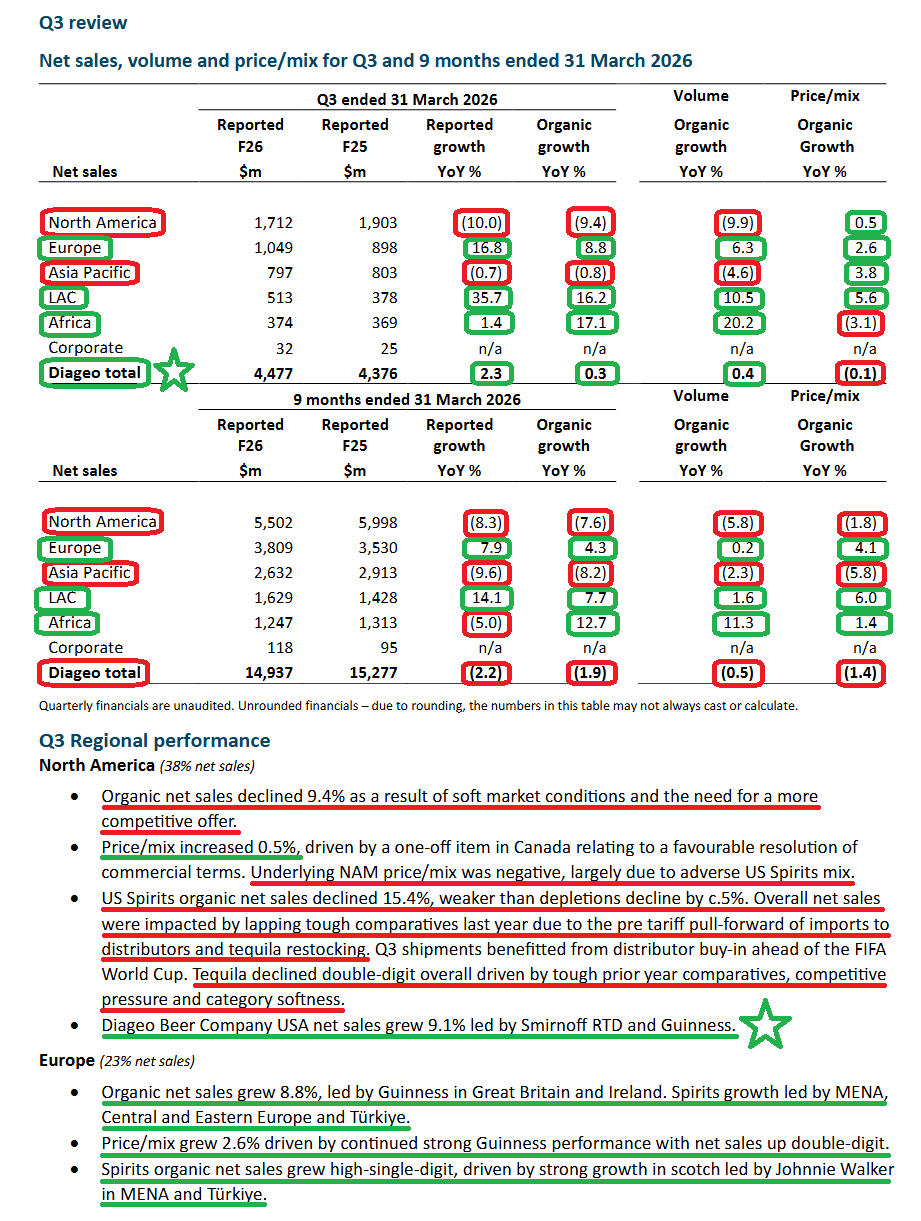

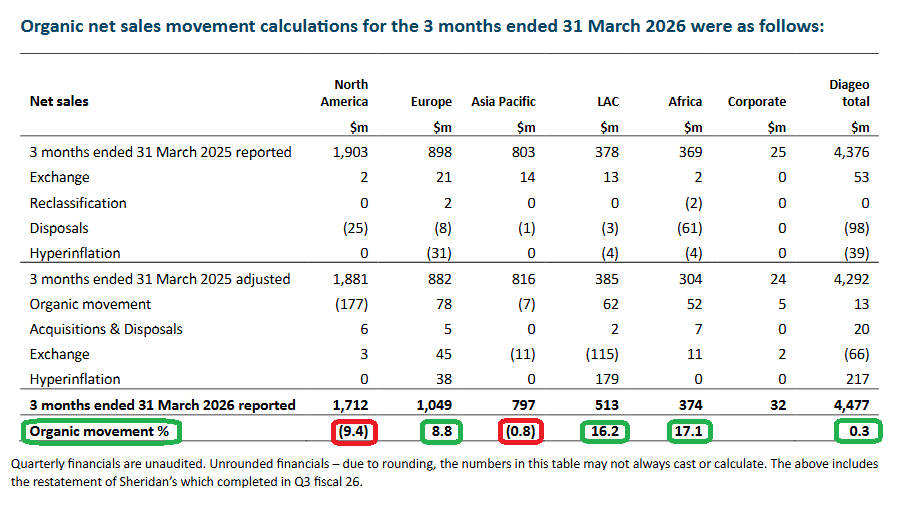

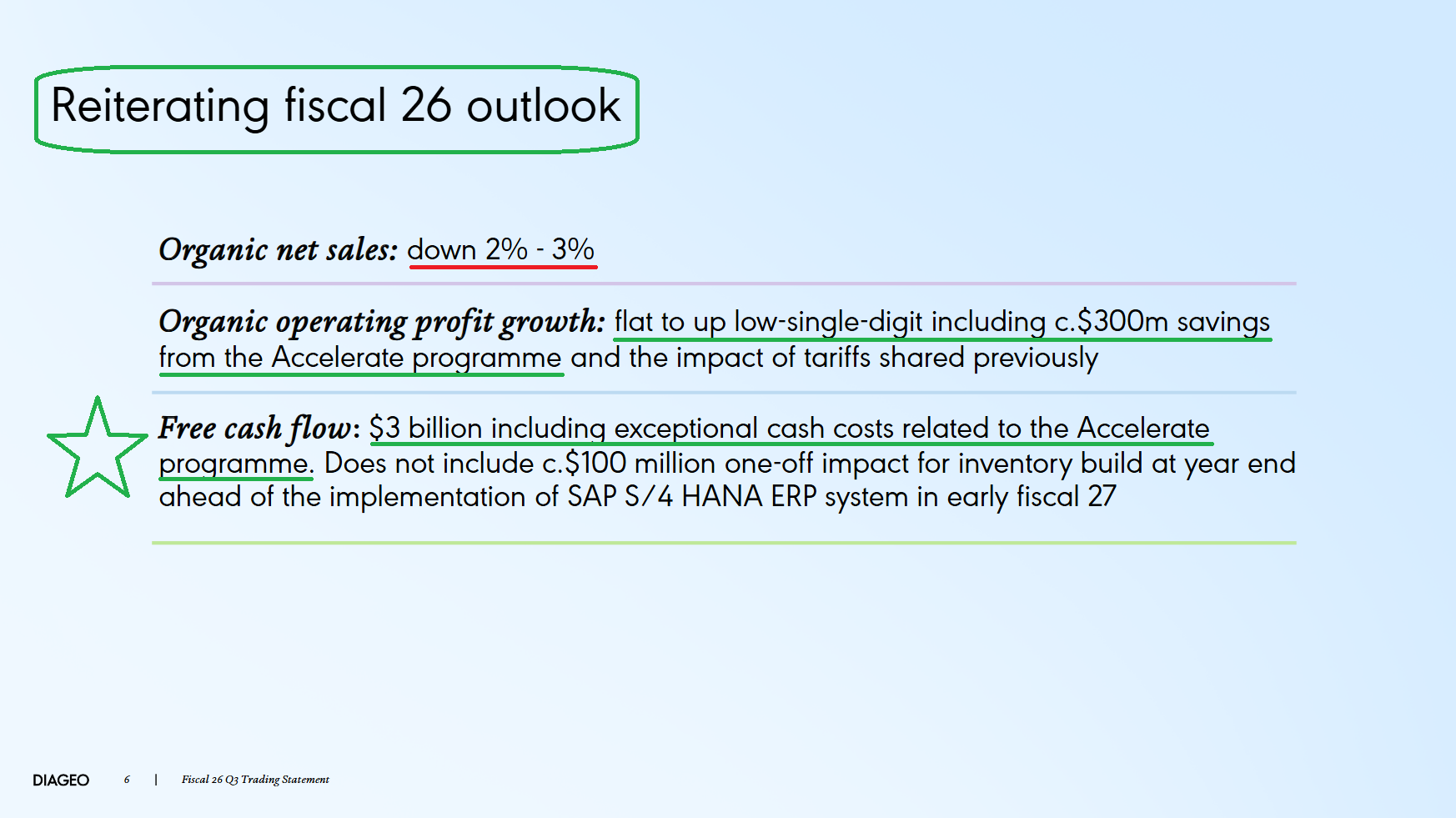

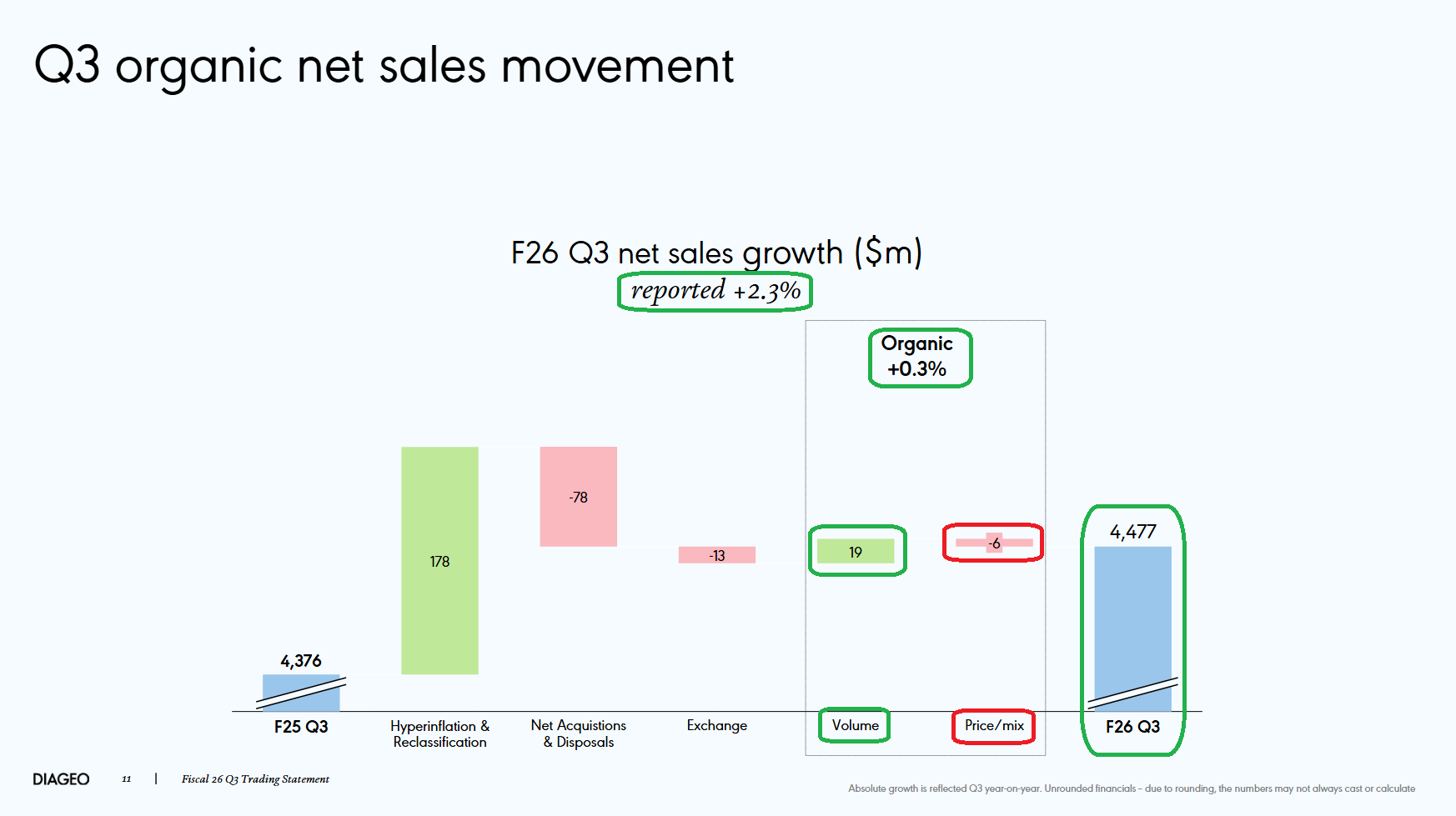

1) Diageo reported Q3 net sales of $4.48B, up +2.3% Y/Y on a reported basis and ahead of consensus expectations of $4.26B. Organic net sales grew +0.3% (volume +0.4%, price/mix -0.1%), well ahead of consensus estimates for a -2.3% decline and marking an inflection after two consecutive quarters of organic weakness. Three of five regions delivered at least high single-digit organic growth, with Europe (+8.8%), LAC (+16.2%), and Africa (+17.1%) more than offsetting North America (-9.4%) and Asia Pacific (-0.8%). YTD organic sales are now tracking at -1.9%, slightly ahead of the company’s -2% to -3% full-year guidance.

