We're looking at two weeks of November rain here in the UK and, to misquote Guns N' Roses, prepare for November strain as the Brexit-centered election campaign ignites and GBP is caught in limbo. The dollar may face more hurdles on the back of grim data and broadly supported risk appetite. A possible RBA hawkish tilt could pave the way for a rally in AUD.

Guns N'Roses made November Rain famous

- The frequency of market-moving data releases is going to be much lower in the coming week. Only retail sales and German industrial production (both for September) are on the eurozone agenda while the ISM Non-Manufacturing and the University of Michigan sentiment index will be in the spotlight for the US. The ISM read will likely be pivotal as markets hope to cement their expectations that the Fed will stay put in December; a clear rebound in the gauge will be needed to dissipate fears that the slowdown in manufacturing has expanded to the service sector. Our economists see the risk of a weaker-than-expected read that may revive some expectations for a December cut (with the latest ISM manufacturing indicating a recession in the sector and keeping the case for a cut in place).

- Markets will also await more details on trade talks and on President Trump’s impeachment process. The latter may continue to have a quite limited market impact, whereas a number of sticky points (as well as a timetable, after the APEC meeting got cancelled) are still to be outlined in the “phase-one” US-China trade deal. We still see the risk of markets having misplaced their optimism for a breakthrough in trade tensions, although we expect the news flow on trade to remain broadly supportive for risk sentiment this week. All this may translate into another unlucky weak for the dollar and give another chance for EUR/USD to crawl back above 1.12.

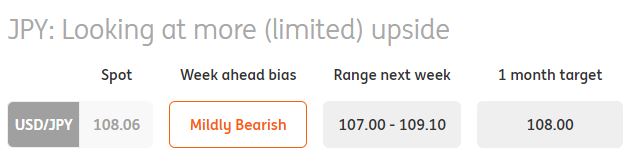

- The yen has staged a solid one-figure gain vs the USD this past week on the back of the “hawkish” cut delivered by the Fed. The BoJ also came to the rescue of the currency by not cutting rates, although it sensibly trimmed its forecasts for inflation and growth. Currently, markets are torn about a 10bp cut in December (53% priced in the OIS curve).

- In such supported risk environment, neither the dollar nor the yen is likely to have an easy time next week. Of the two, the dollar is probably richer in negative catalysts (a possibly weak ISM non-manufacturing, for instance), which suggests the risk for USD/JPY may be slightly tilted to the downside this week. We expect the pair to keep edging lower and establish itself in the 107-108 area while waiting for a new clear catalyst (likely, on the trade front) in the coming weeks.

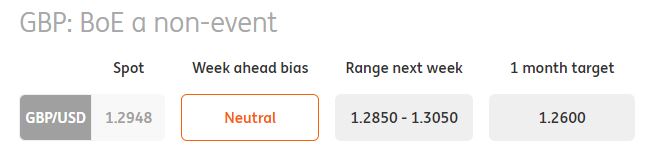

- A very eventful week in the UK has set the sterling for a 1% gain before trapping it in a relatively narrow range. Parliament has voted to send Brits to the polls on Thursday 12 December, and all parties are gearing up for what will be a Brexit-centred electoral campaign. Sterling’s recent strength suggests that the markets are positioned for a Conservative majority win, which would ultimately allow incumbent PM Johnson to have his deal ratified by the House. However, the vulnerability of the Conservatives in Scotland and some Southern-English areas suggests more caution, and we wouldn’t rule out a Labour-led minority or a hung parliament as a result (though this is an outside risk at this point). For now, as long as opinion polls continue to point in the direction of a Tory triumph, it seems unlikely to see GBP fiercely correct lower just yet.

- In this context, the Bank of England meeting (Thursday) will once again be quite an uninteresting one, with the MPC likely sticking to a cautious approach ahead of lingering uncertainty ahead. With some signs that the jobs market is no longer tightening, the pressure to unfold monetary stimulus is probably lower and allows more time for policymakers to assess the internal and external backdrop before adjusting rates.

- The Australian dollar has staged consistent gains this week, taking advantage of stable risk appetite and an encouraging inflation read, that allayed the lingering doubts on whether the RBA will keep rates on hold next week. The market is now pricing in only a 6% probability of a cut next Tuesday, so most of the reaction will likely be driven by the Bank’s forward-looking language. Our base case is that the RBA will refrain from any more cuts at least through the end of 2019, so we would not be surprised to see Governor Lowe providing some indications of a more extended pause in the easing cycle. Alternatively, he may well err on the side of caution and keep the door open for more cuts, whilst expecting developments in the inflation and employment spheres as well as on the global trade backdrop.

- We think that a further stabilisation in risk sentiment and the possibility of a hawkish shift by the RBA suggests that the balance is skewed to the upside for AUD/USD in the next week. The 200d MA at 0.6955 should, however, prove to be a fairly solid resistance to AUD rallies for now.

Comments

Log in or sign up to join the conversation.