Gold’s Strong Hands Are Still Buying

The gold market is beginning to resemble a crowded theatre after the opening act has ended. The true believers are still in their seats, patiently waiting for the second half, but the tourists who rushed in during the excitement have already headed for the exits. That distinction matters because while gold remains supported by some of the world's most powerful long-term buyers, the speculative fuel that helped propel bullion above $5000 remains largely absent.

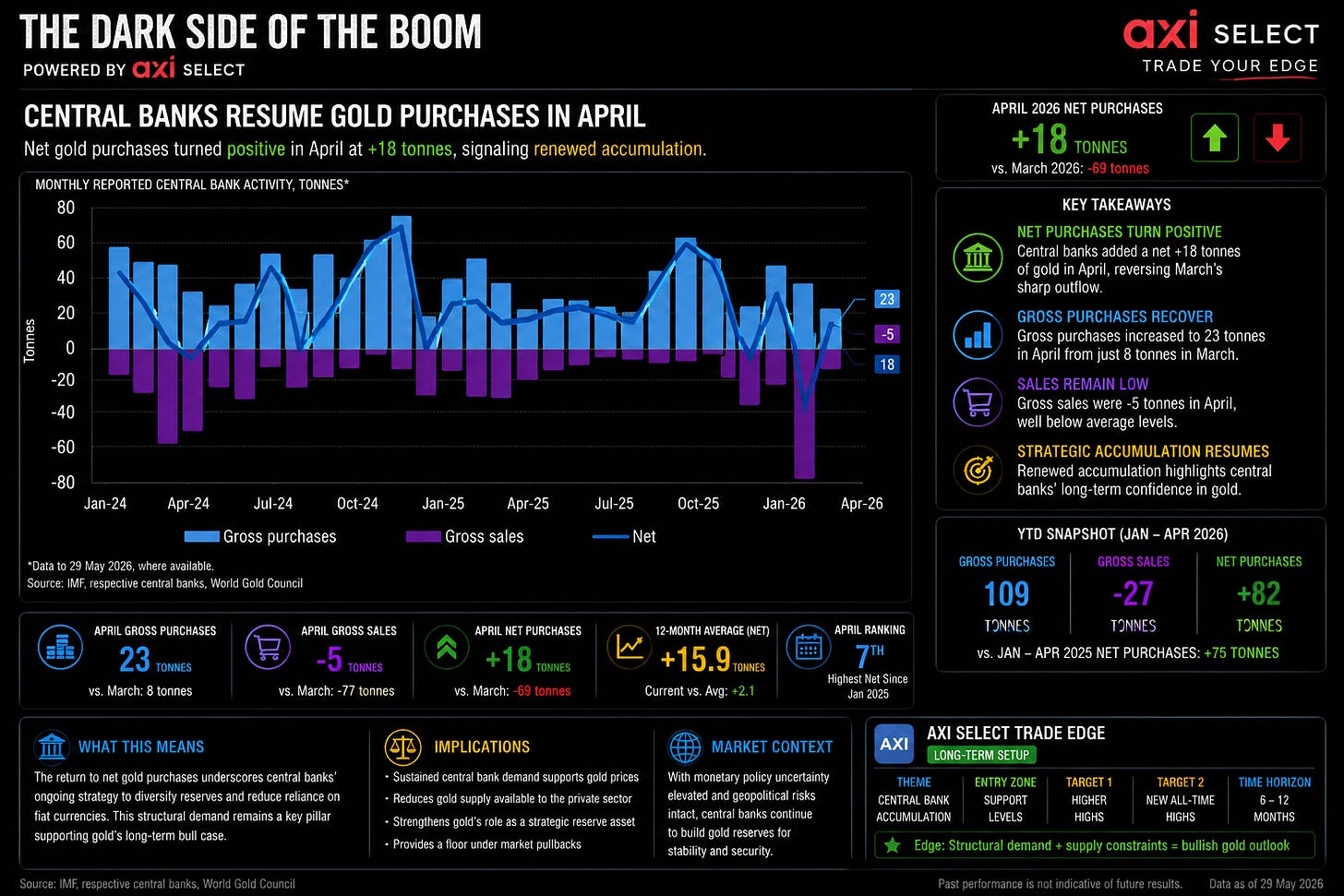

The latest World Gold Council data confirms that central banks returned to net buying in April, adding 17 tonnes after March delivered the largest monthly official sector liquidation in years, driven almost entirely by Turkey. That reversal is important because it reinforces what has become one of the defining investment themes of this decade. Central banks are no longer treating gold as a relic stored in a vault. They are increasingly treating it as financial insurance in a world where geopolitical fractures, sanctions risk, reserve diversification and questions surrounding sovereign debt sustainability have become permanent features of the landscape rather than temporary disruptions.