2) North America remains the company’s biggest pain point, with organic sales down -9.4% and U.S. Spirits down -15.4%. The headline decline was driven by lapping difficult comparisons from last year’s pre-tariff pull-forward and tequila restocking, along with soft underlying market conditions. Tequila declined double digits due to competitive pressure and continued category softness. Management has already begun selective price repositioning for Casamigos in Florida and other World Cup host cities, with early results described as positive. John O’Keeffe, one of Diageo’s most experienced spirits executives, has stepped in as North America CEO, replacing Sally Grimes, with a mandate to fully evaluate competitiveness, capabilities, and positioning across the region.

3) Europe was a standout performer, with organic sales up +8.8%, accelerating from +2.2% last quarter. Results were led by continued double-digit growth for Guinness in Great Britain and Ireland, with additional strength across spirits in MENA, Central and Eastern Europe, and Türkiye. Price/mix grew +2.6%, driven by Guinness as new capacity continues to come online, with management expecting the momentum to carry into Q4 as additional capacity unlocks further volume growth.

4) Asia Pacific organic sales declined -0.8%, with continued double-digit weakness in Chinese White Spirits (CWS) offsetting low single-digit growth in international premium spirits. CWS declined more than -20% during the quarter, driven by reduced consumption tied to Chinese market policy, negatively impacting regional net sales by ~3% and group net sales by ~0.6%. Management expects CWS comparisons to normalize in coming quarters as the business begins to lap these headwinds. India was also impacted by the Maharashtra excise tax increase, though excluding Maharashtra, the country delivered high single-digit growth.

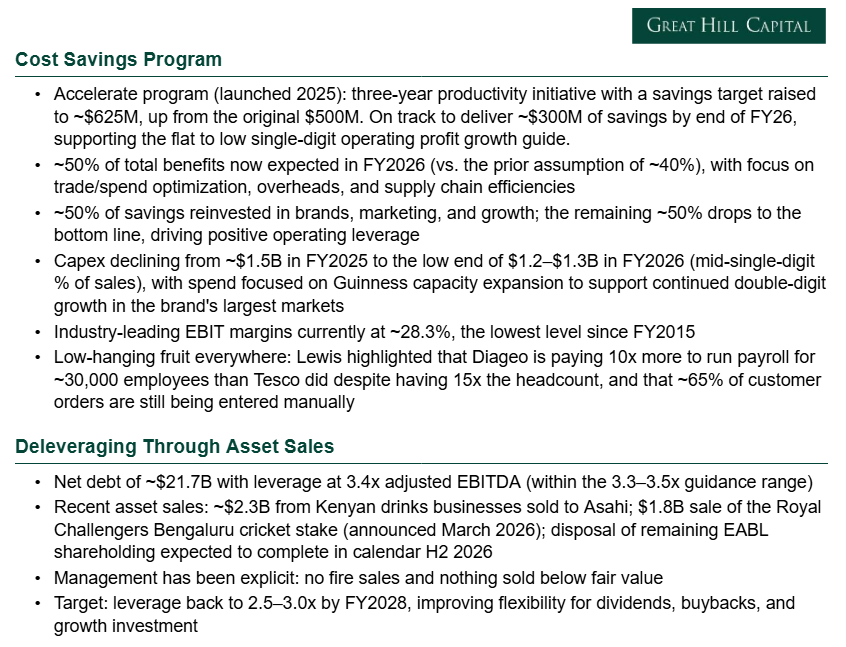

5) The Accelerate cost savings program remains on track to deliver ~$300M of savings in FY26, supporting management’s guidance for flat to low single-digit organic operating profit growth despite ongoing top-line pressure. Savings continue to come from a combination of A&P optimization, supply chain efficiencies, and reduced overhead, with management indicating that additional low-hanging fruit remains to be addressed as part of the broader operating framework redesign set to be unveiled at the August Capital Markets Day.

6) The FIFA World Cup is expected to be a critically important tailwind in 2H FY26 and into FY27, with Diageo serving as the Official Spirits Supporter in the Americas, marking the first time a spirits producer has sponsored the tournament. With 104 matches played over six weeks, compared to 64 in prior tournaments, it will be the largest World Cup in history. Diageo plans to activate top brands including Casamigos, Don Julio, Buchanan’s, Johnnie Walker, and Smirnoff at stadiums and fan festivals. Management is highly confident in the impact across Latin America given the cultural significance of football in the region, while North America will be more of a first-time learning opportunity. Early signs of momentum are already showing up in the numbers, with distributor buy-in ahead of the tournament contributing to LAC growth of +16.2% and, to a lesser extent, North America during the quarter.

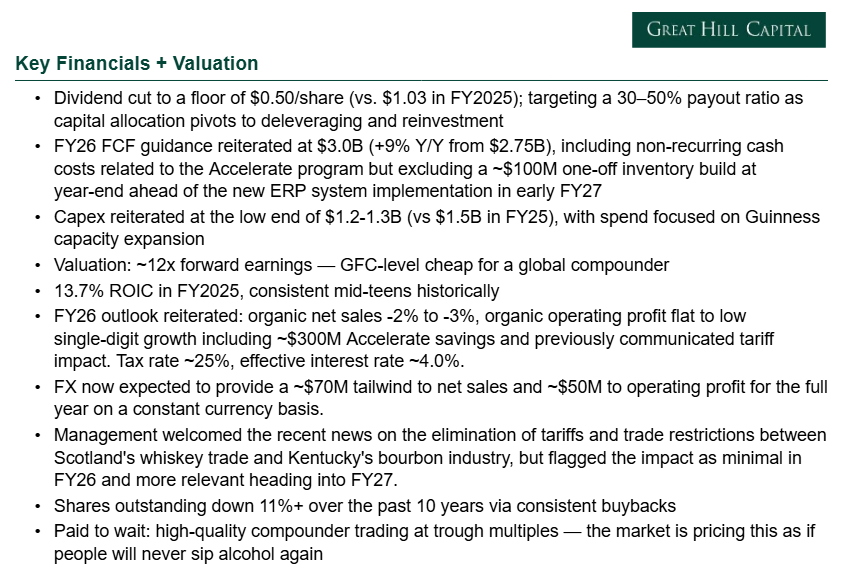

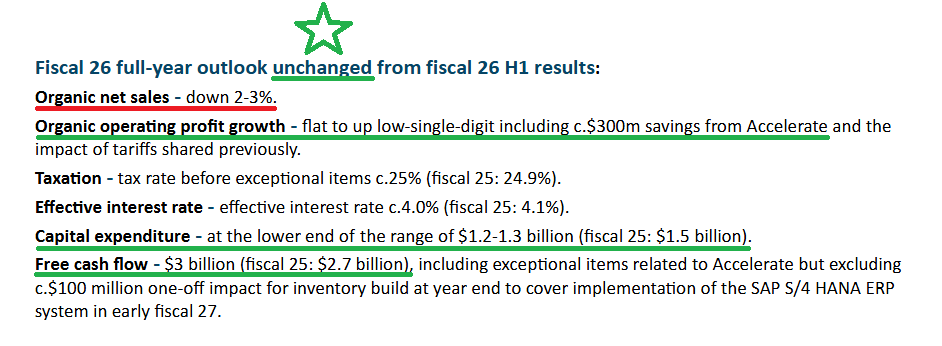

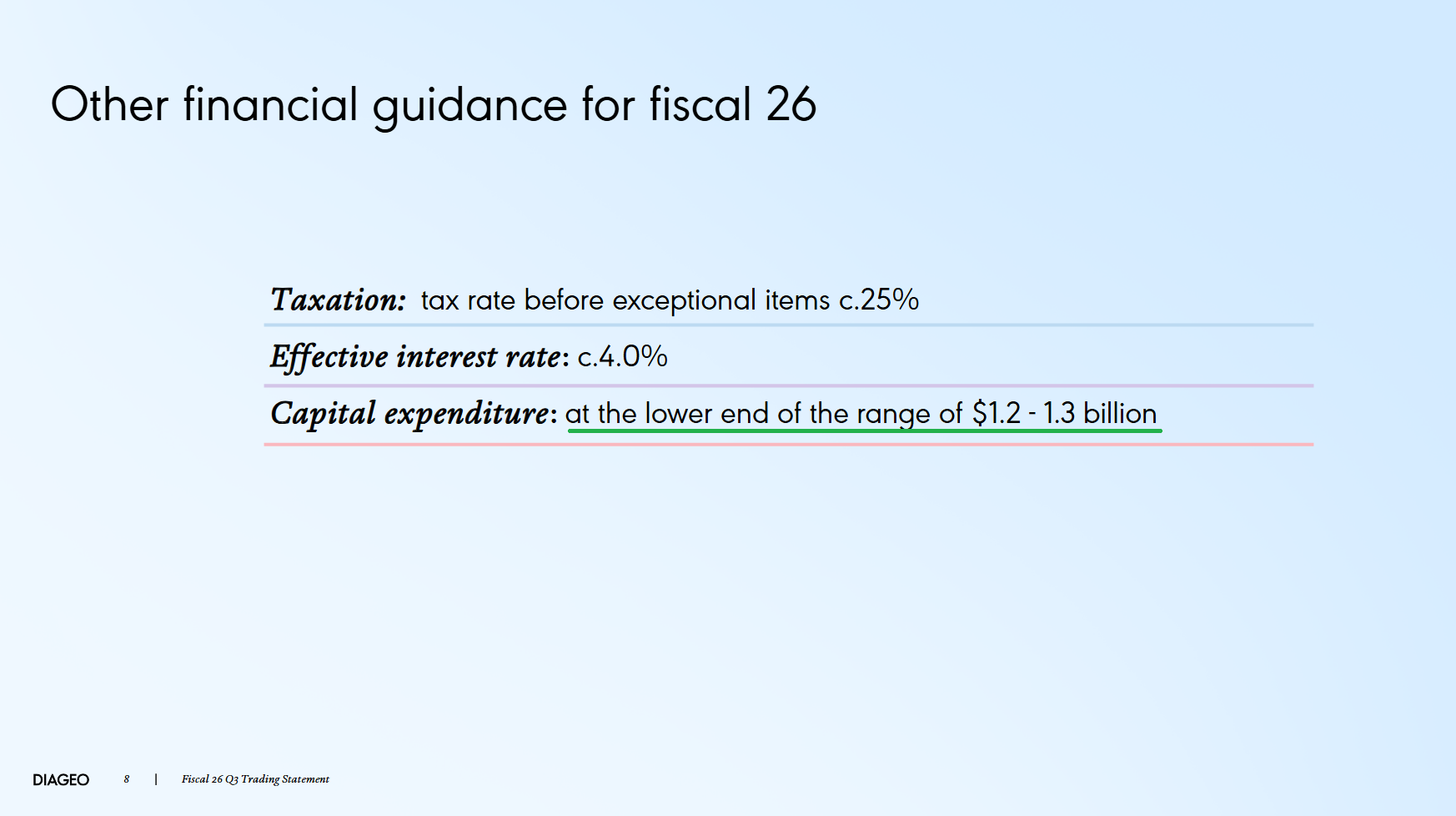

7) FY26 free cash flow guidance was reiterated at ~$3.0B (+9% Y/Y from $2.75B in FY25), including non-recurring cash costs related to the Accelerate program but excluding an ~$100M one-off inventory build at year-end ahead of the new ERP system implementation in early FY27. Capex was also reiterated at the low end of the $1.2B-$1.3B range (down from $1.5B in FY25), with spending focused on Guinness capacity expansion to support continued double-digit growth in the brand’s largest markets.

8) The Capital Markets Day has been scheduled for August 6, where CEO Dave Lewis will unveil the company’s full strategic plan and redesigned operating framework alongside FY26 full-year results. Lewis noted that the work is well underway, with management taking a step back across every region and category and working through the consumer, capabilities, portfolio, and operating framework in sequence. The goal is to lay out a credible multi-year path to improved competitiveness and growth.

9) Management noted the recent elimination of tariffs and trade restrictions between Scotland’s whisky trade and Kentucky’s bourbon industry as a positive development but indicated that the impact will be minimal in FY26 and more meaningful heading into FY27. Prior guidance calling for a ~$200M annualized operating profit headwind from tariffs before mitigation efforts remains unchanged.

