After several weeks of consolidation and a technical breakout that had convinced many market participants that gold’s bull cycle was over, the yellow metal has just gained nearly $240 in just a few trading sessions. This move warrants close attention, as it appears to reflect much more than a simple rebound in an oversold market.

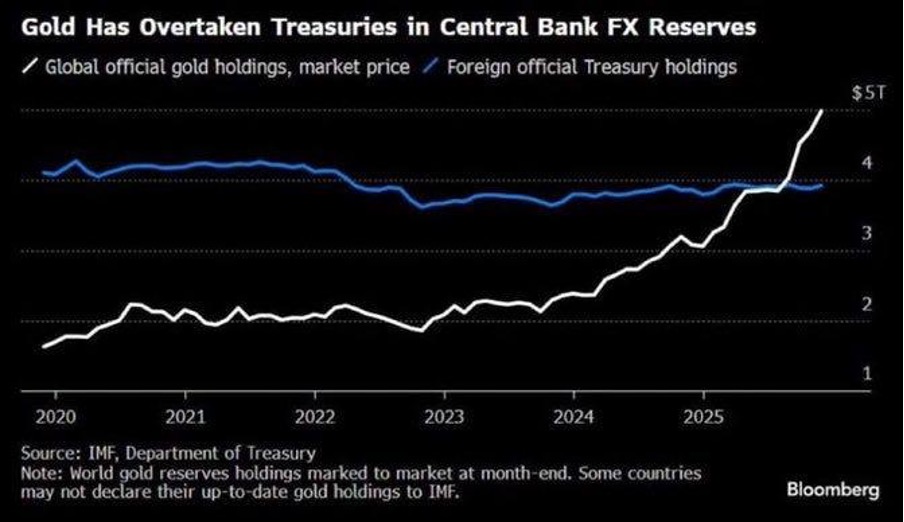

The first explanation lies with central banks. The Bloomberg chart is particularly revealing: for the first time in recent history, the value of official gold reserves held by central banks exceeds that of their holdings of U.S. Treasury bonds:

This symbolic shift marks the culmination of a trend that began after Russian reserves were frozen in 2022 and has been accelerated by the current geopolitical fragmentation.

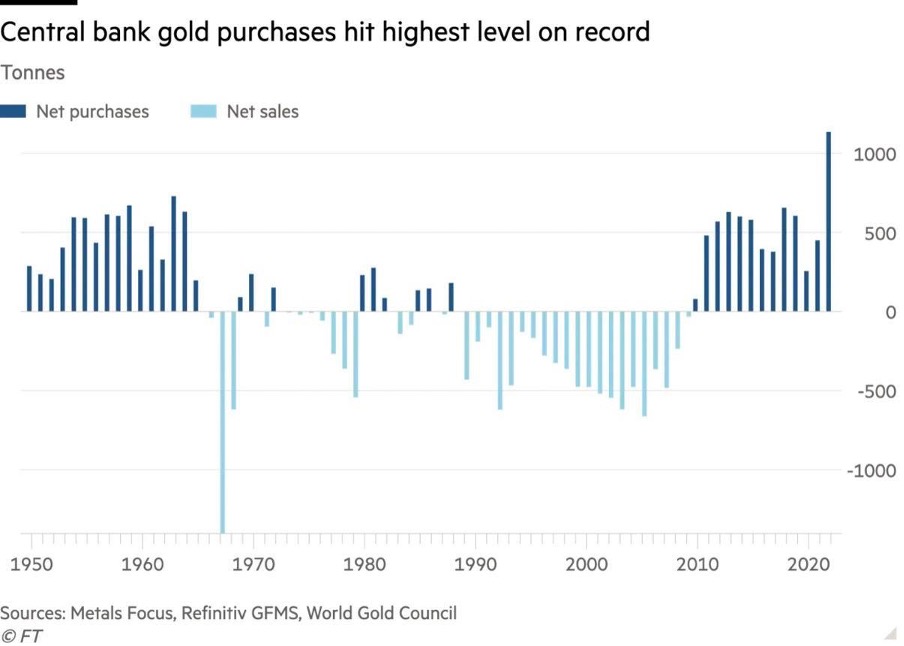

According to the latest survey by the World Gold Council, central banks have purchased an average of nearly 1,000 metric tons of gold per year over the past four years — twice the rate observed during the previous decade:

Even more significantly, 89% of the central banks surveyed expect global gold reserves to continue rising, while 45% plan to increase their own holdings over the next twelve months. The motivations remain remarkably consistent: protection against crises, diversification of reserves, a hedge against inflation, and, increasingly, protection against geopolitical risks.

At the same time, expectations regarding the dollar continue to deteriorate. Nearly three-quarters of the central banks surveyed believe that the greenback’s share of global reserves will be lower five years from now. This does not signal a collapse of the international monetary system, but rather a gradual rebalancing in which gold appears to be one of the main beneficiaries.