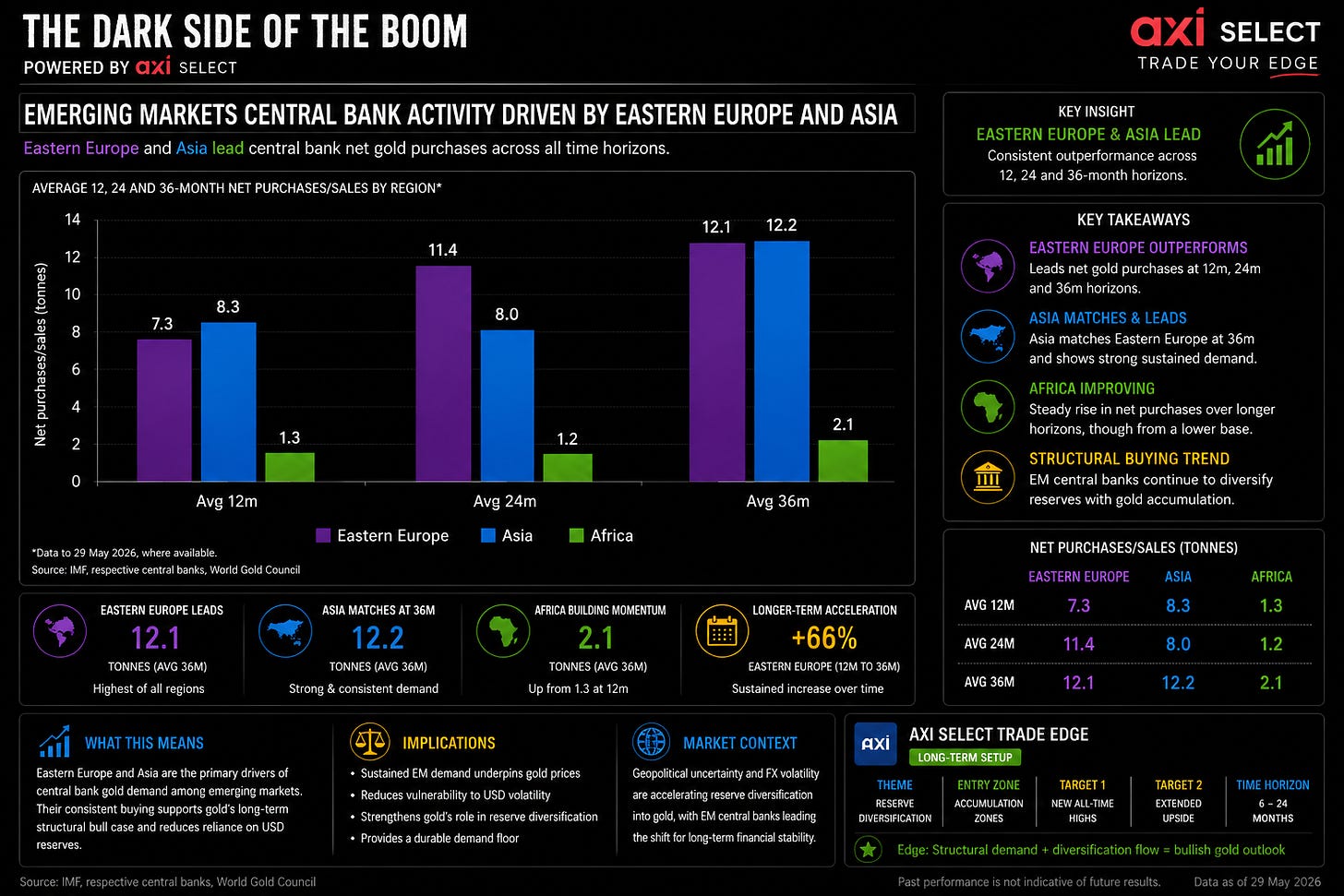

The leadership remains concentrated in familiar places. Poland once again carried much of the load, adding another 14 tonnes and bringing year-to-date purchases to 45 tonnes. China accelerated its buying program with an 8-tonne addition, the strongest monthly increase since late 2024 and an extension of an extraordinary 18-month consecutive buying streak. The Czech Republic quietly continued what has become one of the most consistent accumulation programs in the world, while Uzbekistan remains a significant net buyer despite modest sales during April. Across Eastern Europe and Asia, central banks continue to absorb gold with remarkable consistency, creating a structural bid beneath the market that has now persisted for years.

That is the part of the story that many investors understand. The part they may be missing is that central bank buying and price momentum are not the same thing. Central banks are the foundation of the house. Momentum investors are the rooftop extension. One provides stability. The other creates acceleration. At the moment, the foundation remains solid, but the extension crew has largely packed up and gone home.

That is why gold has struggled despite a backdrop that would normally appear supportive. The market is no longer trading the structural story. It is trading the immediate headwinds. Treasury yields continue to grind higher, the dollar has regained its footing, and the US economy remains surprisingly resilient despite elevated energy costs. In market terms, the discount rate is rising faster than the fear premium. When that happens, gold often finds itself swimming against the current regardless of how attractive the longer-term destination may appear.

