Key Market Outlook(s) and Pick(s)

On Monday, I joined the great David Asman on Fox Business’ Varney & Co. to discuss markets, the economy, outlook, rotation, and more. Thanks to Stuart Varney, Maggie Edwards, Nick Palazzo, and David for having me on:

Video Length: 00:01:42

Canada Goose Update

For newer readers, here’s a quick overview of the key drivers behind our thesis on Canada Goose, an iconic luxury outerwear brand in the early innings of a DTC-led inflection as it evolves into a year-round lifestyle brand.

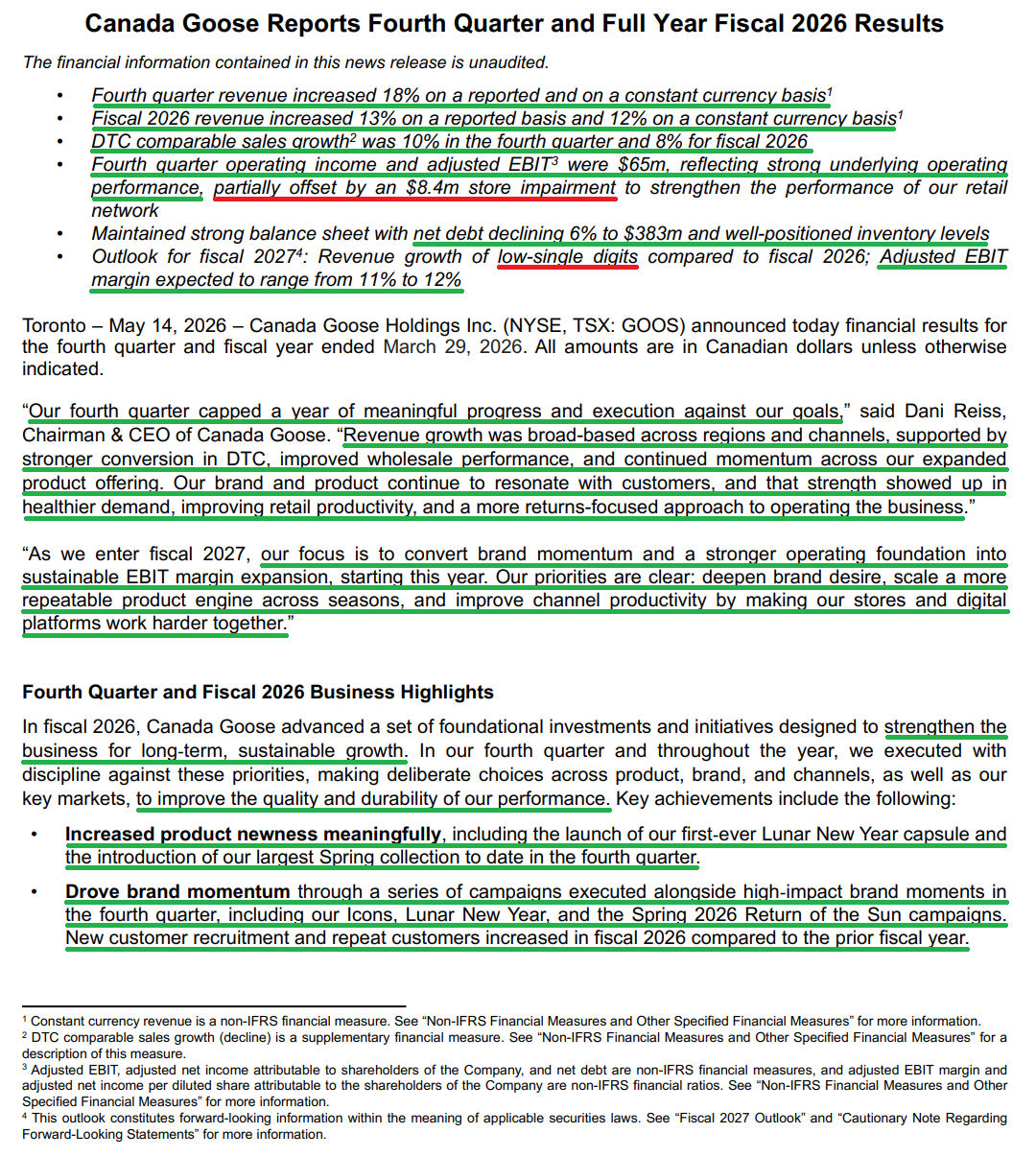

Canada Goose closed out FY26 with another quarter of strong execution, delivering the kind of results that continue to reinforce the multi-year turnaround thesis we laid out when we initiated the position.

