The Fed largely delivered on expectations with an emergency 50bp rate cut this Tuesday. The dollar was initially weaker across the board, with high yield FX performing strongly. However, a very uncertain equity environment means that volatility will stay high and it looks too early to be jumping back into carrying trade strategies.

US Fed Chairman, Jerome Powell, announcing a cut in US rates

Fed largely delivers in Round One

The Fed has acted reasonably quickly in cutting rates 50bp. As James Knightley writes, this may well be the first of perhaps a three-stage easing cycle that will ultimately be worth 100bp. The DXY had already fallen 2.5% over recent days and today we did not see that much follow-through selling of dollar against the EUR and the JPY.

The larger dollar selling in the G10 space came against the activity currencies of AUD and SEK on the view that reflationary Fed policy (steeper yield curves) would kick start an economic recovery. That view looks premature, however. It is very unclear how far Covid-19 will spread and its impact on activity – proving both a supply and demand shock.

And like most financial products, the FX market is wary that the Fed’s medicine will only provide temporary relief to global equity markets. Our team is very cautious on risk assets and believe the Fed will be called again into action over coming quarters. We see EUR/$ moving to 1.15 and $/JPY to 105 over the coming months, with volatility staying high.

Too early to re-enter the carry trade

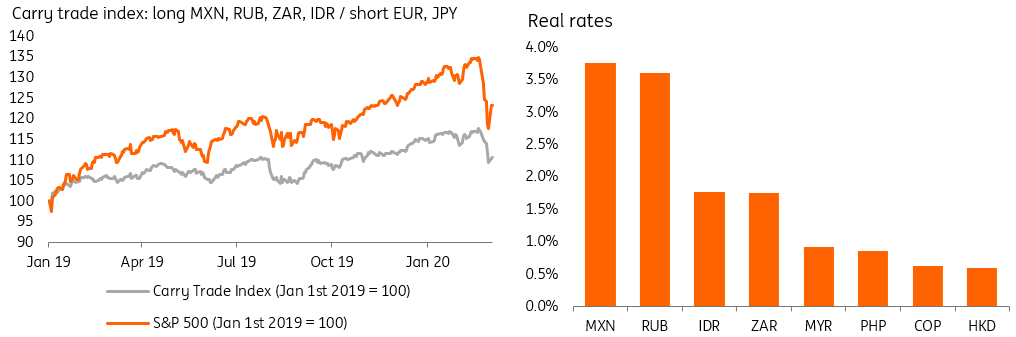

The bigger FX moves on today’s Fed cut came in the high yield EM space. The Mexican peso, the darling of the EM high yield world, briefly enjoyed a 2% rally against the dollar, with other high yielders, such as RUB and ZAR, following suit. As we highlighted last week, these are the currencies with the highest real rates in the EM universe and have been very popular with carry trade strategies.

However, the carry trade is a low volatility strategy designed to pick up yield (and hopefully some nominal FX appreciation) in a benign market environment. As we highlight below, the pick-up in volatility emerging from the equity market has triggered huge draw-downs in carry trade strategies (we look at a basket equally invested in MXN, RUB, ZAR and IDR, funded equally out of EUR and JPY).

Unless one believes that policymakers with their actions so far have put a floor under risk assets and volatility drops substantially – (highly unlikely in our opinion) – it looks premature to be buying the dip in high yield FX.

Carry trade and real rates

(Click on image to enlarge)

Source: Bloomberg, ING

Comments

Log in or sign up to join the conversation.