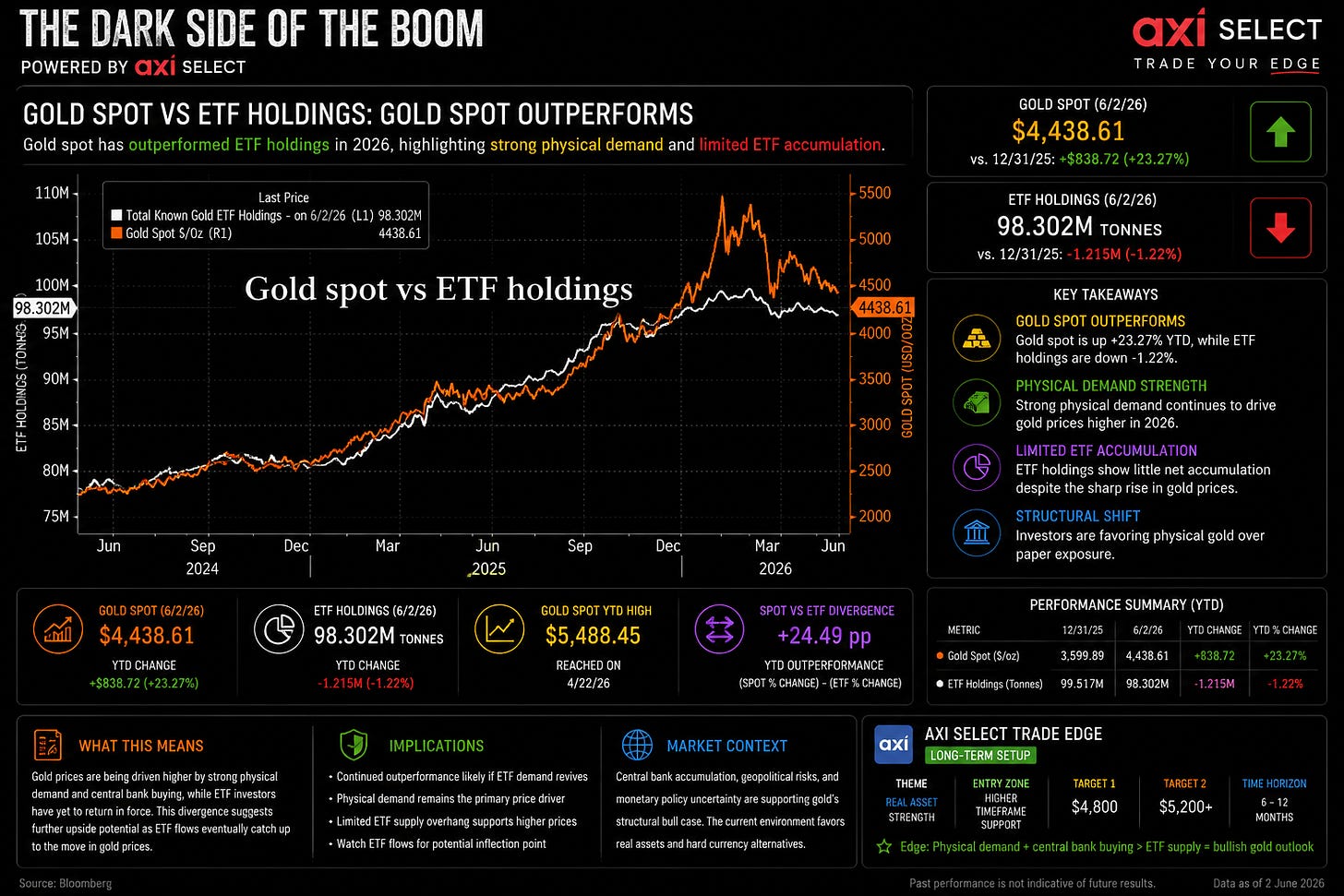

The missing piece, as usual, remains ETF demand. Last year’s explosive rally was not powered solely by central banks. It was amplified by a wave of momentum-driven investment flows that transformed a steady accumulation story into a full-scale melt-up. Today that liquidity is chasing a different dream. The speculative crowd that once piled into bullion has redirected its attention toward artificial intelligence, semiconductors, memory stocks and the broader technology ecosystem. Markets have a habit of behaving like migratory birds. Capital rarely stays in one field forever. It simply follows the next source of excitement.

That dynamic helps explain why gold can simultaneously enjoy strong official sector demand and yet struggle to maintain upward momentum. The strong hands are still accumulating. The fast hands have moved elsewhere. For now, the market is rewarding growth narratives more than defensive reserve accumulation.

Adding to recent pressure was another headline-driven scare surrounding the Reserve Bank of India. Reports suggesting the RBI had sold roughly $12 billion in gold reserves triggered another round of selling and renewed speculation about official-sector demand. Yet the story quickly unravelled. The RBI explicitly denied the reports, confirming that its physical gold holdings remain unchanged at 880.52 tonnes. What changed was valuation, not ownership. Rising and falling market prices altered the reported value of reserve assets, but the underlying gold itself never left the vault. In other words, the market briefly mistook accounting movement for physical liquidation.

That distinction is critical because it reinforces a broader point. The structural buyers have not abandoned the market. If anything, the official sector continues to demonstrate remarkable commitment to reserve diversification, albeit at a fraction of last year’s average pace. What has changed is not the destination but the speed of travel. The convoy is still moving forward, just no longer with the same urgency that characterized last year’s surge.

For traders, this creates a fascinating tug-of-war. On one side stands a powerful long-term reserve-allocation story, supported by central banks that continue to treat gold as strategic financial ballast. On the other stands a market wrestling with higher yields, a stronger dollar and the gravitational pull of technology-driven speculation. Until ETF inflows return and momentum capital rediscovers bullion, gold may remain trapped between those two forces.

The irony is that the very factor weighing on gold today could eventually become its next catalyst. The higher yields climb, the more debt servicing costs rise. The stronger the dollar becomes, the greater the pressure placed on the global financial system. Those forces may support the dollar in the short run, but they are precisely the conditions that have encouraged central banks to diversify reserves in the first place.

The market is focused on the weather. Central banks are focused on climate. Right now, the weather is cloudy for gold. The climate remains extraordinarily bullish.

Comments

Log in or sign up to join the conversation.