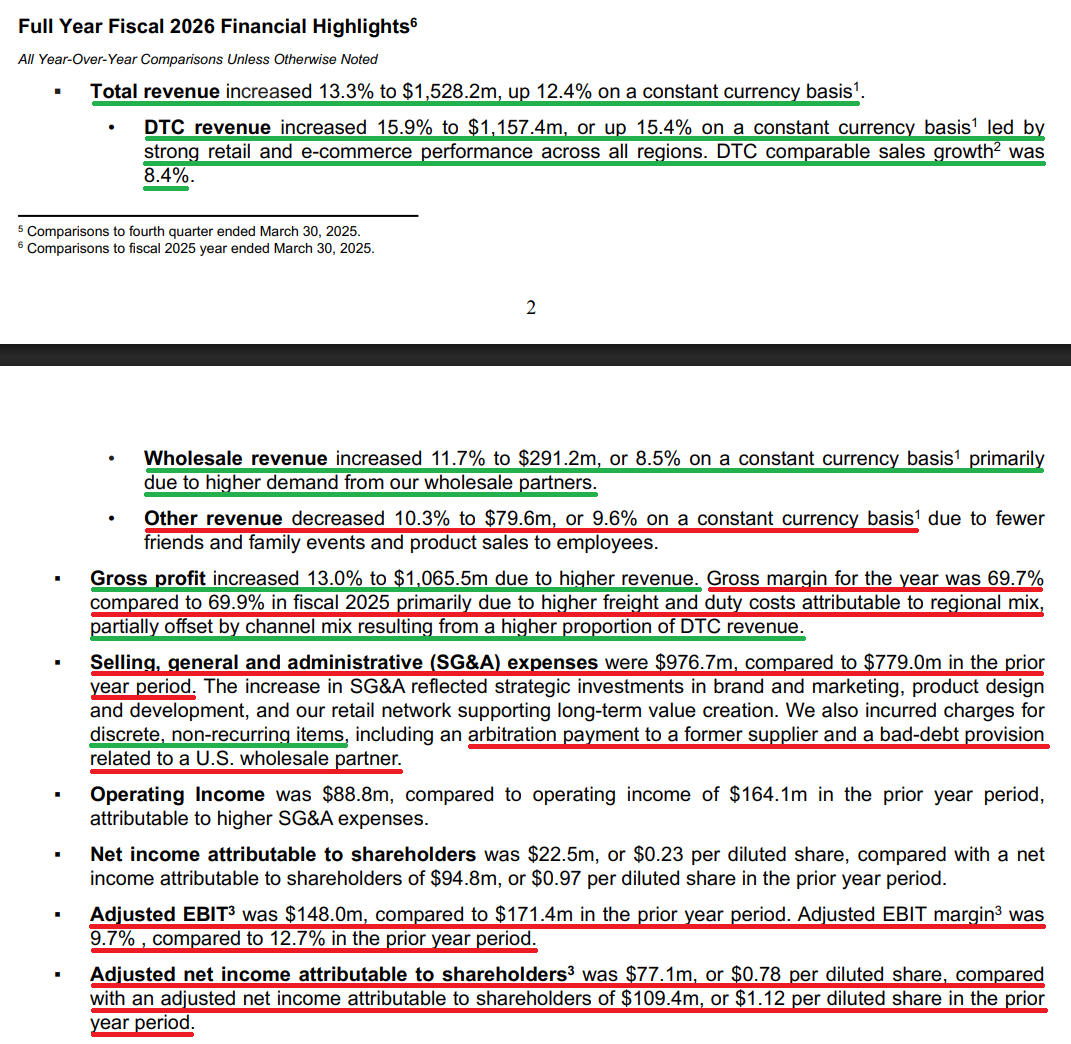

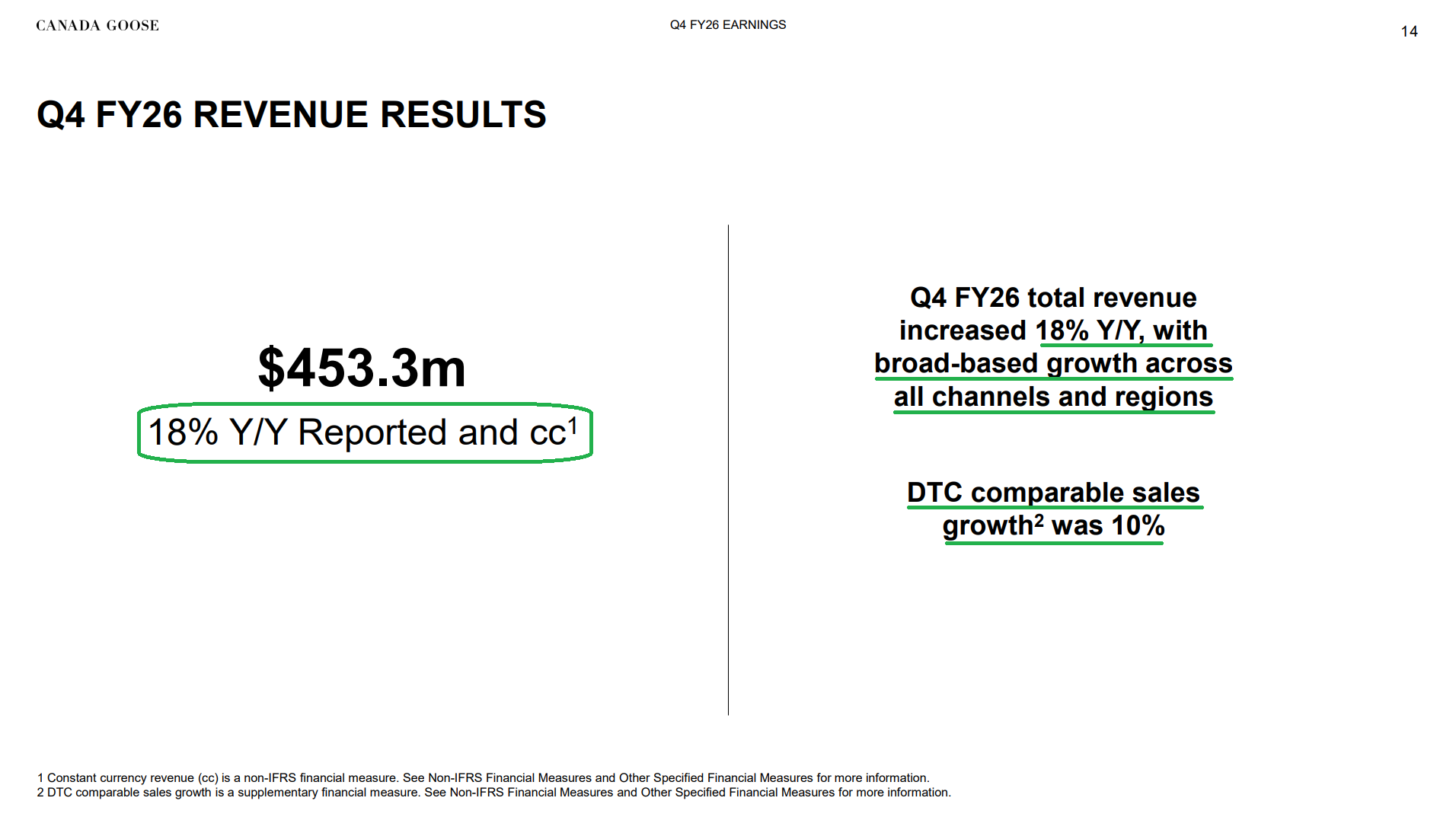

Q4 revenue jumped +17.9% Y/Y (+18.2% cc) to $453.3M, bringing full-year revenue to $1.53B, up +13.3% Y/Y and crossing the $1.5B threshold for the first time in company history. Growth was broad-based, with every channel and region contributing to the recovery. DTC comps accelerated to +10% from +6.3% last quarter, marking the fifth consecutive quarter of positive comps and bringing full-year comps to +8.4%. After revenue growth bottomed at just over +1% last year, FY26 delivered the strongest growth in more than four years, a testament to the years of heavy lifting and the foundation built for a durable top-line recovery.

That heavy lifting started with a fundamental shift in the business model. Management’s first priority was to pivot the company away from a wholesale model and toward higher-margin DTC while simultaneously transforming Canada Goose from a seasonal outerwear company built around a single $1,000-plus parka purchase into a 365-day luxury lifestyle brand.

When this pivot began in FY17, DTC represented just ~29% of revenue as Canada Goose remained heavily reliant on wholesale. Today, the channel accounts for ~76% of revenue, with management targeting ~80% by FY28. Not only does DTC command a far more attractive margin profile, generating gross margins in the mid-70s versus the mid-to-high 40s for wholesale, but it also provides greater brand control, stronger customer engagement, more disciplined inventory management, and a direct connection with consumers. As expected, the payoff is showing up where it matters most: full-year gross margin reached 69.7%, just shy of last year’s record high and up +17 percentage points from FY17.