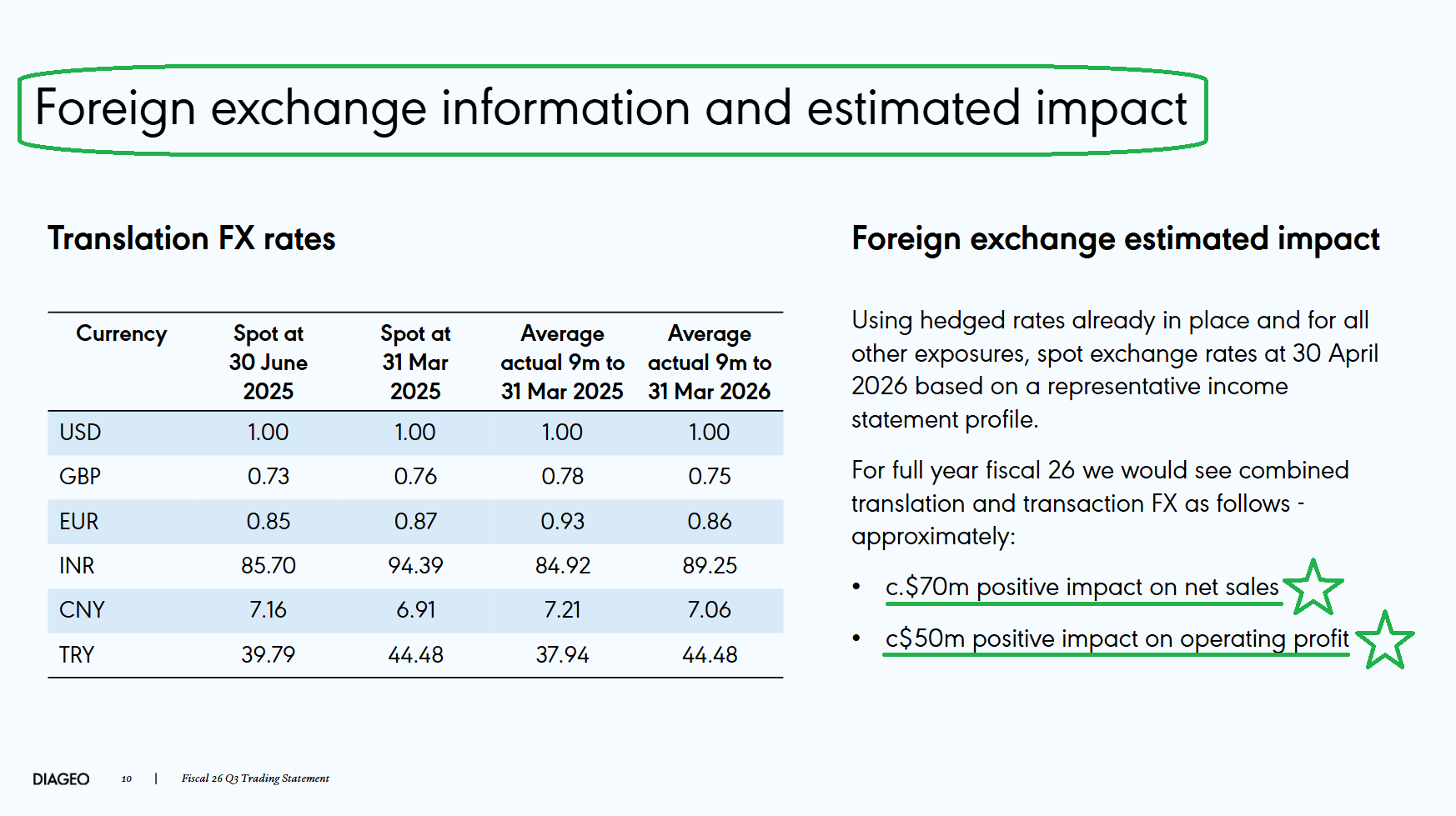

10) FY26 guidance was reiterated across the board, including organic net sales growth of -2% to -3%, organic operating profit growth ranging from flat to low single digits (including approximately $300M of Accelerate savings and the previously communicated tariff impact), a tax rate of ~25%, and capex at the low end of the $1.2B-$1.3B range. FX is now expected to provide a ~$70M tailwind to net sales and a ~$50M tailwind to operating profit for the full year.

Earnings Call Highlights

Morningstar Analyst Note

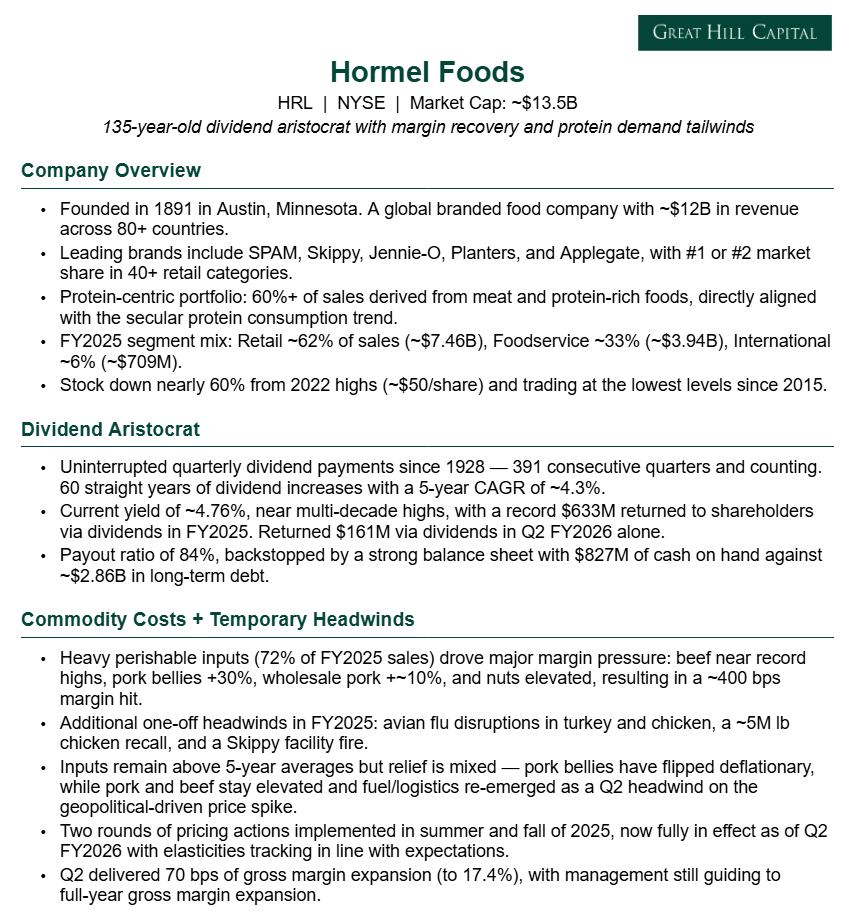

Hormel Update

For newer readers, here’s a brief overview of the key drivers behind our thesis on Hormel, an out-of-favor staples compounder and dividend aristocrat with a margin inflection ahead and the secular protein megatrend behind it:

Q2 Earnings Breakdown

10 Key Points

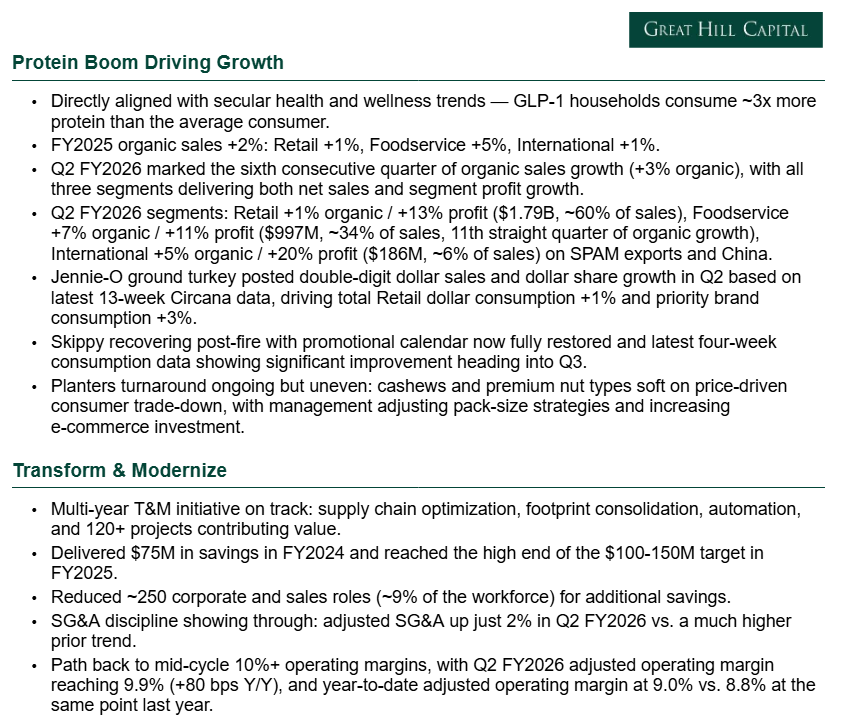

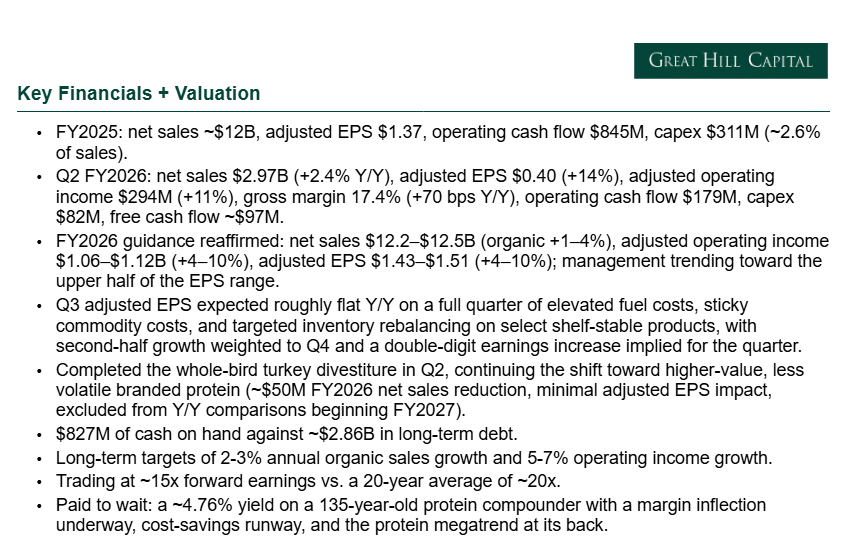

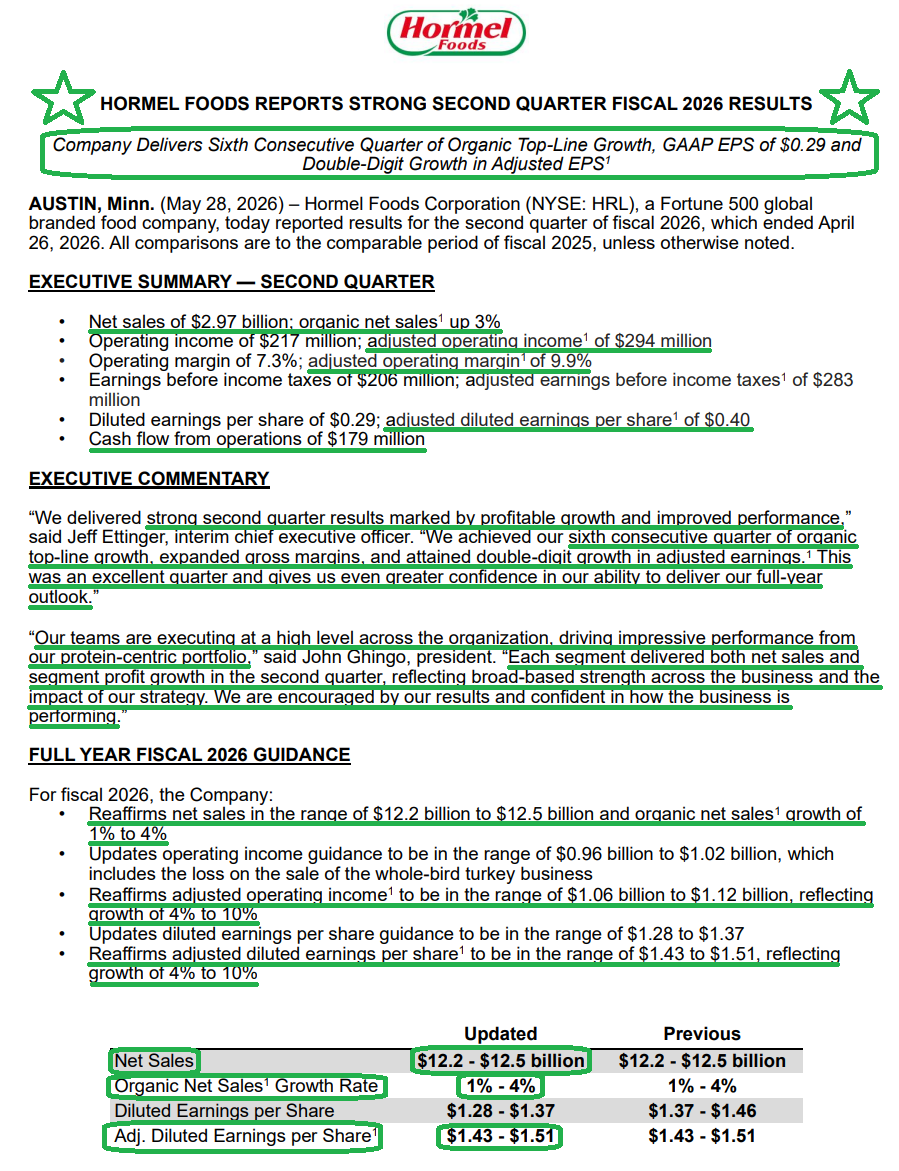

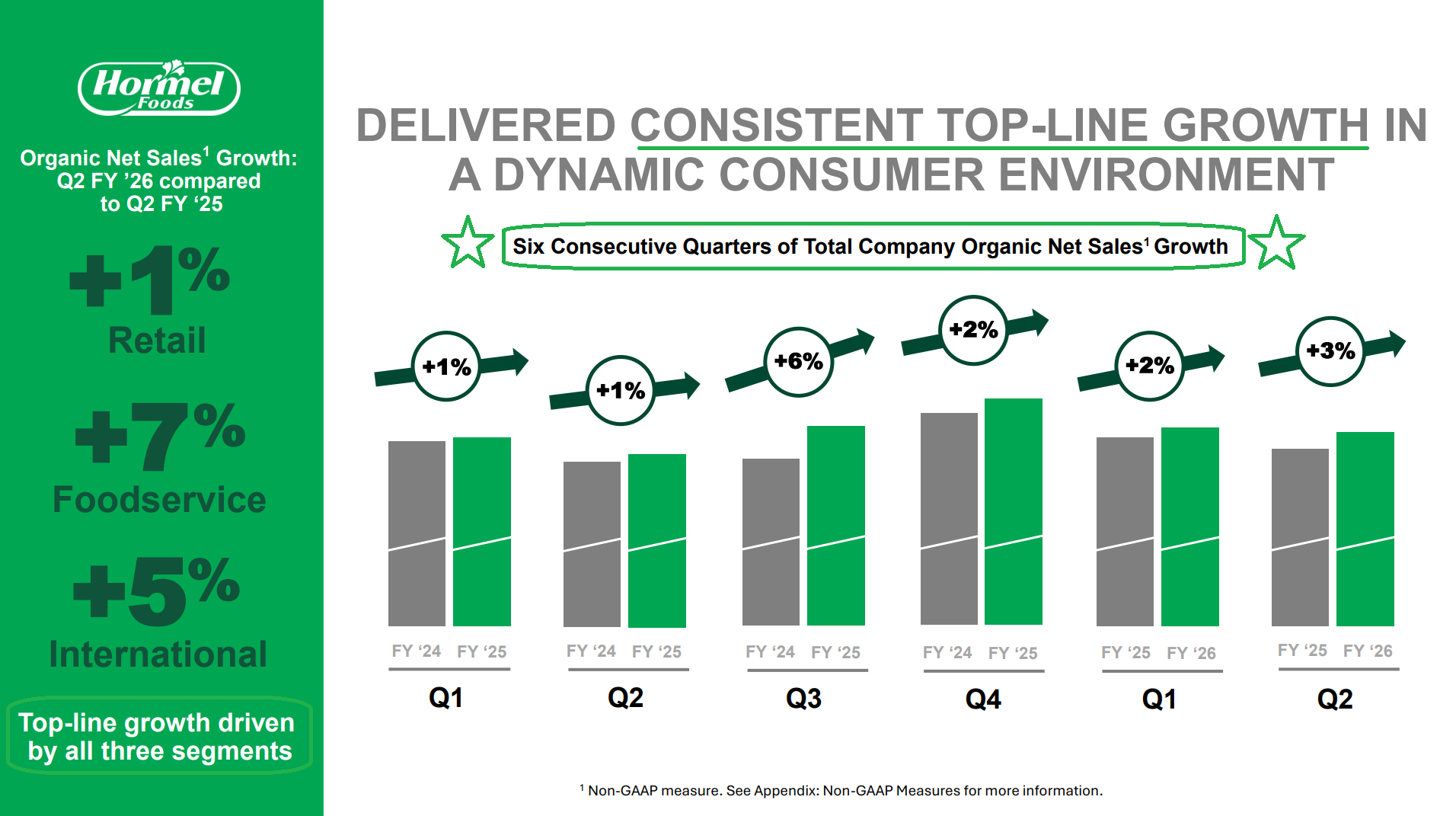

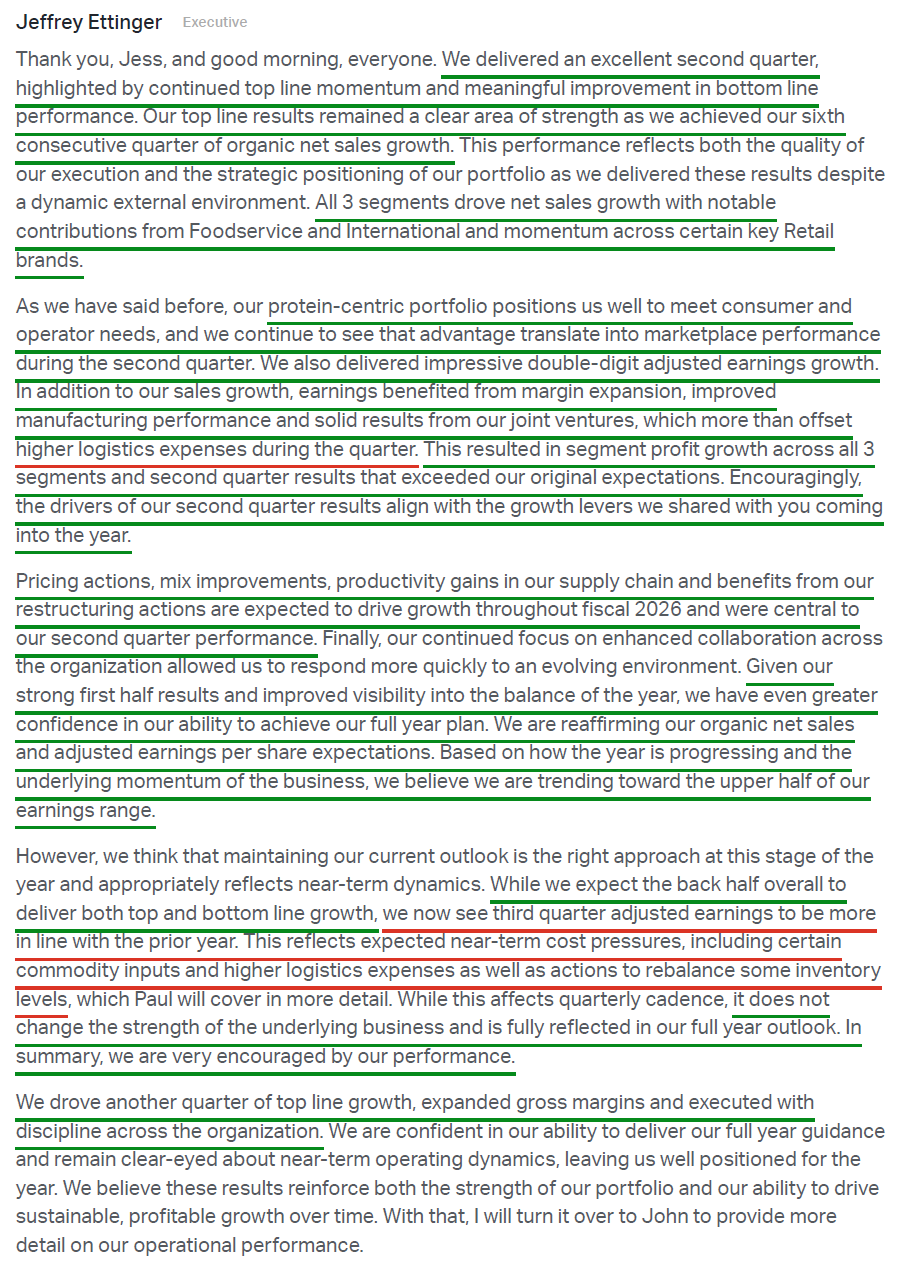

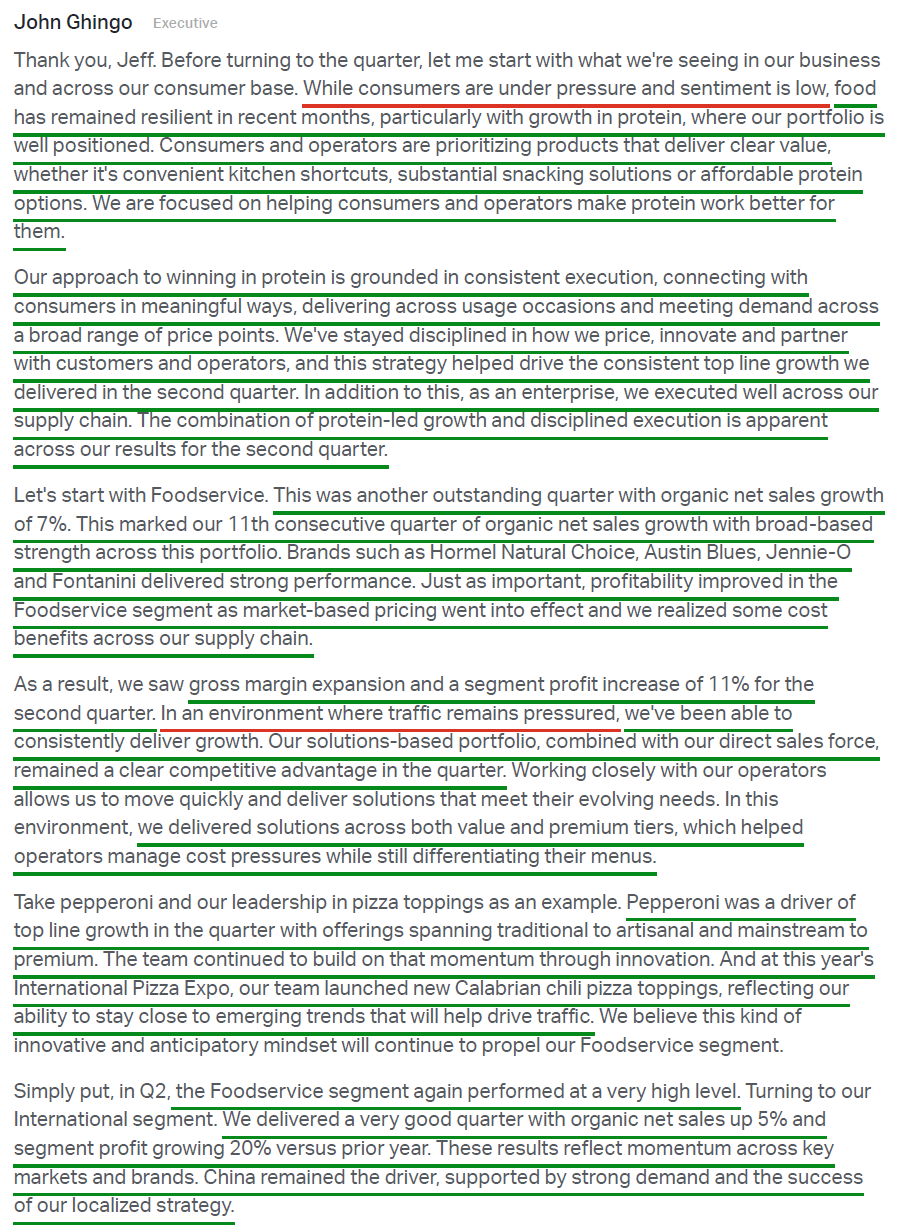

1) Hormel delivered its sixth consecutive quarter of organic net sales growth at +3% Y/Y, with reported net sales of $2.97B (+2.4% Y/Y) coming in slightly ahead of consensus expectations of ~$2.96B. Growth was broad-based across all three segments, each delivering both net sales and segment profit growth, as the protein-centric portfolio continued to resonate with consumers and operators alike in what management described as a strained consumer environment.

