Minutes of the Federal Open Market Committee

Please consider Minutes of the June 16–17, 2026 Federal Open Market Committee emphasis mine.

Staff Economic Outlook

The staff’s inflation forecast for this year and the next was higher than the one prepared for the April meeting, reflecting incoming data, higher energy prices and other input costs due to the conflict in the Middle East, and the effects of the AI buildout on consumer prices. Total inflation was projected to slow over the second half of this year from its recent pace, as retail gasoline prices were expected to decline, although core inflation was forecast to change little over the rest of the year. Inflation was projected to step down next year, as some of the factors lifting inflation this year—such as tariffs—were expected to wane, and then move down further to about 2 percent in 2028.

The staff’s outlook for real GDP growth was a bit lower than the one prepared for the previous meeting, mostly reflecting incoming data. Real GDP was forecast to expand at about the same pace as potential this year and to slightly outpace potential over the next two years, buttressed by persistently strong productivity growth, continued gains in AI-related capital spending, and supportive financial conditions. The unemployment rate was expected to remain close to the staff’s estimate of its longer-run rate this year and next before edging slightly below it in 2028.

The staff continued to view the uncertainty around their forecast as elevated, importantly because of uncertainty about the conflict in the Middle East and about the potential economic effects of AI investment and adoption. On balance, risks to the forecasts for employment and real GDP growth were seen as tilted somewhat to the downside. Risks to the inflation projection were seen as more skewed to the upside. With inflation having run significantly above 2 percent over the past five years and in light of some emergent price pressures that appeared unrelated to tariffs or energy prices, the staff continued to view the possibility that inflation would be more persistent than projected as a salient risk.

Participants’ Views on Current Conditions and the Economic Outlook

Participants generally noted that inflation had increased further and remained well above the Committee’s 2 percent longer-run objective. They observed that both core and total inflation had moved higher and generally attributed these increases to the lingering effects of tariffs, supply chain disruptions related to the closure of the Strait of Hormuz, and strength in demand for some goods and services stemming from robust AI-related investment. Several participants commented that price pressures had become more broad based, with a large share of goods and services—including transportation, airfares, petrochemical products, and agricultural inputs—experiencing substantial increases. Several participants remarked that services price inflation excluding housing had declined little and remained high.

Participants anticipated that inflation would remain elevated in the near term and then begin to decline as the effects of tariffs and energy price increases wane and other supply disruptions related to the closure of the Strait of Hormuz diminish. Participants judged that the risks to the inflation outlook were still tilted to the upside. Many participants noted that elevated commodity prices and supply disruptions could persist longer than currently anticipated. Several participants reported that their business contacts were facing notable cost pressures. Some participants observed that the sharp rise in input costs reported in business surveys raised concerns about the potential for higher energy and commodity costs to pass through more broadly to final goods prices.

Participants generally expected solid real GDP growth to continue throughout the remainder of the year and pointed to several factors likely to support continued expansion, including ongoing AI-related investment, household spending, and fiscal policy. Participants generally acknowledged that while the economy had demonstrated resilience to date, uncertainty surrounding the economic outlook remained elevated, partly due to the conflict in the Middle East.

Regarding participants’ individual assessments of appropriate monetary policy under what each participant judged to be the most likely scenario for the economy, many participants indicated that the appropriate level of the federal funds rate would be within or slightly below the current target range at the end of this year. Many other participants, however, assessed that the appropriate level of the federal funds rate would be above the current target range at the end of this year. Participants noted that their future policy actions would depend on incoming information.

A number of participants noted that it was an opportune time to consider significant changes to the FOMC’s postmeeting statement. A majority of participants remarked that they saw advantages in shortening the statement. Most participants emphasized that they preferred not to repeat the language in the previous postmeeting statement that had suggested an easing bias regarding the likely direction of the Committee’s future interest rate decisions. Various participants discussed how the public could perceive the changes to the postmeeting statement. Some participants commented that they welcomed the opportunity to review the Committee’s communications tools and practices.

The Chairman described plans to establish five independent task forces to examine issues related to the broad conduct of monetary policy.

Warsh Is Stuck With Two Bosses

Fed Chair Kevin Warsh is stuck with two bosses.

Warsh’s first boss is Trump who wants lower rates. His second boss is inflation which has defied the Fed’s expectations.

Forward guidance and dot plots may go away. Warsh does not like either. But rather than do away with them, he set a task force to decide.