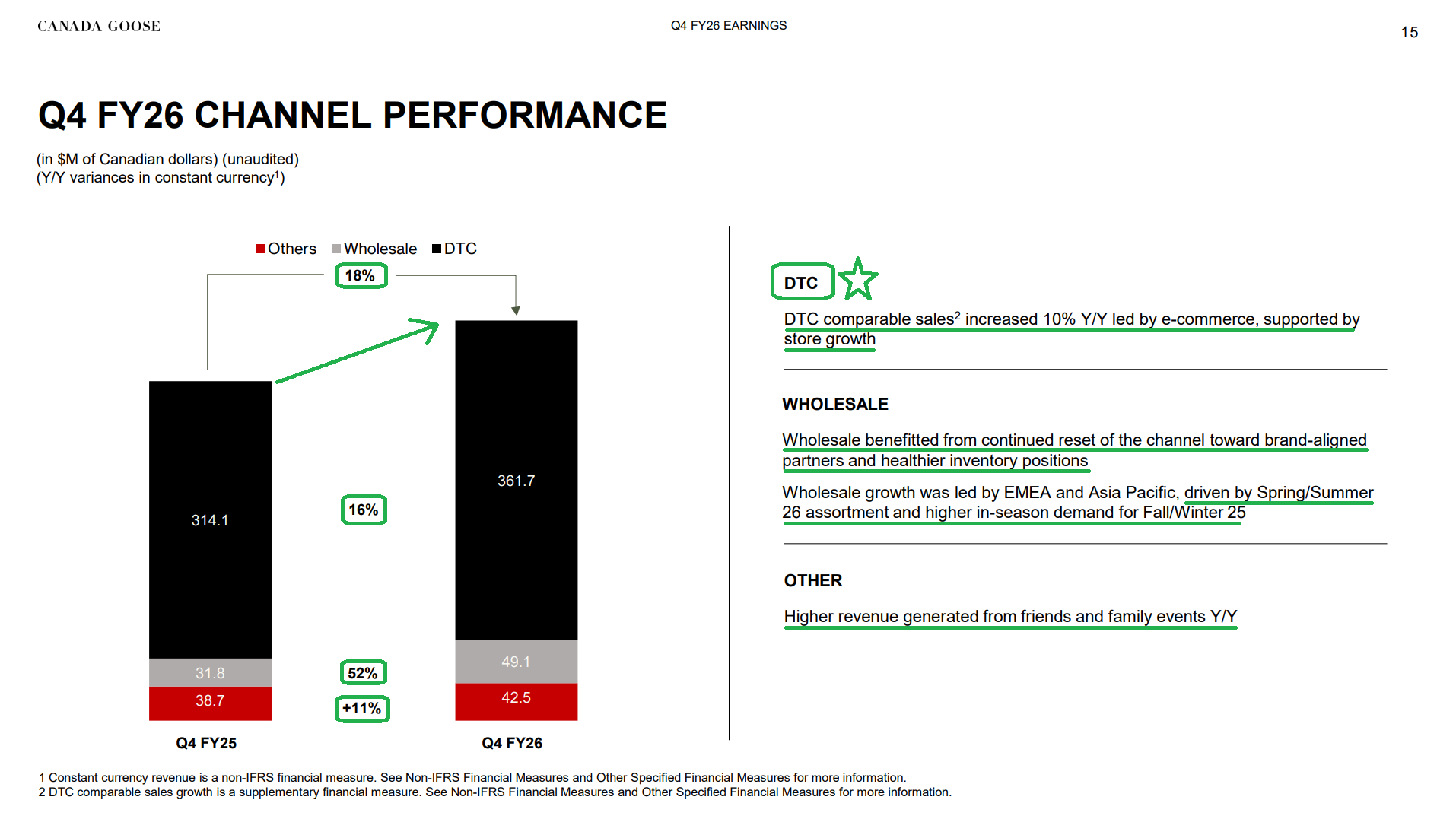

The flip side of that transformation was a deliberate reset of the wholesale channel. Over the past three years, management reduced exposure and refocused the channel around the highest-quality, brand-aligned partners, a decision that weighed on results during the transition (-6% in FY23, -16% in FY24, and -16.5% in FY25). That reset is now in the rearview mirror, with wholesale returning to growth at +54.4% in Q4 and +11.7% for the full year. Most importantly, Fall/Winter ’26 order book trends point to another year of growth ahead, serving as a leading indicator that what was once a persistent headwind has become a healthy contributor to the business.

At the same time, management has expanded Canada Goose beyond its roots as a winter-only outerwear company. Less than 15 years ago, down-filled outerwear represented ~95% of the business, with the brand largely defined by a single flagship purchase. Today, that category has fallen to roughly half of revenue as the company has expanded into a broader lifestyle assortment spanning apparel, lighter-weight outerwear, accessories, and other everyday products. Rather than diluting the core, a challenge where many brands have stumbled, Canada Goose has extended the brand across more occasions, more seasons, and more price points while continuing to strengthen its core down-filled outerwear business.

The strategy continues to resonate with consumers, with apparel leading category growth in Q4 and for the full year. The launch of the company’s largest-ever Spring/Summer ’26 mainline collection, brought to market earlier than in prior years to strengthen brand presence through the shoulder season, helped extend engagement beyond peak winter. New customer acquisition, repeat customer counts, and purchase frequency all improved in FY26, delivering exactly the customer behavior management set out to create.

Together, these initiatives have laid the groundwork for a durable top-line recovery, which is now well underway. With the business model reset largely behind it, the focus shifts to margin expansion, the final piece of the GOOS turnaround story.

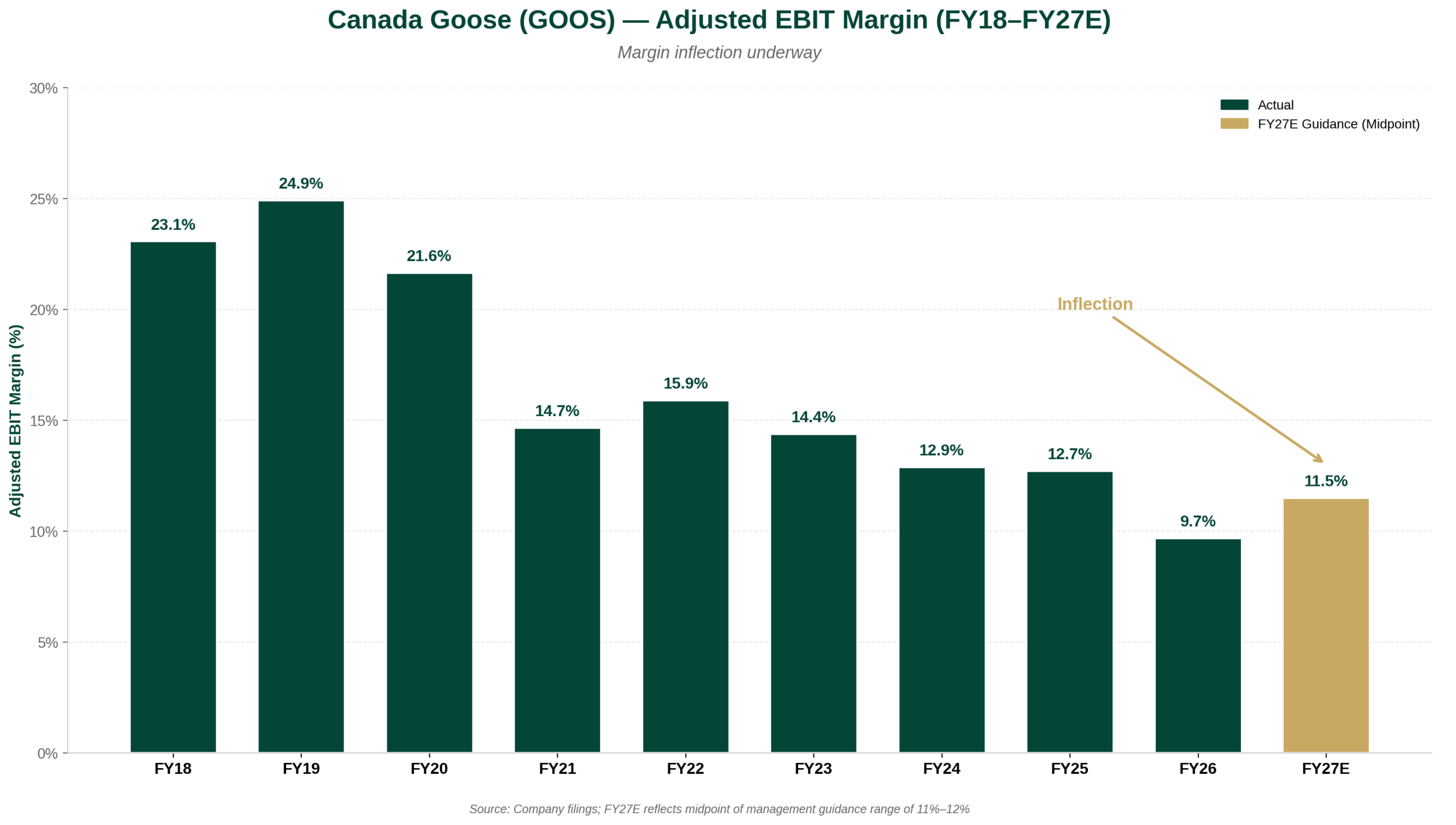

Adjusted EBIT margin peaked at 24.9% in FY19 before steadily declining through a combination of cyclical pressure, operating deleverage during the company’s slower growth period, and the investment cycle behind the company’s DTC transition and brand expansion. FY26 marked the trough in the company’s public operating history, with adjusted EBIT margin falling to 9.7%, weighed down by a slew of one-off headwinds totaling ~$67M: a $43.8M arbitration award payment, a $15M U.S. wholesale bad debt provision, and an $8.4M Q4 store impairment charge.