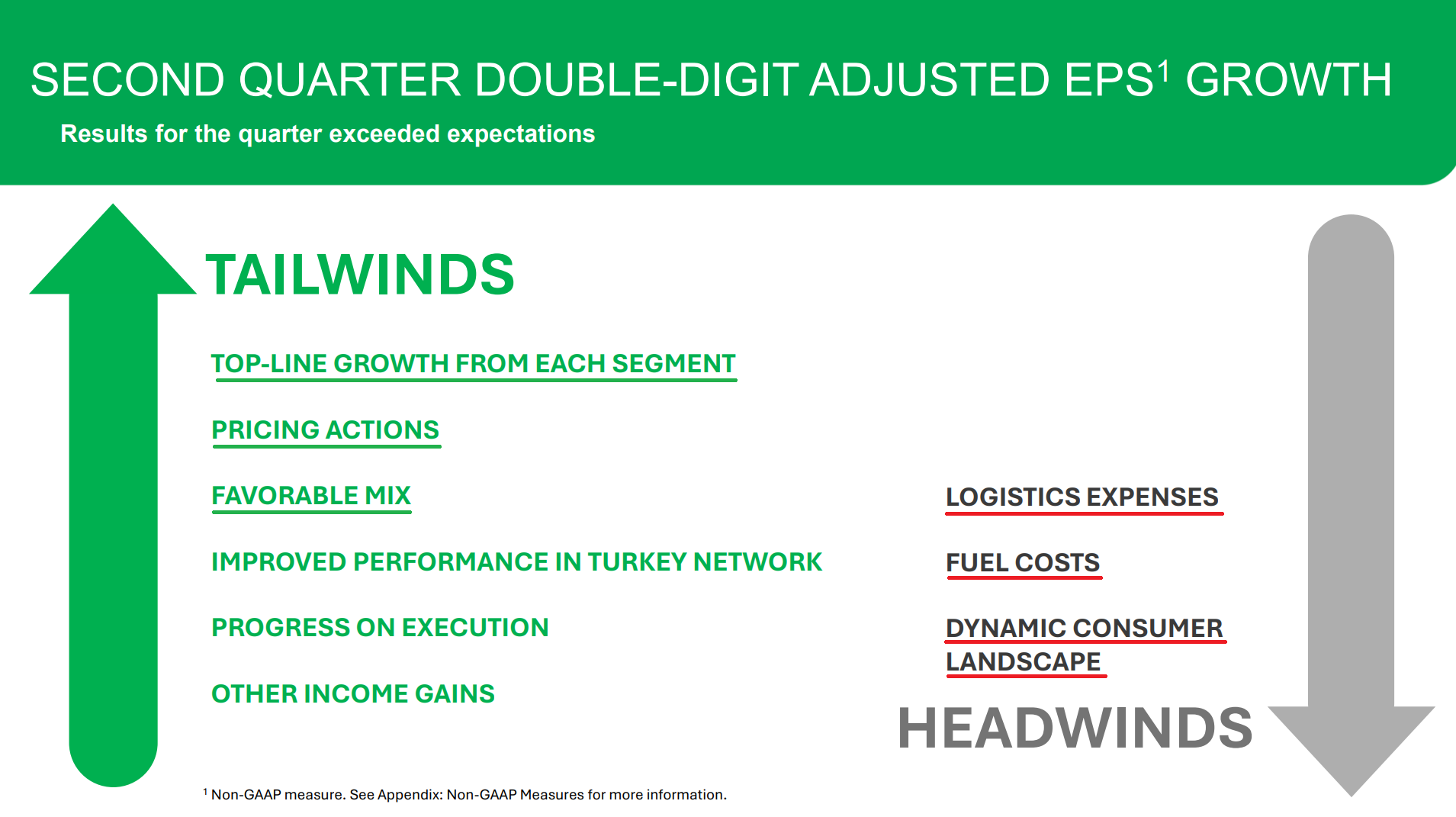

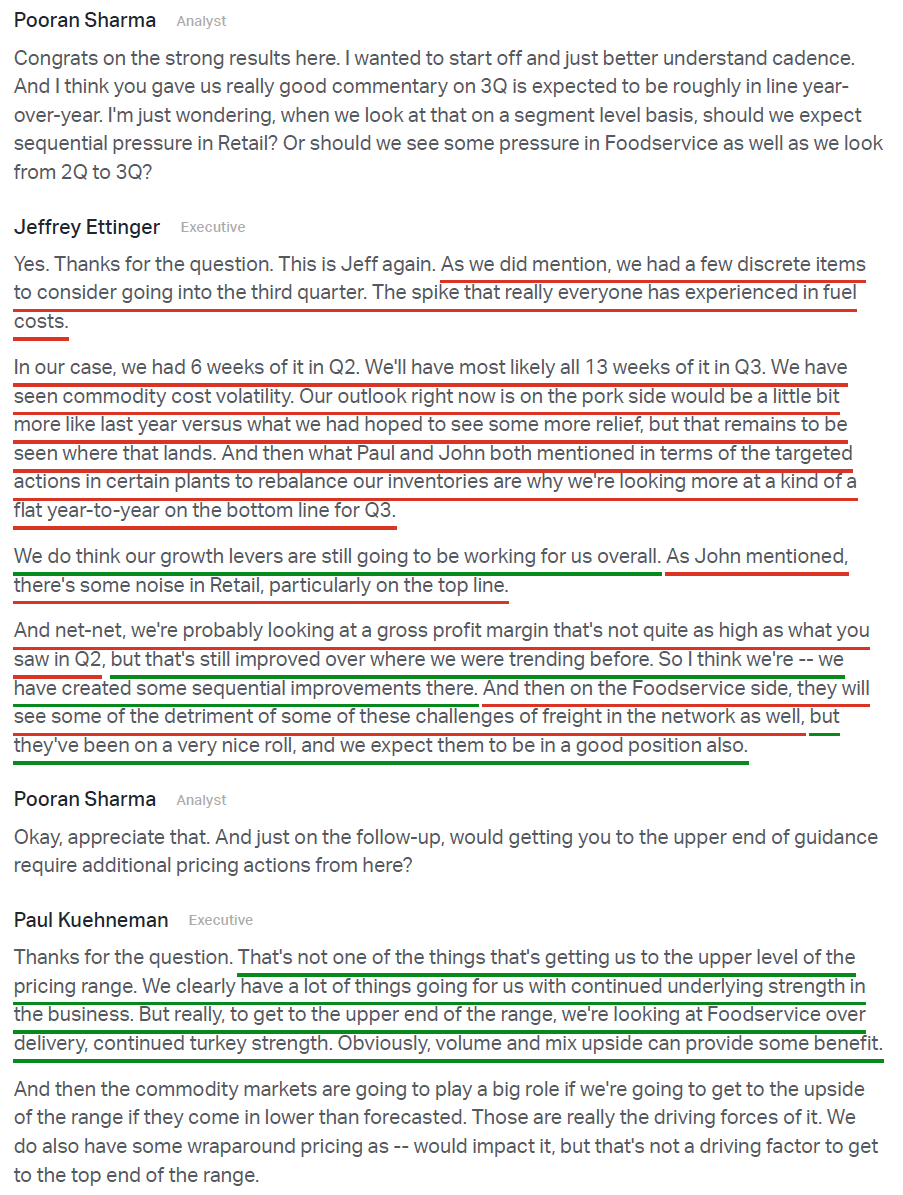

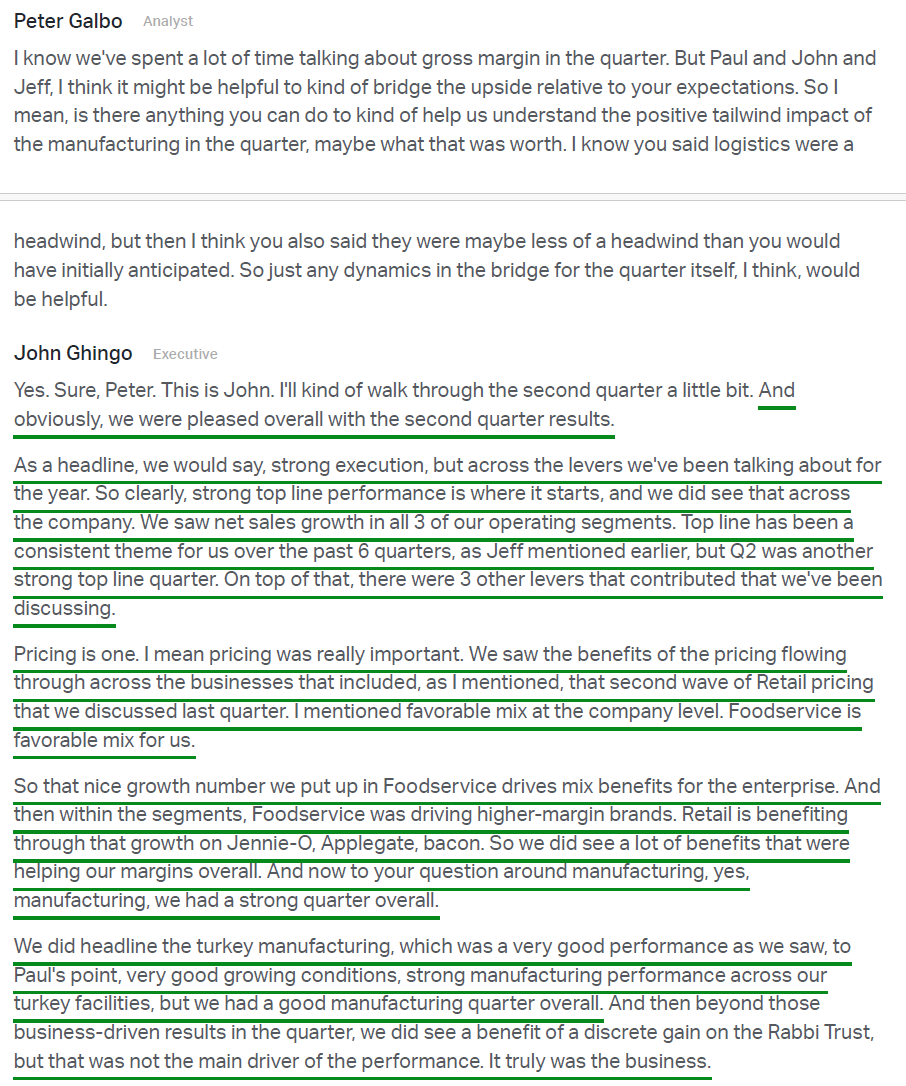

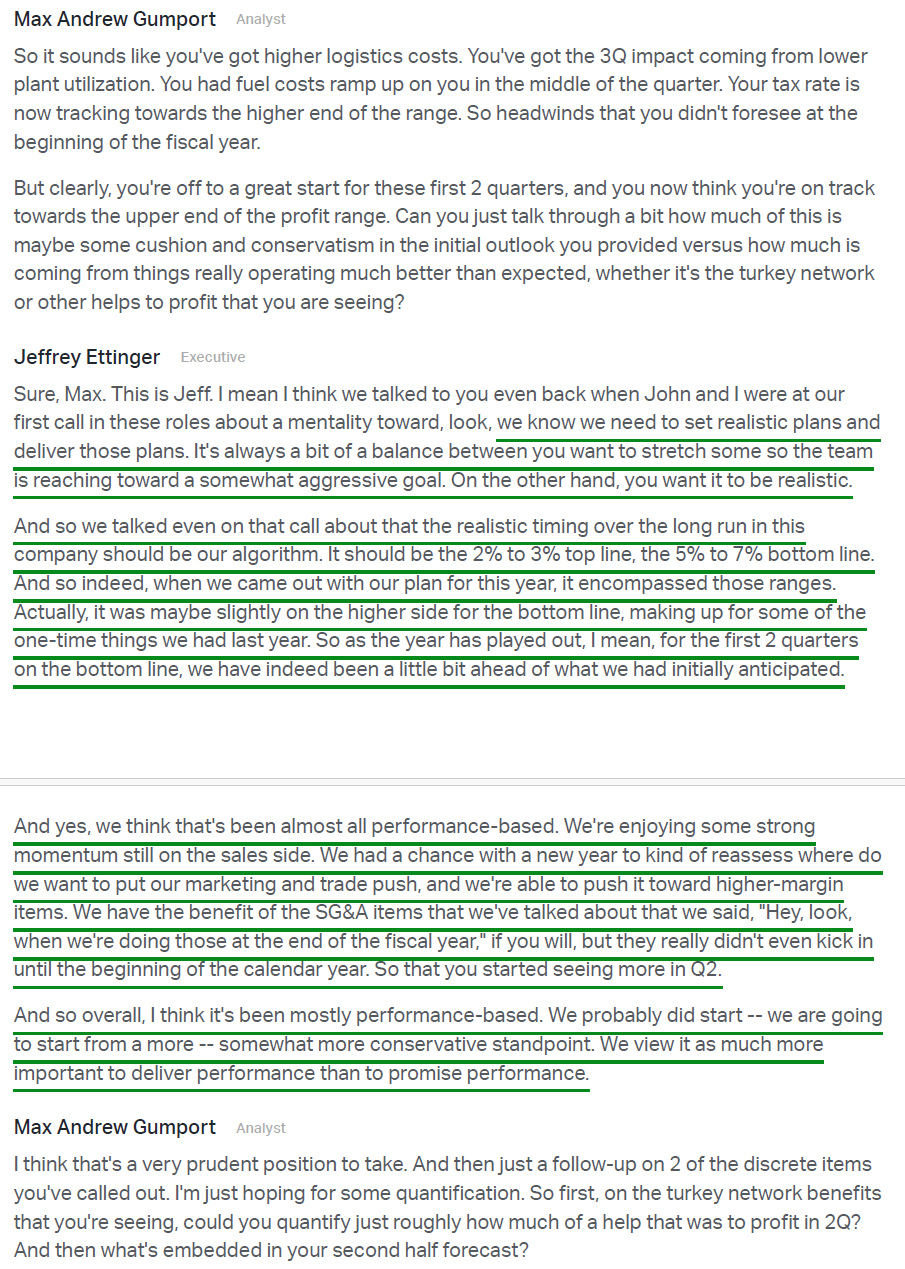

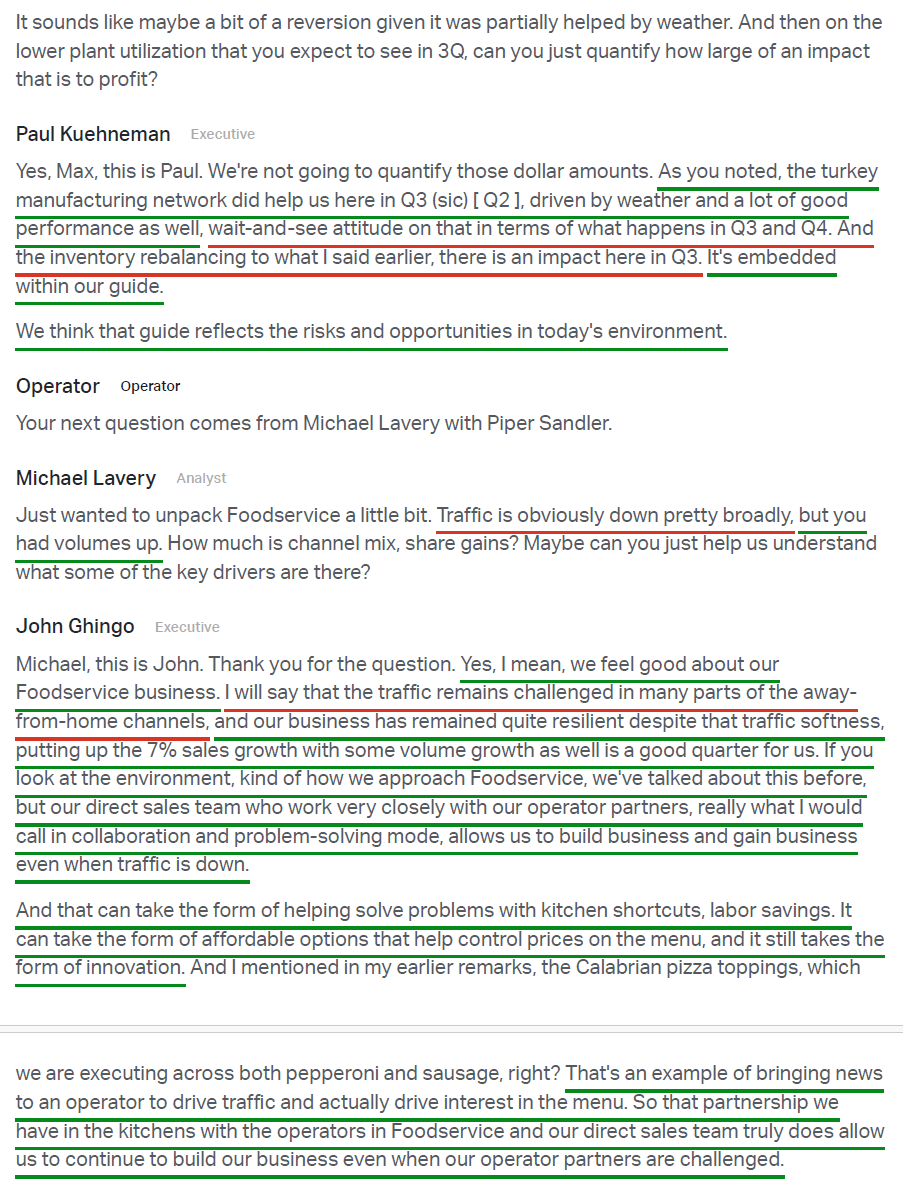

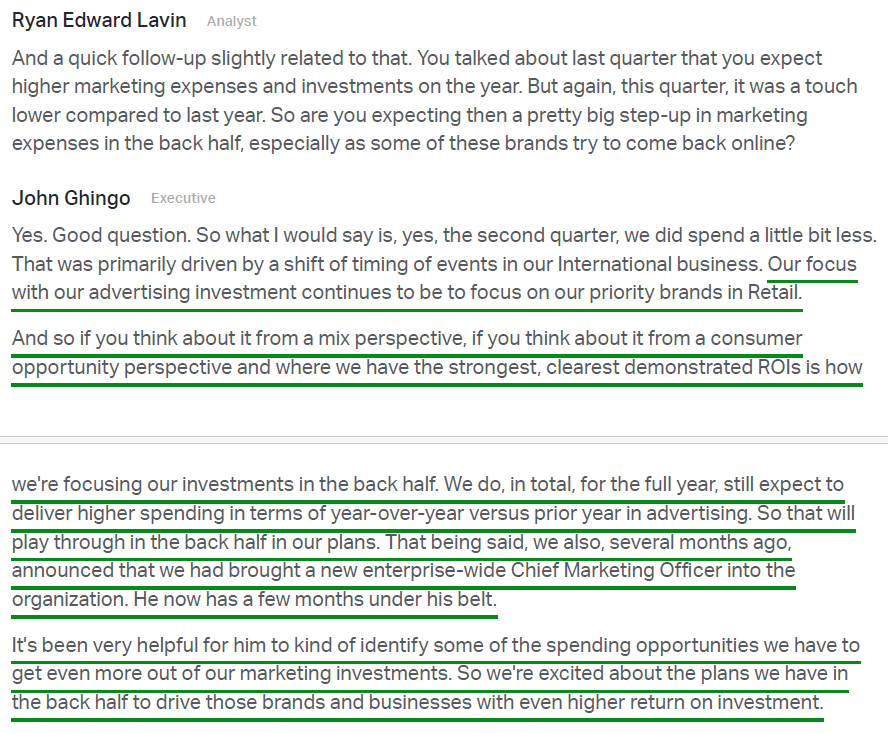

2) Adjusted diluted EPS of $0.40 (+14% Y/Y) beat consensus expectations of $0.35, marking double-digit earnings growth for the quarter and putting management on track toward the upper half of its full-year earnings guidance range. The outperformance was driven by top-line strength, pricing actions, favorable mix, improved turkey manufacturing performance, and SG&A discipline, all of which more than offset continued pressure from logistics costs and elevated fuel expenses.

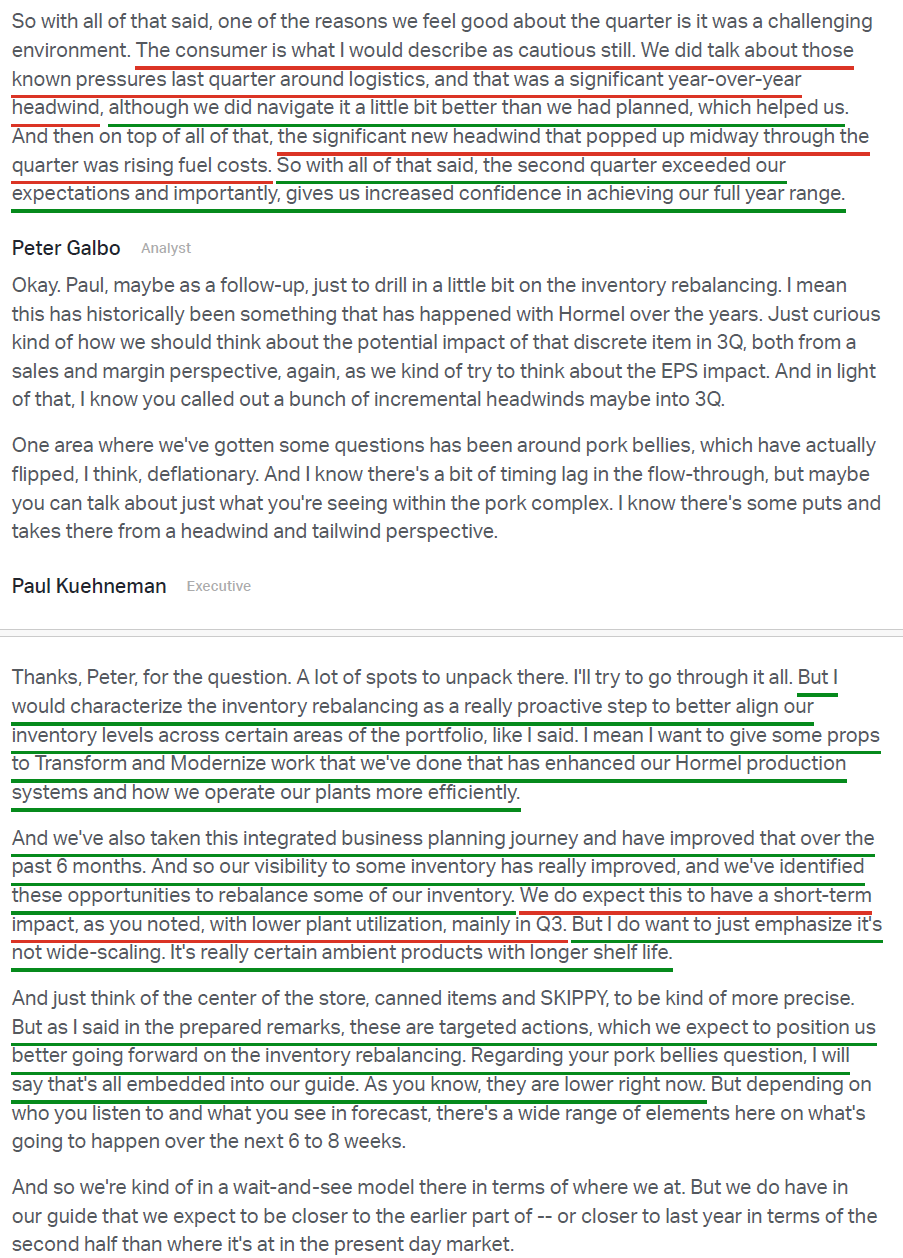

3) Gross profit came in at $519M (+7% Y/Y), with gross margin expanding 70 bps to 17.4%. The improvement was driven by pricing actions, a favorable mix shift toward higher-margin branded proteins, and better performance across the turkey manufacturing network. Pork and beef costs remained elevated relative to historical levels, while logistics continued to be a Y/Y headwind. However, both came in better than originally anticipated, allowing the business to absorb those pressures and still deliver solid margin expansion.

4) Adjusted operating income of $294M (+11% Y/Y) drove adjusted operating margin to 9.9%, up 80 bps from 9.1% a year ago and well ahead of the ~8.9% consensus expectation. Adjusted SG&A increased just 2% Y/Y and remained flat as a percentage of net sales at 8.2%, reflecting the benefits of the corporate restructuring actions taken during FY2025. Year-to-date adjusted operating margin now sits at 9.0%, compared to 8.8% at the same point last year.