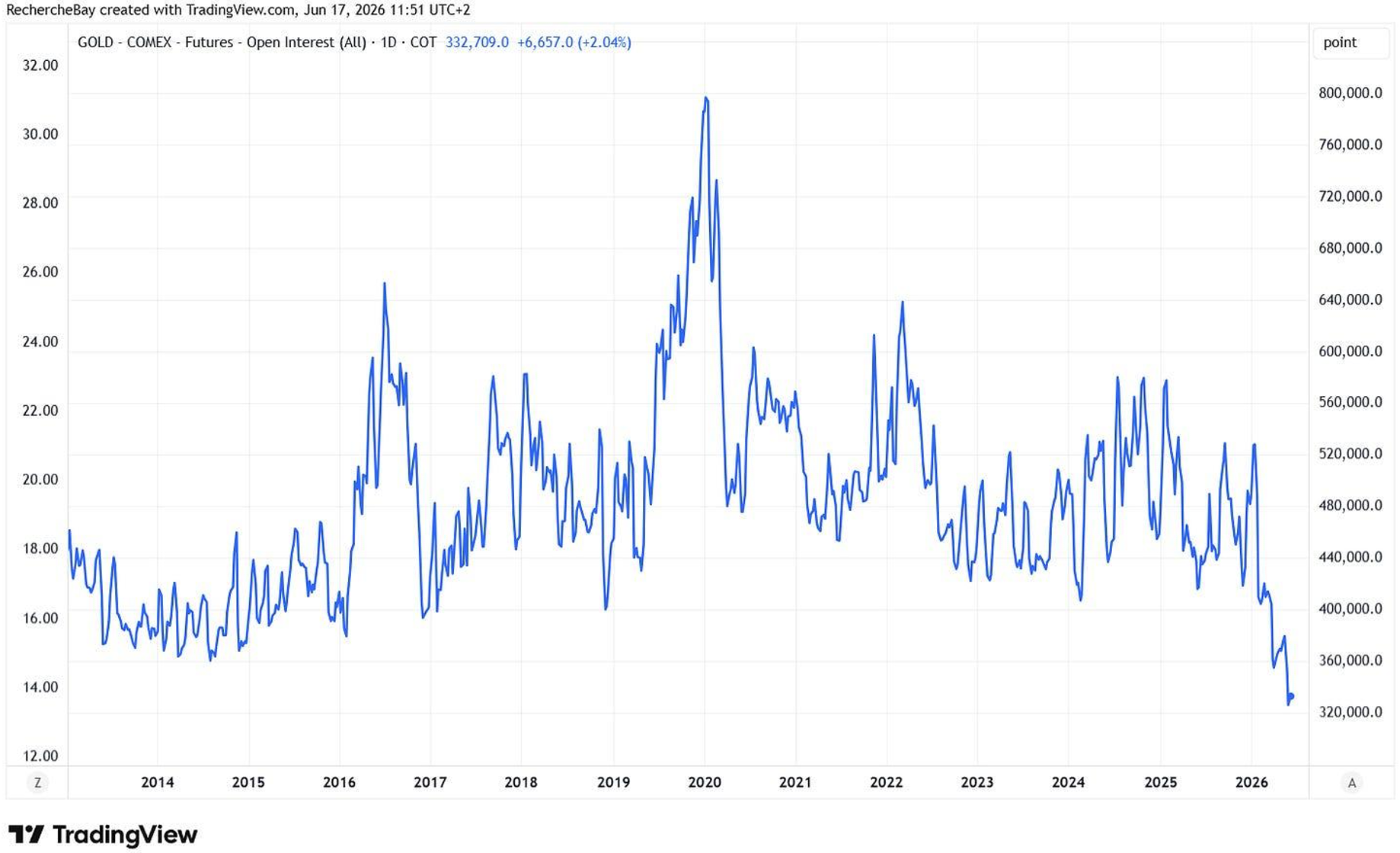

Recent behavior in the futures market reinforces this interpretation. Even as India reportedly sold nearly $12 billion worth of gold on the market, the price per ounce rose by about 5% between Friday and Monday.

Even more surprising is that COMEX’s open interest declined slightly during this rally. Normally, a sustained rise in prices is accompanied by an increase in open interest, a sign that new buyers are entering the market. This time, however, the opposite occurred.

This pattern suggests that the move was primarily driven by short covering. Hedge funds and CTAs had massively increased their bearish bets after the 200-day moving average was broken. But when the market refused to extend its decline despite these aggressive sales, those same players were forced to unwind their positions in a hurry, fueling a powerful short squeeze.

This dynamic is particularly interesting because it means that the current rebound is not yet driven by a massive return of traditional investors. ETF inflows remain modest, institutional allocations remain low, and quantitative models are still largely underinvested. In other words, a large portion of the sellers has already exited the market, while long-term buyers have not yet returned in force.