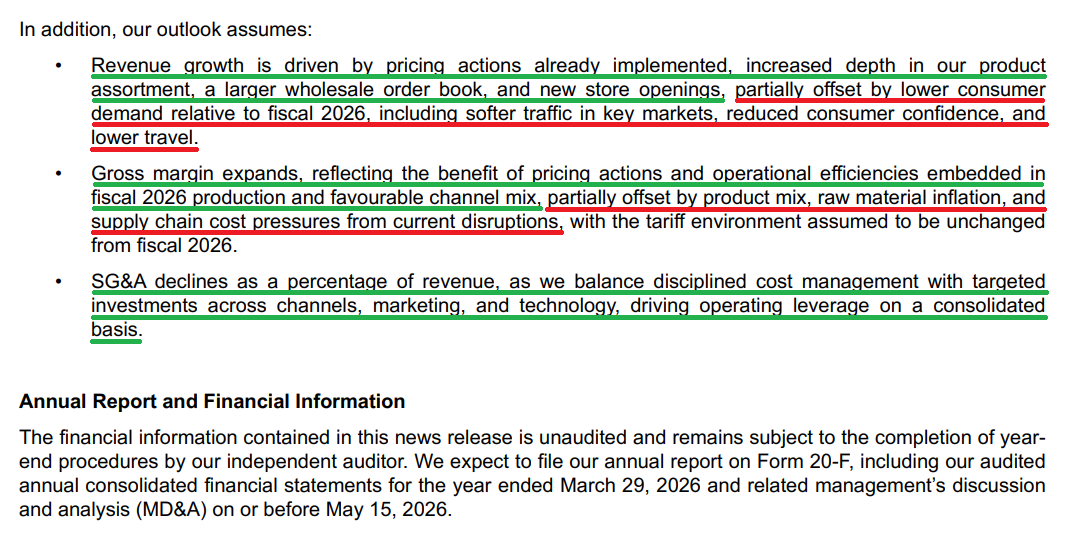

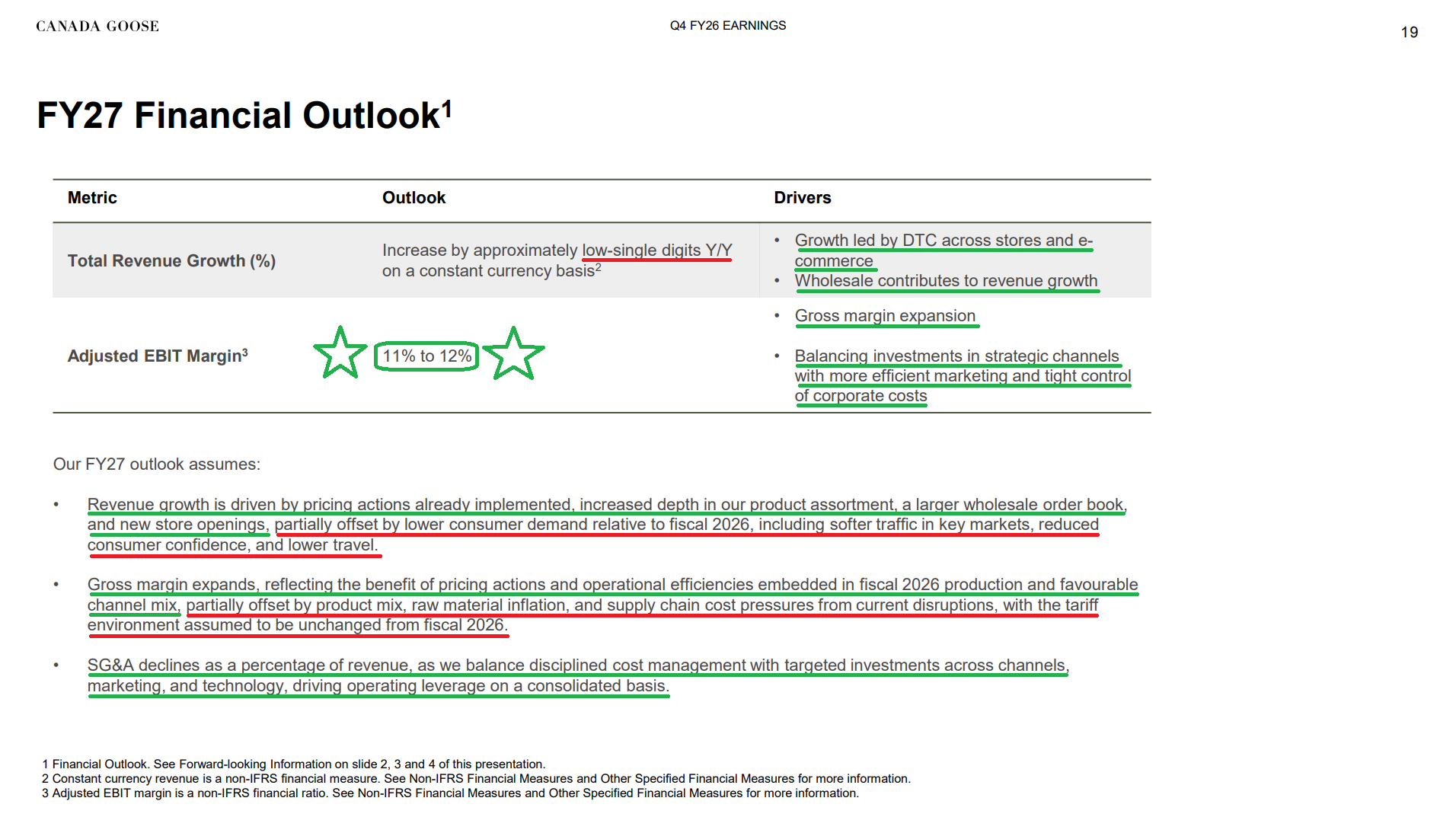

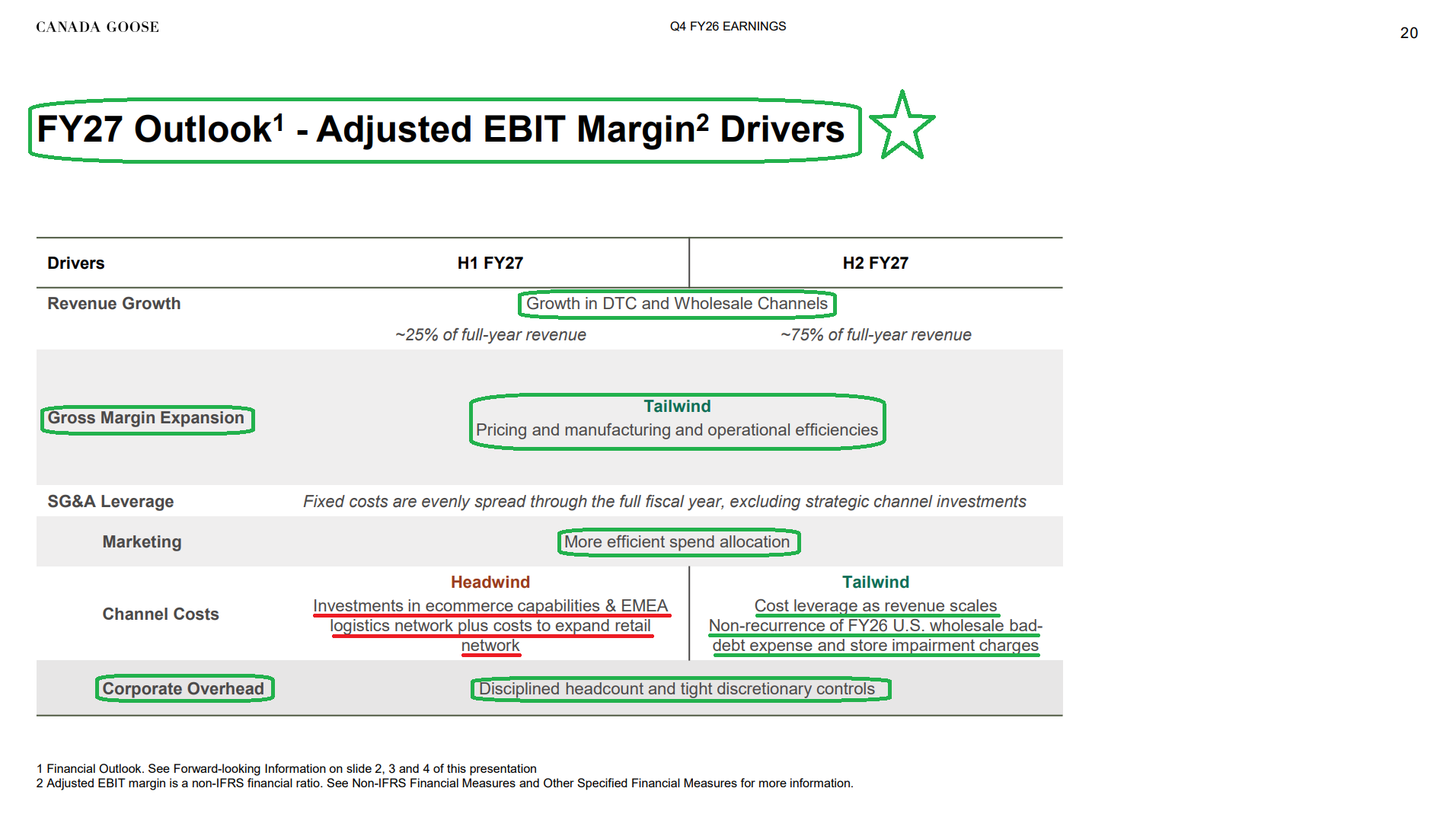

FY27 should mark the first step in the margin recovery, with management guiding adjusted EBIT margin to 11-12%, representing +130 to +230 bps of expansion from the FY26 trough. While the absence of last year’s one-off charges provides an initial tailwind, the biggest opportunities to drive margin expansion come from self-help levers already embedded throughout the business: pricing actions already implemented, manufacturing and operational efficiencies, lower marketing spend as prior investments begin to pay off, and disciplined corporate cost control driving operating leverage.

Management has been clear that they see no structural reason the business cannot work back toward historical margin levels under the current operating model. We believe management has earned the benefit of the doubt given the progress made across the first stages of the strategy. Even if the shift toward a DTC-led model ultimately limits a full return to historical peak margins, a path back toward the mid-teens over the next several years appears well within reach and, in our view, would unlock significant earnings power while providing the catalyst for a meaningful re-rating.

The market, for its part, remains firmly in the show-me camp, unconvinced the profitability story will unfold as smoothly as management expects. We are happy to take the other side. We have watched this management team execute the first two phases of the strategy almost flawlessly, giving us confidence the final piece of the puzzle will be no different.