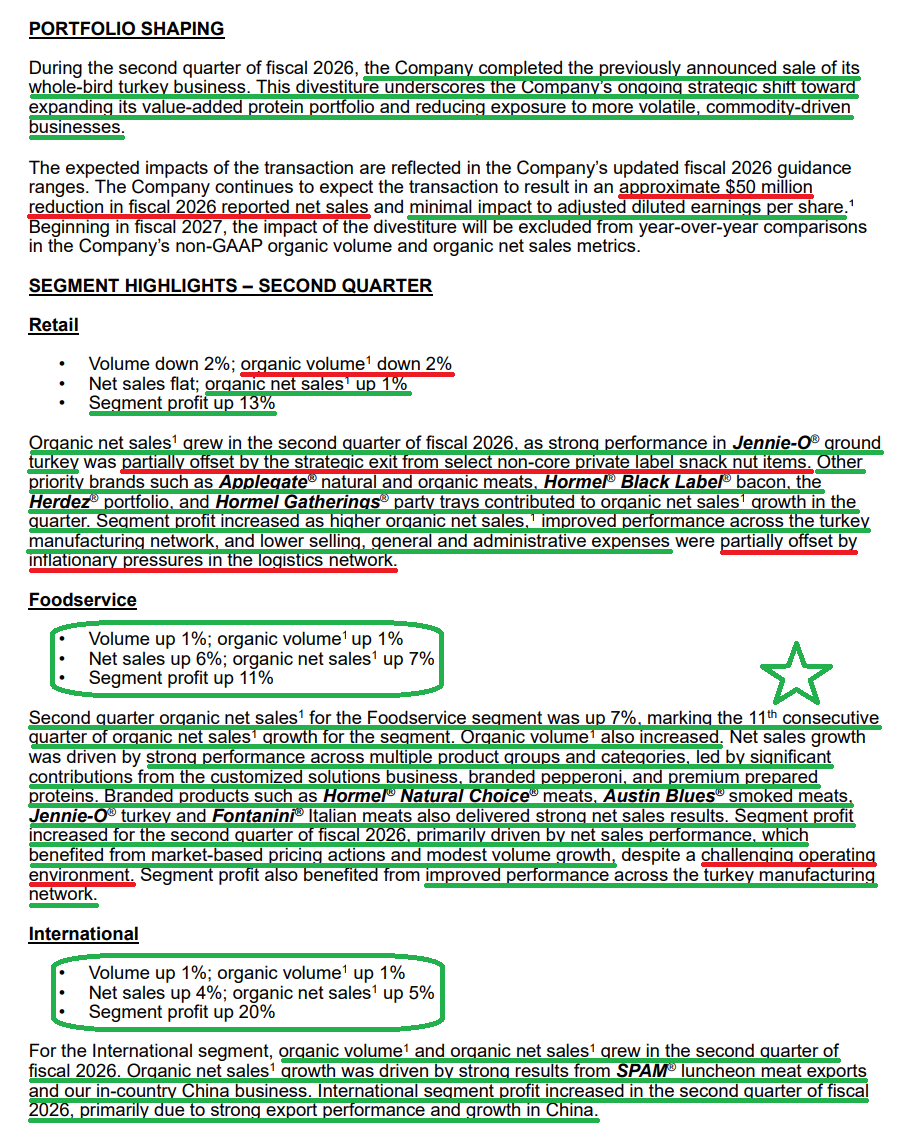

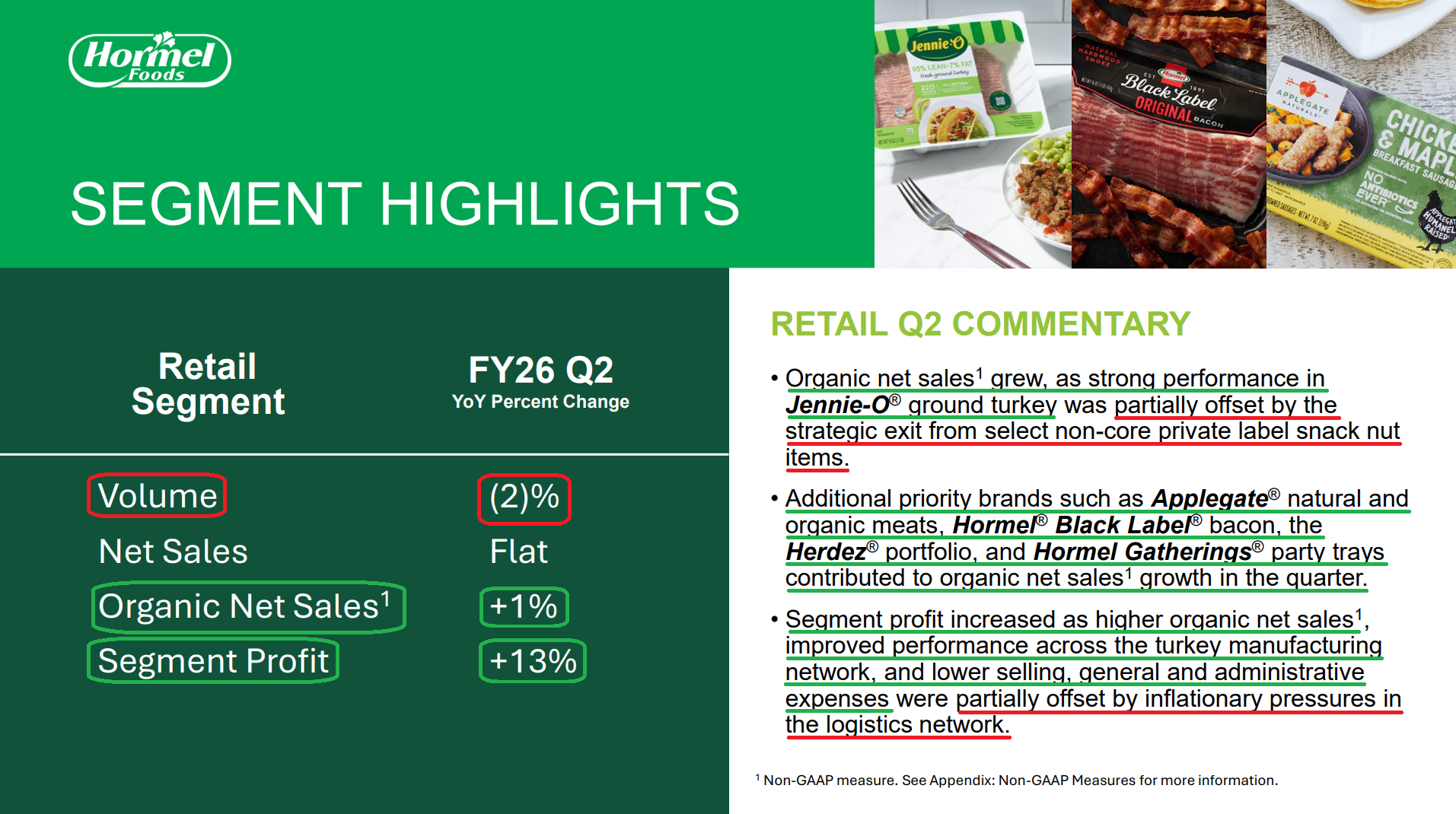

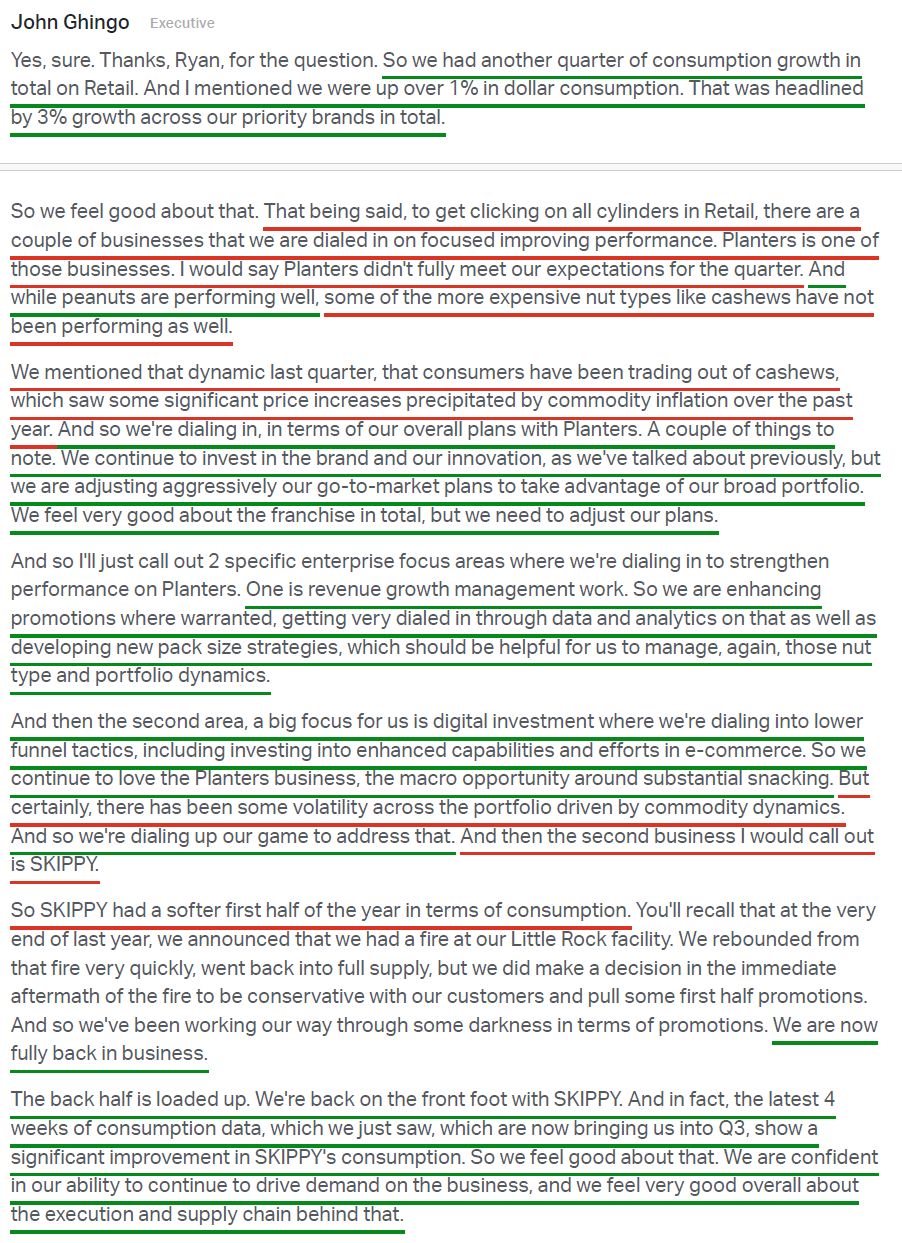

5) The Retail segment posted net sales that were roughly flat at $1.79B (~60% of total net sales), with organic net sales growth of +1%, volume down -2%, and segment profit up +13% Y/Y. Segment profit margin expanded ~100 bps to 8.7%, ahead of management’s own expectations. The second wave of pricing actions was fully reflected on shelves during the quarter, with elasticities tracking largely in line with expectations. Jennie-O ground turkey led the way with double-digit dollar sales and dollar share growth in the latest 13-week Circana data, while Applegate, Hormel Black Label bacon, and Herdez also contributed, driving total dollar consumption growth of +1% and priority brand consumption growth of +3%. Planters faced pressure as consumers traded away from higher-priced nut varieties such as cashews following commodity-driven price increases, prompting management to adjust pack-size strategies and increase e-commerce investment. Skippy’s softer first half was driven by a deliberate pullback in promotions following the Little Rock facility fire. With the brand now back to full supply and normal promotional activity, the latest four-week consumption data is already showing meaningful improvement.

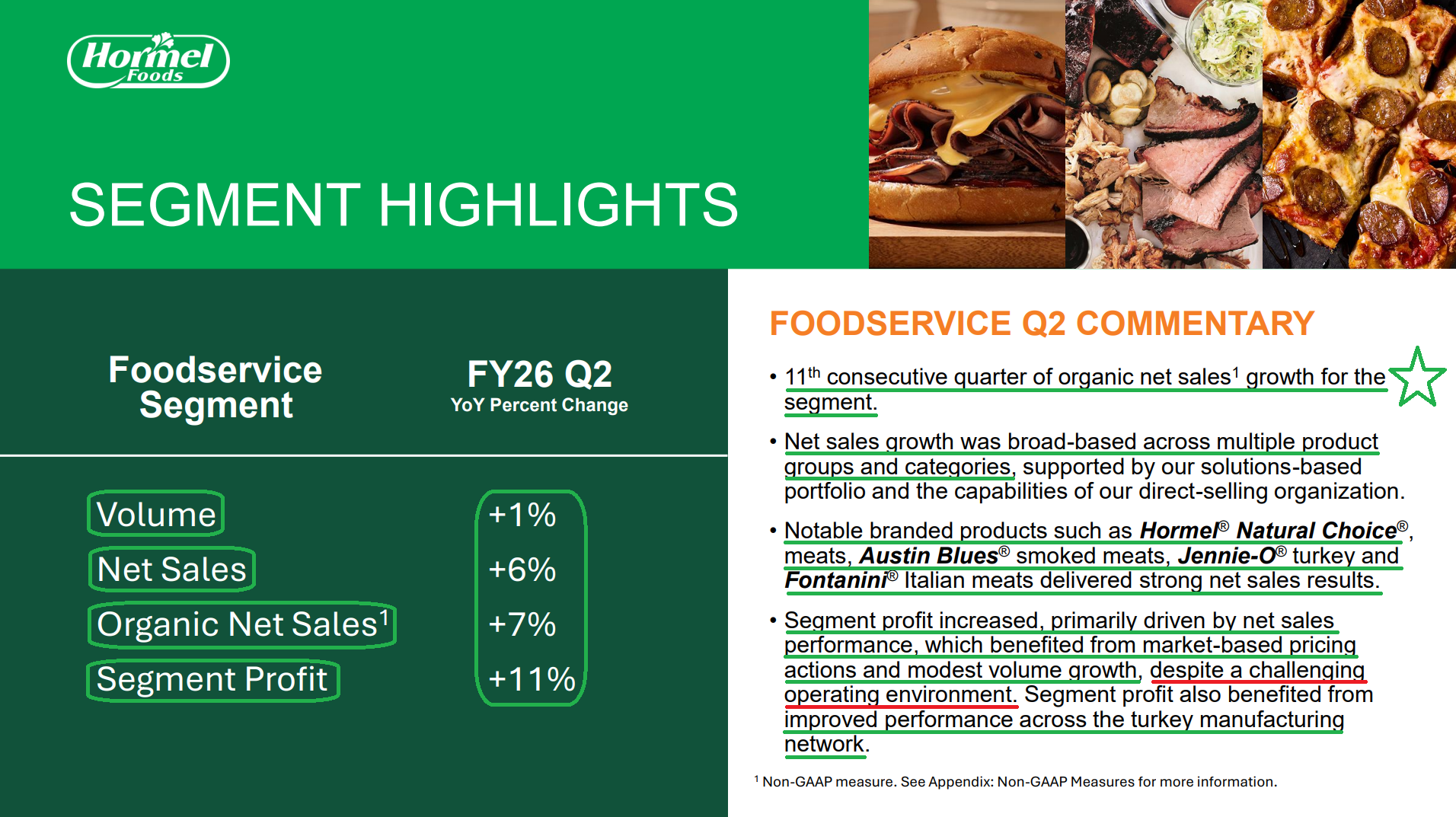

6) The Foodservice segment posted net sales growth of +6% to $997M (~34% of total net sales), with +7% organic net sales growth marking its 11th consecutive quarter of organic net sales growth. Segment profit grew +11%, with margin expanding ~60 bps to 15.6%. Despite away-from-home traffic remaining under pressure throughout the quarter, the segment delivered strong results driven by broad-based growth across categories, led by branded pepperoni, customized solutions, and premium prepared proteins. Hormel Natural Choice, Austin Blues, Jennie-O, and Fontanini all delivered strong net sales results. Management credited the direct-selling organization and solutions-based portfolio, which works closely with operators on kitchen shortcuts, labor savings, and menu innovation, as a key competitive advantage in the current environment. Full-year guidance assumes traffic remains at current levels, with any improvement representing potential upside to the outlook.