It is likely Warsh shortens FOMC statements starting with the July meeting.

Market Reaction

It’s difficult to ascertain what if any impact the minutes had on the market because the renewed fighting in Iran and Trump’s cancelling of the MOU set the tone for the day.

My guess is nearly all of the market reaction today in bonds is from the Mideast. However, Fed concerns over AI spending and persistent inflation didn’t help.

For the July meeting, rate hike odds are 30.5 percent, up from 26.7 percent yesterday.

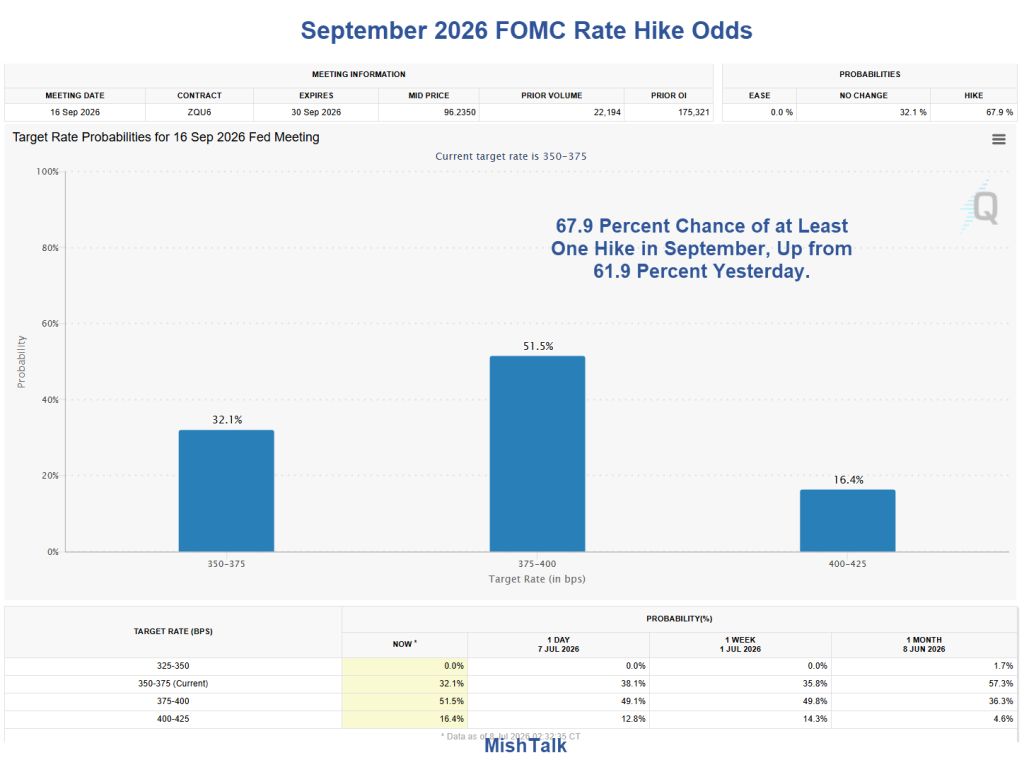

Looking ahead to September, the futures market sees a 67.9 percent chance of a at least one hike, up from 61.9 percent yesterday.

I highly doubt the Fed hikes at the October 28th meeting so close to the election.

The betting markets, however, forecast a 76.6 percent chance of at least one hike (up 4.8 percentage points from yesterday), with a 28.9 percent chance of at least two hikes.

The net expectation then is for a single quarter point hike by the end of October. If so, expect that hike in September, not July or October.

There is no meeting in August or these odds would look a lot different.

I will reserve rate hike judgement until we see how quickly (or not) Trump backs off fighting Iran. We also need to see the next CPI, PCE, and job reports.

Related Posts

July 8, 2026: Trump Warns Ceasefire with Iran Is Over, Calls Iran Scum, Oil Surges 8 Percent

I didn’t think Trump would be this foolish, but here we are.

July 7, 2026: Goods and Services Trade Deficit Expands 44 Percent to 77.6 Billion

Trump’s tariffs have done nothing to reduce the trade deficit.

July 6, 2026: Trump’s Tariffs Did Not Bring Back Manufacturing Jobs. What Will?

On average, tariffs are a jobs killer. They protect one industry while costing others.

Comments

Log in or sign up to join the conversation.