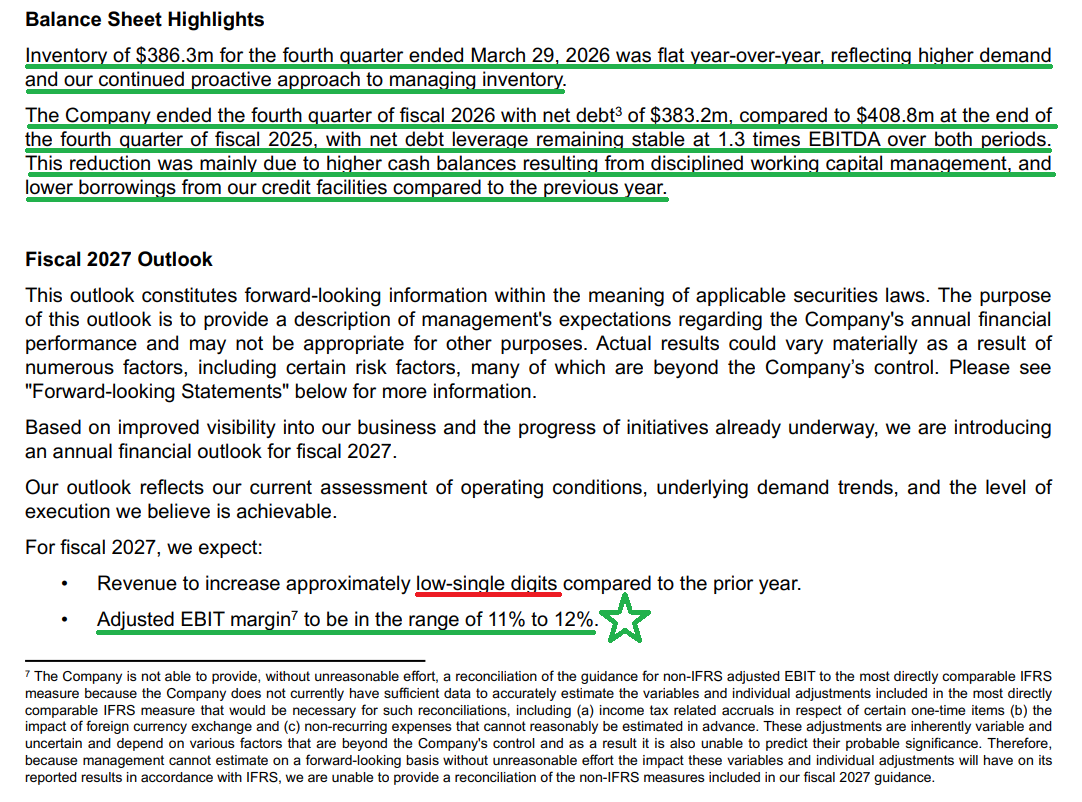

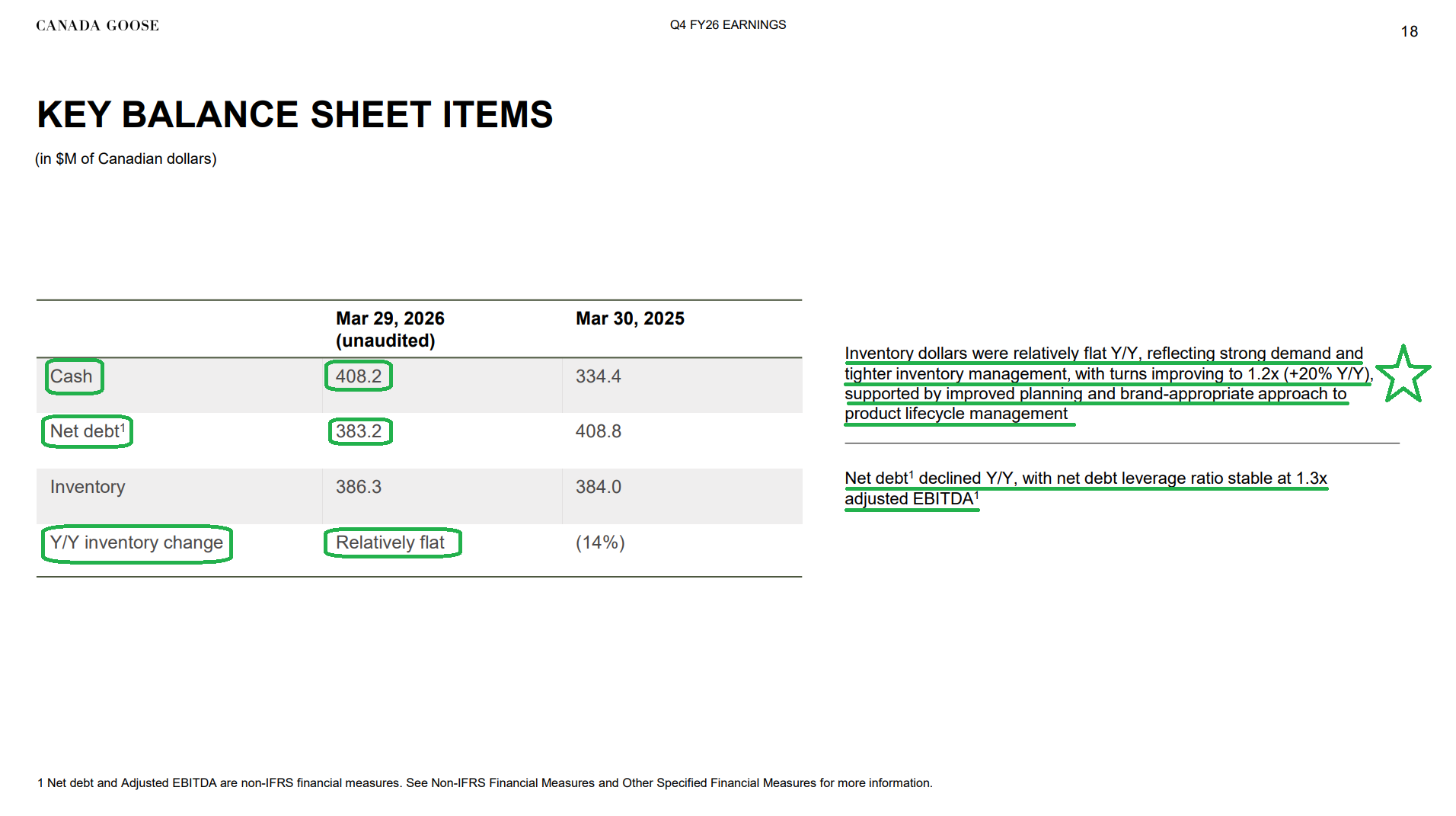

A key driver of that confidence is having a true partner at the helm, with third-generation CEO Dani Reiss maintaining massive skin in the game through his ~21% ownership stake. On top of that, the company is backstopped by a strong balance sheet, with $408M of cash, net leverage at just 1.3x EBITDA, and solid free cash flow generation providing ample runway to finish the job.

Once the margin inflection becomes obvious to everyone else, we believe the multiple will follow. GOOS trades at just ~12x forward earnings today, well below its five-year average of ~20x. We’re happy to be patient and let execution close that gap.