The contrast is striking: while central banks are quietly continuing to accumulate physical gold at a historic pace, financial markets continue to favor a handful of stocks linked to artificial intelligence. Yet, behind the euphoria of the indices, gold is sending a different message. It suggests that demand for the ultimate reserve asset remains intact in an environment marked by record budget deficits, persistent geopolitical tensions, and a gradual questioning of the dollar’s role as the sole pillar of the global reserve system.

The recent shift in sentiment toward gold is particularly interesting. After the euphoria seen at the start of the year — when every price rise seemed to confirm a bullish consensus that had become nearly unanimous — the narrative has changed radically. Some commentators now argue that gold has become “bad money,” sacrificed by investors to finance the most speculative initial public offerings of the moment. Yet history shows that gold is never bad money: it remains the only monetary asset that weathered cycles, crises, and changes in monetary regimes.

Even more interestingly, most sentiment and positioning indicators have now shifted into a zone of extreme pessimism. Open interest in gold has fallen to levels comparable to — or even lower than — those seen during the major low of 2015–2016. Futures trading volumes have plummeted, sentiment indicators among professional investors are near all-time lows, and most technical analysts have abandoned the sector following the break below long-term moving averages. This type of environment never guarantees an immediate rebound, but it often corresponds to phases where sellers have already largely exited the market.

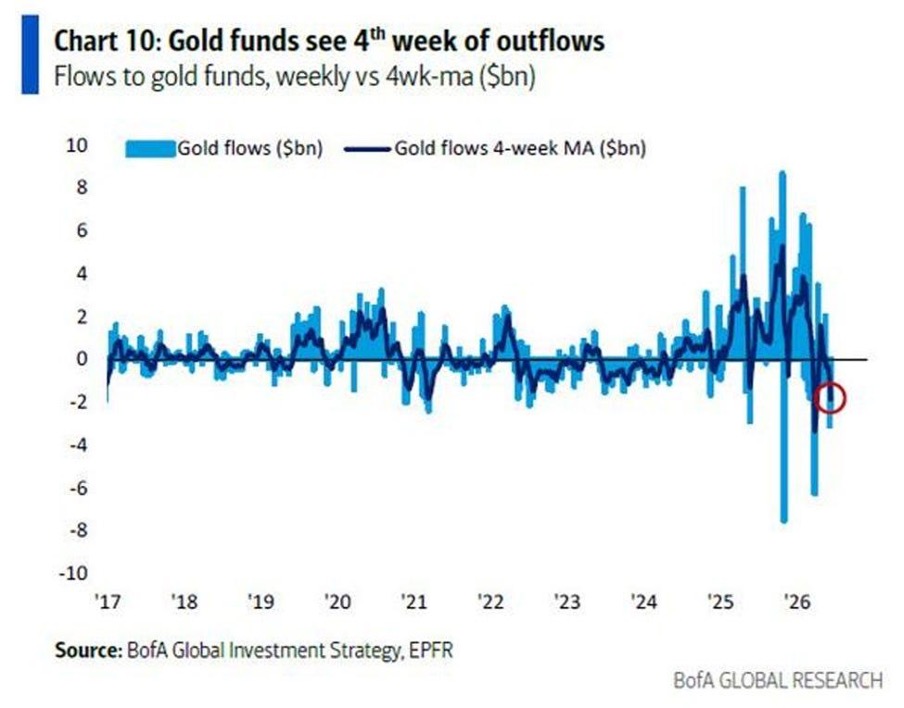

Against this backdrop, ETF flows continue to send a paradoxical signal. Gold-backed funds have recorded several consecutive weeks of capital outflows, at a rate among the highest seen in recent years.

The world’s leading gold ETF has also seen significant outflows since the start of the year, suggesting that a significant portion of Western investors has taken advantage of the recent consolidation to reduce their exposure to gold. Typically, such a move would result in a much more pronounced price correction.

However, despite these persistent sales and the markets’ hope for a geopolitical agreement that could ease certain international tensions, gold has not only held its ground but has recently rebounded strongly.

This divergence between financial flows and price movements is particularly revealing. It suggests that sales by Western investors are being absorbed by more structural demand, driven in particular by central banks and Asian buyers.

It also leaves open the possibility that the market has become excessively pessimistic, where a significant portion of short positions could be forced to cover if the long-awaited normalization scenarios continue to be postponed.

In this context, the gold market could paradoxically find itself facing a powerful short squeeze, fueled not by the arrival of new speculative buyers, but by the gradual exhaustion of sellers.

The current rebound could therefore be just the first step in a broader trend: one driven less by speculation than by a structural reallocation of global reserves and the gradual disappearance of the most aggressive sellers.

Comments

Log in or sign up to join the conversation.