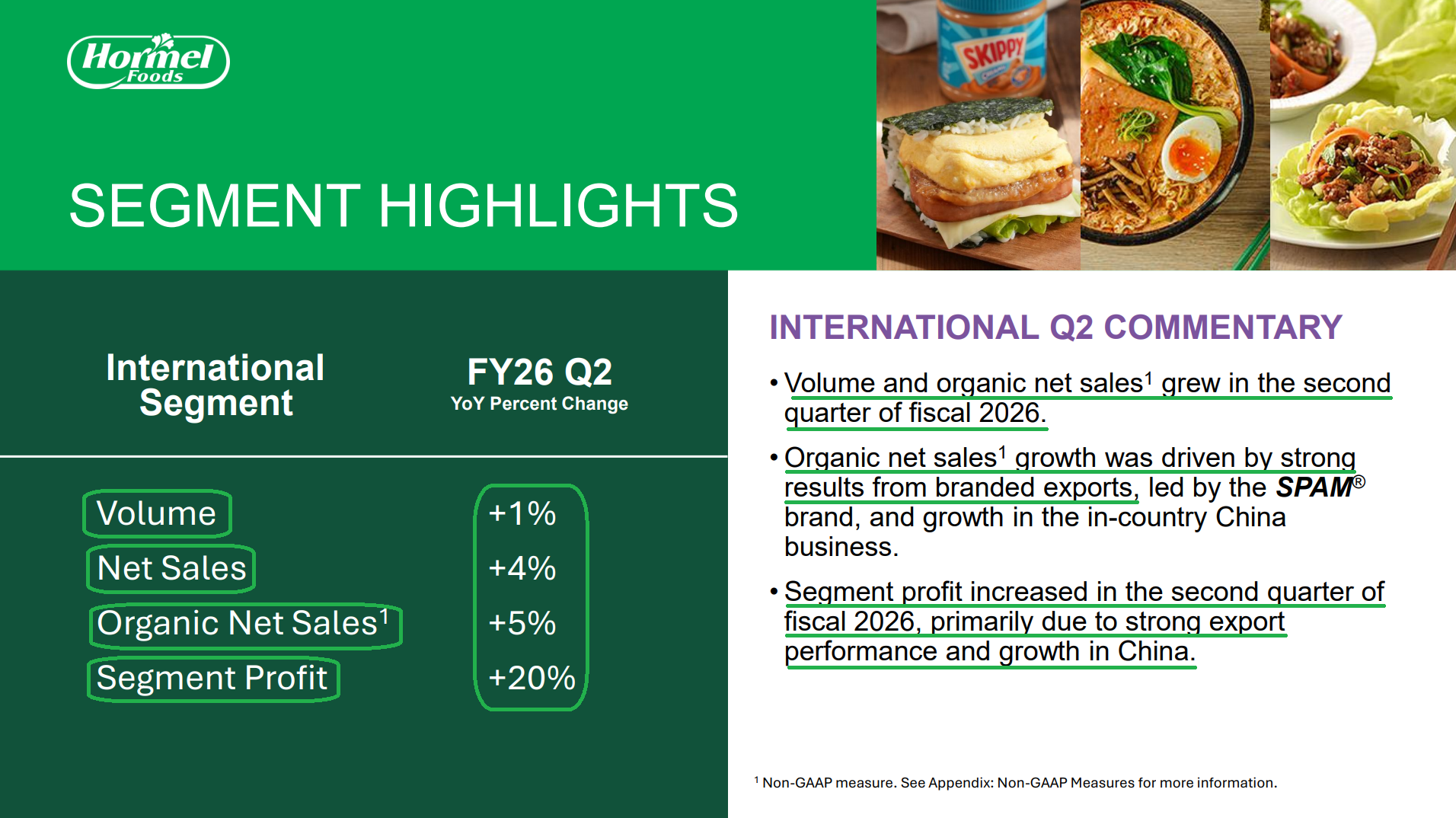

7) The International segment posted net sales growth of +4% to $186M (~6% of total net sales), with organic net sales growth of +5%, volume growth of +1%, and segment profit growth of +20%, the strongest profit growth among the three segments this quarter. Segment profit margin expanded ~160 bps to 11.9%. Results were driven by SPAM-led branded exports and continued momentum in the in-country China business, with management citing the success of Hormel’s localized strategy in China as the primary growth driver.

8) Operating cash flow came in at $179M for the quarter. After capital expenditures of $82M (vs. $75M last year), the company generated free cash flow of ~$97M. Cash on hand at quarter-end totaled $827M, up $156M since fiscal year-end, against total long-term debt of ~$2.86B. The balance sheet remains conservatively positioned, with ample liquidity to continue investing in the business while returning capital to shareholders.

9) Hormel returned $161M to shareholders through dividends during the quarter, marking its 391st consecutive quarterly dividend payment and maintaining its Dividend Aristocrat status, supported by more than 60 consecutive years of dividend increases. The current annual dividend yield stands at ~4.76%, and management reiterated its commitment to maintaining that streak.

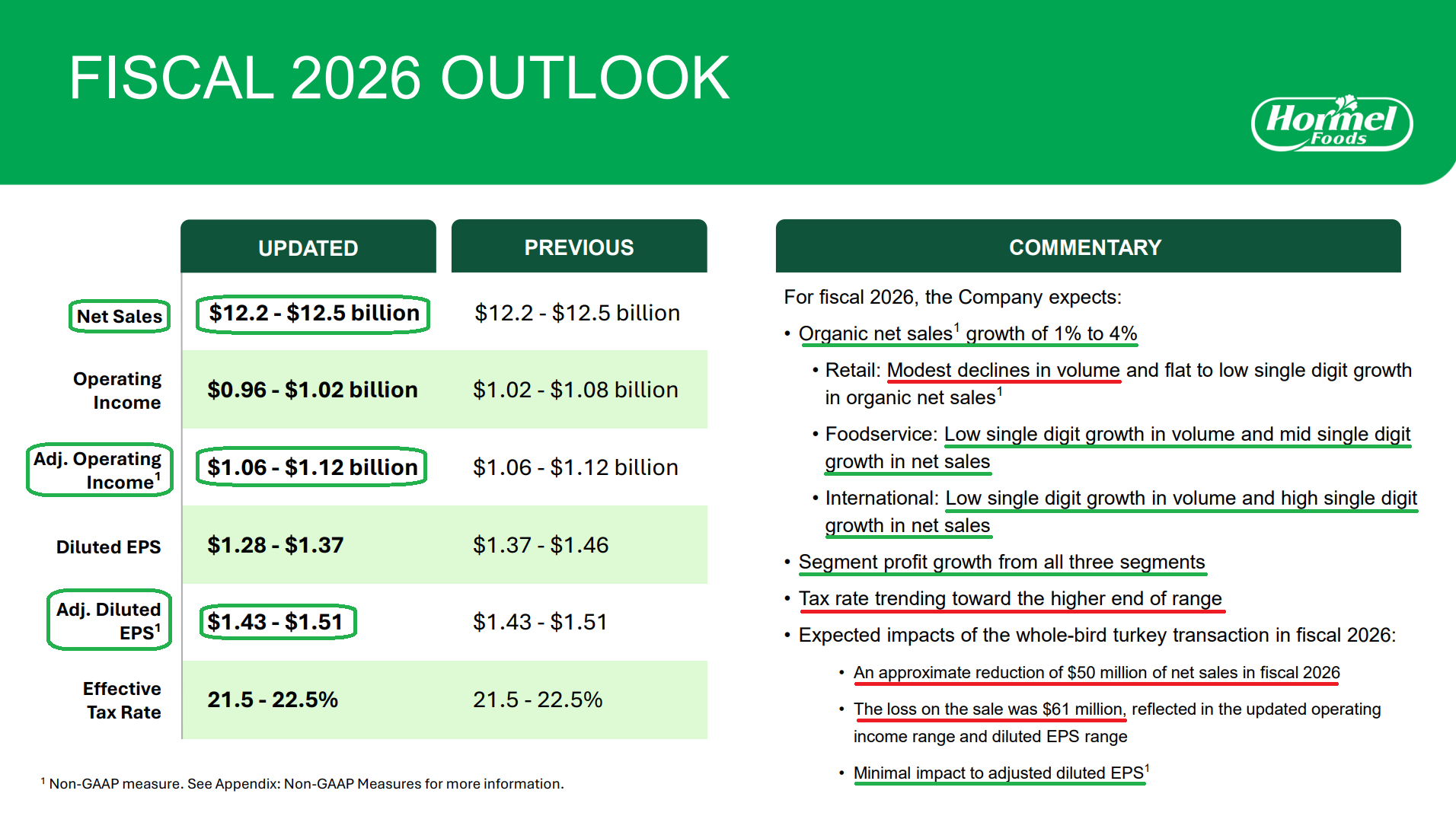

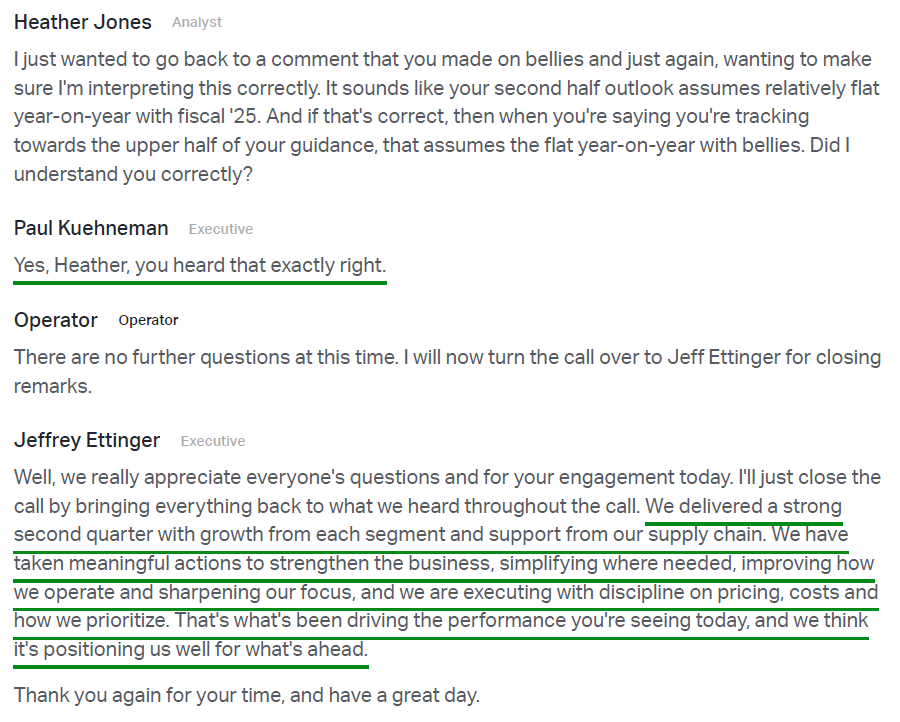

10) Management reiterated full-year FY2026 guidance for net sales of $12.2B-$12.5B, organic net sales growth of +1% to +4%, adjusted operating income of $1.06B-$1.12B (+4% to +10%), and adjusted diluted EPS of $1.43-$1.51 (+4% to +10%). Segment-level expectations were unchanged across Retail (flat to low-single-digit organic growth), Foodservice (mid-single-digit net sales growth), and International (high-single-digit net sales growth), with profit growth expected from all three segments. Near-term, management indicated that Q3 adjusted EPS is likely to be roughly flat Y/Y, reflecting a full quarter of elevated fuel costs (versus only six weeks in Q2), sticky commodity costs, and a targeted inventory rebalancing initiative on select shelf-stable products that will temporarily reduce plant utilization.

Earnings Call Highlights

Morningstar Analyst Note

General Market

The CNN “Fear and Greed Index” ticked up to 44 this week from 34 last week. You can learn how this indicator is calculated and how it works here: (Video Explanation)

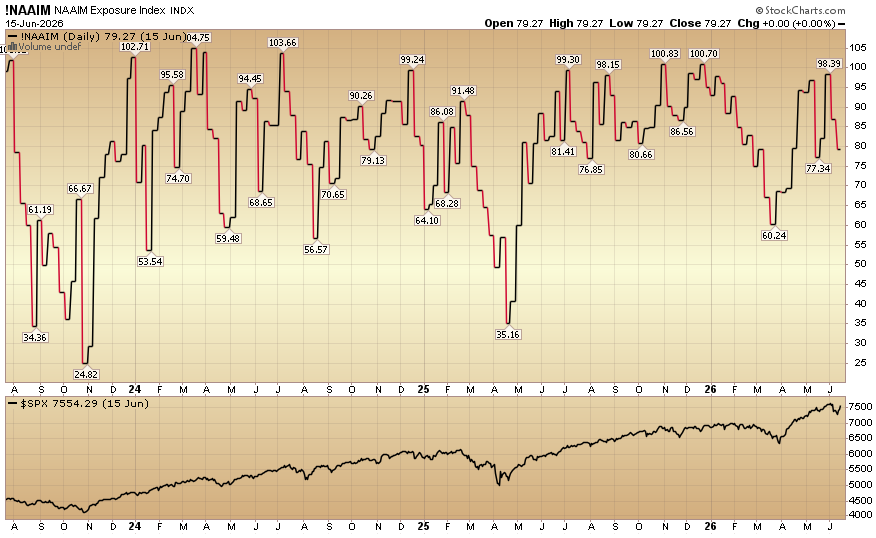

The NAAIM (National Association of Active Investment Managers Index) (Video Explanation) fell to 79.27% equity exposure this week from last week’s 98.39%.

Our podcast|videocast will be out sometime today. We have a lot of great data to cover this week. Each week, we have a segment called “Ask Me Anything (AMA)” where we answer questions sent in by our audience. If you have a question for this week’s episode, please send it in at the contact form here.

Larger accounts $5-10M+ can access bespoke service anytime here.

Not a solicitation.

*Opinion, Not Advice. See Terms

Comments

Log in or sign up to join the conversation.