Q4 & FY26 Earnings Breakdown

10 Key Points

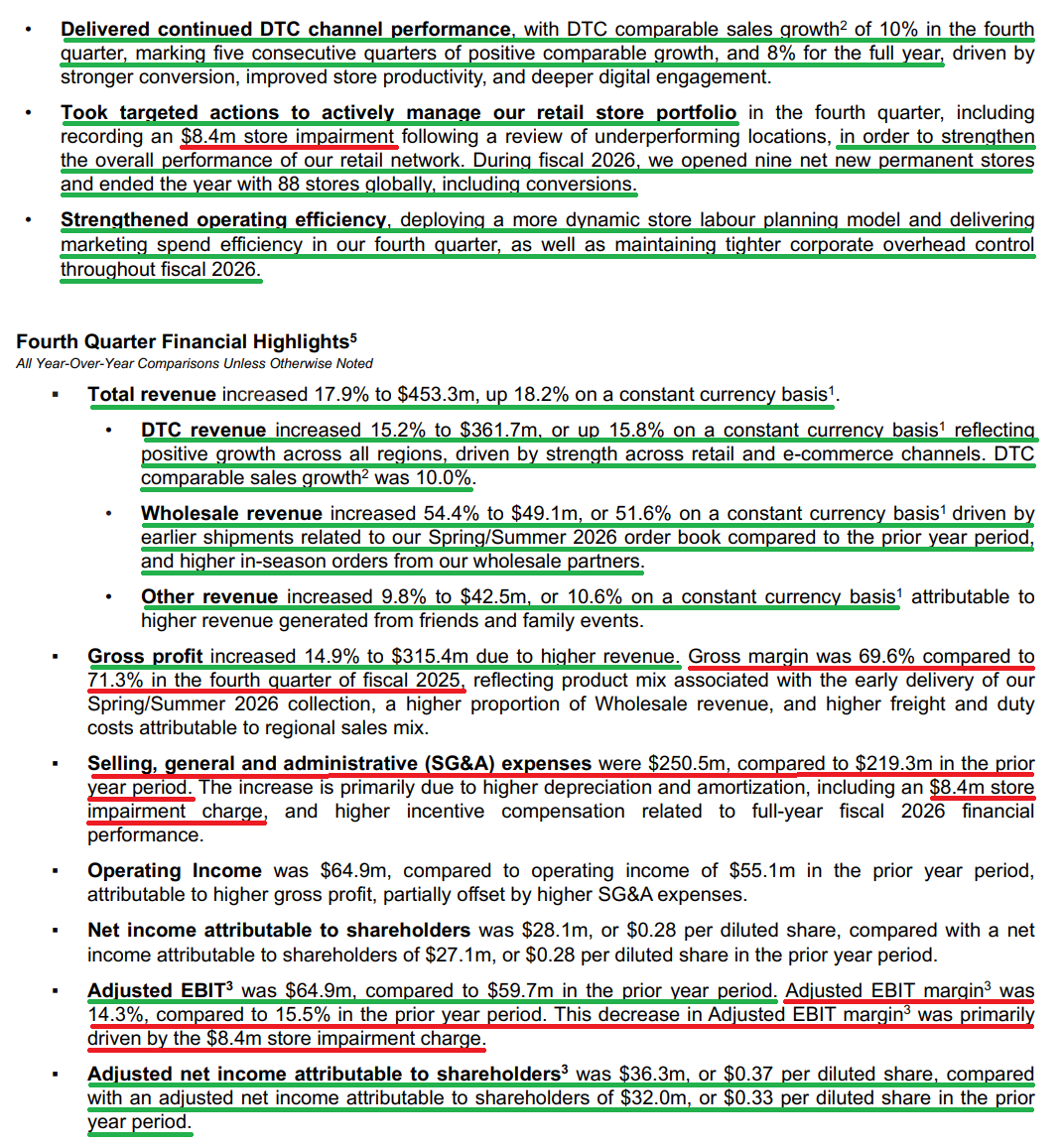

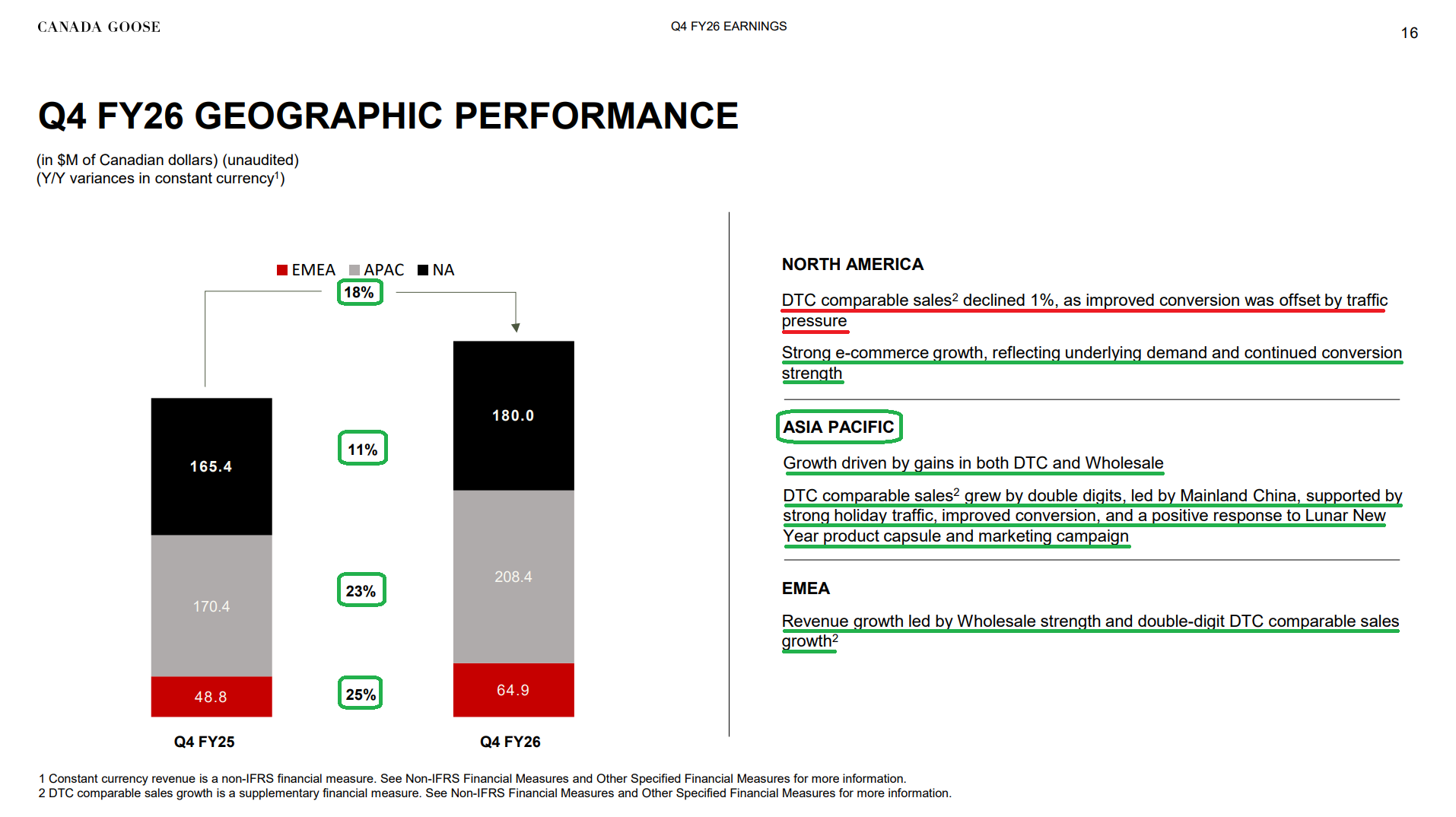

1) Canada Goose reported Q4 revenue growth of +17.9% Y/Y (+18.2% cc) to $453.3M, well ahead of consensus of $412M. Growth was broad-based across all channels and regions, with EMEA leading at +25.2%, Asia Pacific up +23.4% (Greater China +24.2%, led by Mainland China), and North America up +10.9%. For the full year, revenue crossed $1.5B for the first time, growing +13.3% (+12.4% cc) to $1.53B.

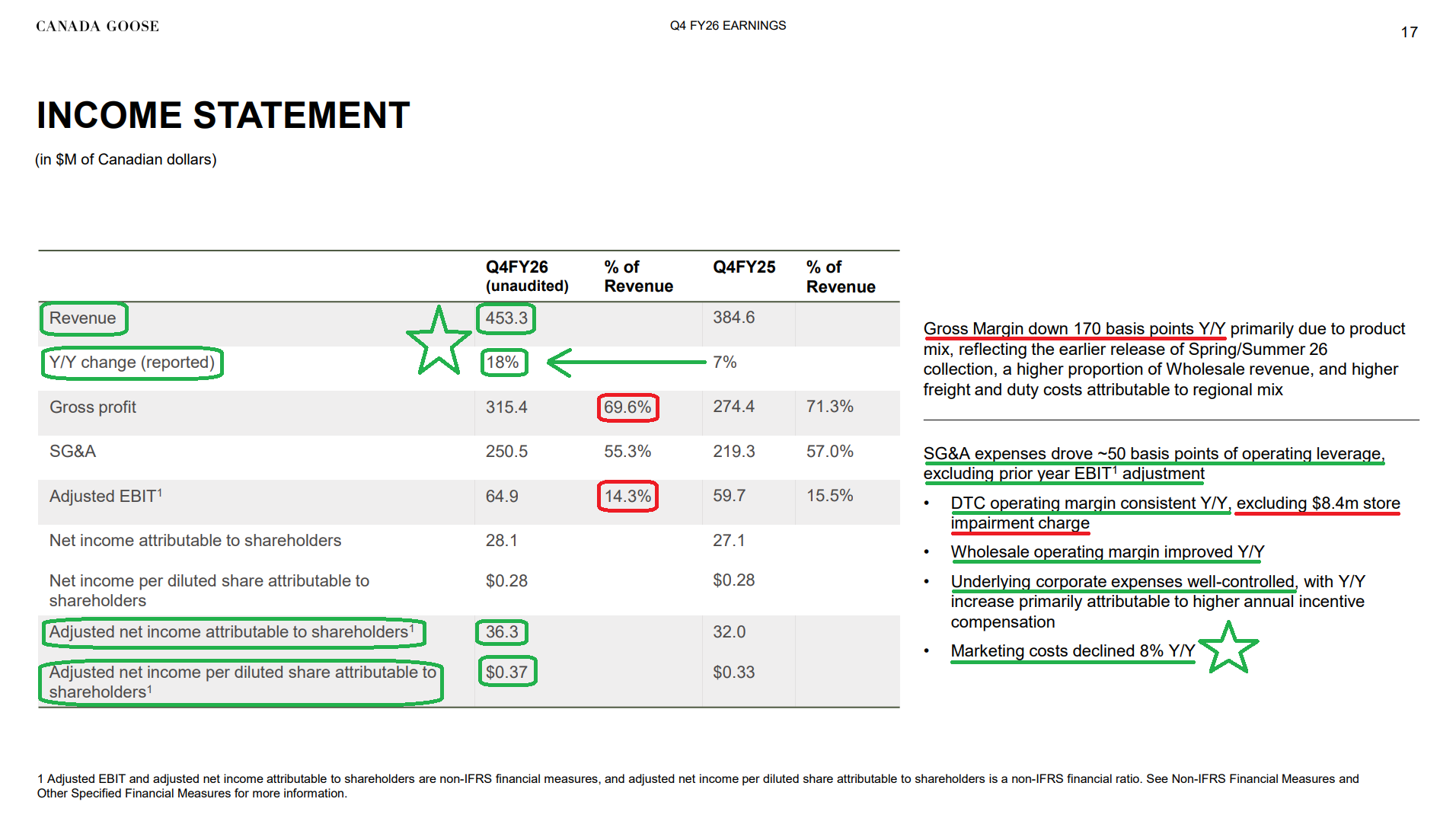

2) Adjusted net income came in at $36.3M, or $0.37 per diluted share, up from $32M and $0.33 in the prior-year period but below consensus of $0.40. For the full year, adjusted EPS was $0.78 versus $1.12 last year, with the decline driven by three discrete one-time items: the $43.8M arbitration award payment to a former supplier, the $15M U.S. wholesale bad debt provision, and the $8.4M Q4 store impairment charge related to a review of underperforming locations.

3) DTC revenue grew +15.2% (+15.8% cc) to $361.7M, accounting for ~79.8% of quarterly sales as the company continues to shift toward its higher-margin channel. DTC comparable sales accelerated to +10% from +6.3% last quarter, marking the fifth consecutive quarter of positive comps, led by e-commerce and supported by double-digit comps in both APAC (led by Mainland China) and EMEA. North America comps declined a modest 1%, as improved conversion was offset by traffic pressure concentrated in a small number of high-tourism urban locations. For the full year, DTC revenue grew +15.9% (+15.4% cc) to $1.16B, with comparable sales up +8.4%.

4) Wholesale revenue increased +54.4% (+51.6% cc) to $49.1M, led by EMEA and Asia Pacific on earlier shipments of the Spring/Summer ’26 order book and higher in-season demand for Fall/Winter ’25. Following three consecutive years of declines, the wholesale channel reset toward brand-aligned partners is now complete, with the channel returning to full-year growth at +11.7% (+8.5% cc) to $291.2M. Management pointed to encouraging Fall/Winter ’26 order book trends as a leading indicator of continued momentum, with another year of wholesale growth expected in FY27.

5) Canada Goose’s push to become an all-season, 365-day relevant brand continues to gain traction, with apparel leading category growth in Q4 and for the full year, supported by ongoing strength in its core down-filled outerwear business, which remains the majority of revenue. Management launched its largest Spring/Summer ’26 mainline collection to date and brought it to market earlier than in prior years, strengthening the brand’s presence during the shoulder season and driving more consistent engagement beyond peak winter. Both new customer acquisition and repeat customer counts increased Y/Y, alongside higher purchase frequency. Wholesale partners are seeing the same dynamic, citing strong demand for lighter-weight outerwear, everyday apparel, T-shirts, and fleece.

6) Gross profit increased +14.9% to $315.4M, while gross margin contracted 170 bps Y/Y to 69.6%. The compression was driven by product mix related to the earlier Spring/Summer ’26 delivery, a higher proportion of wholesale revenue, and elevated freight and duty costs from regional sales mix. For the full year, gross profit rose +13% to $1.07B, with gross margin holding essentially flat at 69.7% versus 69.9% last year, as pricing actions and operational efficiencies offset the same freight and duty pressures alongside the company’s deliberate push into product newness.

7) Adjusted EBIT came in at $64.9M versus $59.7M last year, with adjusted EBIT margin declining 120 bps to 14.3% from 15.5%. The decline was entirely attributable to the $8.4M store impairment charge, with underlying DTC operating margin remaining consistent Y/Y and wholesale operating margin improving. SG&A of $250.5M grew +14.2% Y/Y, slower than the +17.9% revenue growth, driving ~50 bps of operating leverage (excluding the prior-year earn-out adjustment). Marketing expense declined 8% Y/Y as earlier and more consistent FY26 spending carried brand momentum into Q4, while underlying corporate expenses remained well controlled, with the Y/Y increase primarily reflecting higher annual incentive compensation tied to strong performance against targets. For the full year, adjusted EBIT declined to $148M from $171.4M, with margin contracting to 9.7% from 12.7%, largely reflecting the previously cited one-time headwinds (arbitration payment, U.S. wholesale bad debt provision, and Q4 store impairment), with the bad debt provision and impairment alone accounting for ~150 bps of margin pressure.

8) Cash and cash equivalents increased to $408.2M from $334.4M last year, while net debt declined 6% to $383.2M from $408.8M. Net debt leverage remained stable at 1.3x adjusted EBITDA, with the improvement driven by disciplined working capital management and lower borrowings under the company’s credit facilities.

9) Inventory was essentially flat Y/Y at $386.3M despite double-digit revenue growth, reflecting strong demand and disciplined inventory management. Inventory turns improved to 1.2x, up 20% Y/Y and 33% versus two years ago, supported by better planning and a more structured, brand-appropriate approach to product lifecycle management. Management continues to see room for further improvement in inventory productivity from here.

10) Management issued FY27 guidance calling for low-single-digit revenue growth on a constant currency basis, modestly below consensus of ~4.6%. Growth is expected to be driven primarily by DTC across both stores and e-commerce, with an additional contribution from wholesale, partially offset by lower other revenue due to fewer planned friends and family events. Prudently, the outlook assumes a more cautious macro backdrop, including softer traffic in key markets, weaker consumer confidence, and lower travel, leaving room for upside should conditions improve. Adjusted EBIT margin is expected to be 11% to 12%, representing ~130 to 230 bps of expansion from the FY26 base of 9.7%, with the midpoint above the ~11.1% implied by consensus. Key margin drivers include gross margin expansion from pricing and operational efficiencies, more efficient marketing spend, disciplined corporate cost control, and the non-recurrence of FY26’s bad debt provision and store impairment. As is typical for GOOS, ~75% of annual revenue and effectively all of the company’s profit are generated in the back half of the year, pointing to modest H1 margin pressure followed by H2 expansion.

Earnings Call Highlights

General Market

The CNN “Fear and Greed Index” ticked up to 44 this week from 30 last week. You can learn how this indicator is calculated and how it works here: (Video Explanation)

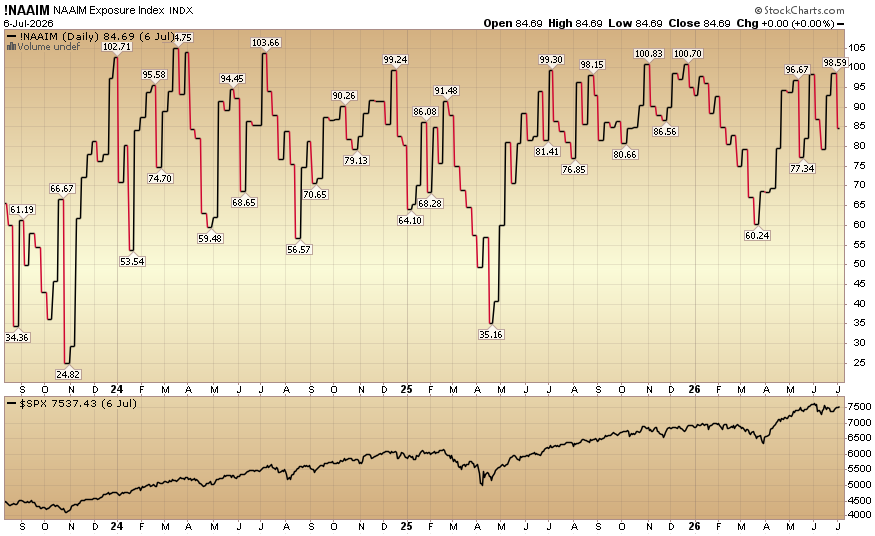

The NAAIM (National Association of Active Investment Managers Index) (Video Explanation) ticked down to 84.69% equity exposure this week from 98.59% last week.

Our podcast|videocast will be out sometime today. We have a lot of great data to cover this week. Each week, we have a segment called “Ask Me Anything (AMA)” where we answer questions sent in by our audience. If you have a question for this week’s episode, please send it in at the contact form here.

Comments

Log in or sign up to join the conversation.