A recent article by the Wall Street Journal entitled Turbocharged Earnings Are Pushing Stocks Higher. There’s a Catch raises an important issue for investors of the megacap AI-tech companies. Wall Street analysts expect S&P 500 earnings growth to top 20% for a second consecutive quarter; however, the earnings growth is not widespread. The predominant bulk of the earnings growth is being driven by semiconductor makers and AI infrastructure companies. Todd Castagno, a Morgan Stanley analyst, questions how long some tech companies can continue to grow earnings at such historical rates. To wit, he deems the current period of growth as “a golden window where everybody looks good.” The reason for his pessimism is how hyperscalers account for expenses.

When Nvidia sells a chip, it books revenue immediately. But the hyperscalers buying those chips (Meta, Microsoft, Alphabet, Amazon, and Oracle) treat the expenses as capital assets, allowing them to spread the cost over years as depreciation. On an aggregated basis, the revenue hits as earnings today, but the expenses are limited. For context, the five major hyperscalers spent $412 billion in capital expenditures in 2025, with estimates for 2026 reaching $760 billion. Depreciation expenses for 2026 are estimated at only $211 billion. The $549 billion gap will ultimately be accounted for.

The bottom line is that there are significant, growing expenses that will hit hyperscalers’ income statements in the future. Can revenue expand quickly enough to offset the coming bulge in expenses? Answering the question is tricky, making it difficult to predict margins for 2028 and beyond. Per the article:

And, as Zion Research Group founder David Zion says, “analyst depreciation estimates for each of these companies are all over the place.” He says that the “consensus D&A (depreciation and amortization) estimates could be systematically understated.”

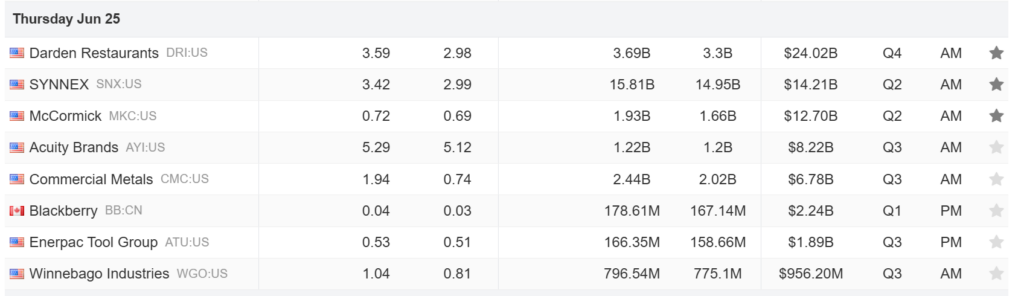

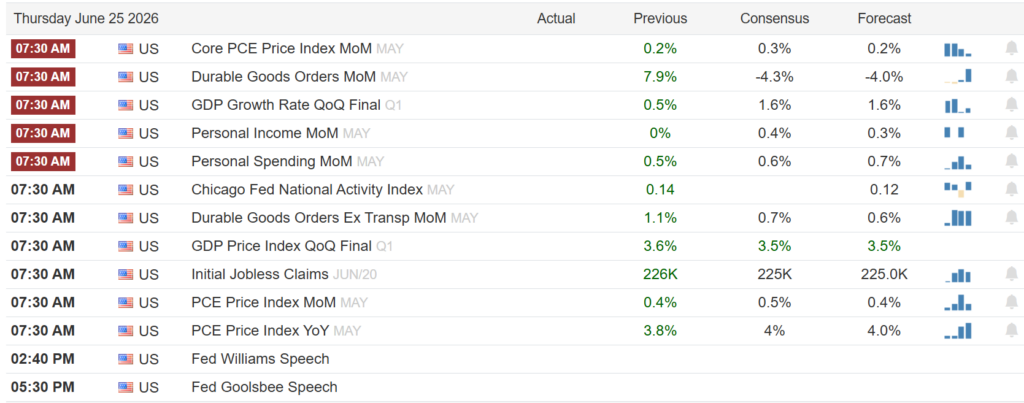

What To Watch Today

Earnings

Economy

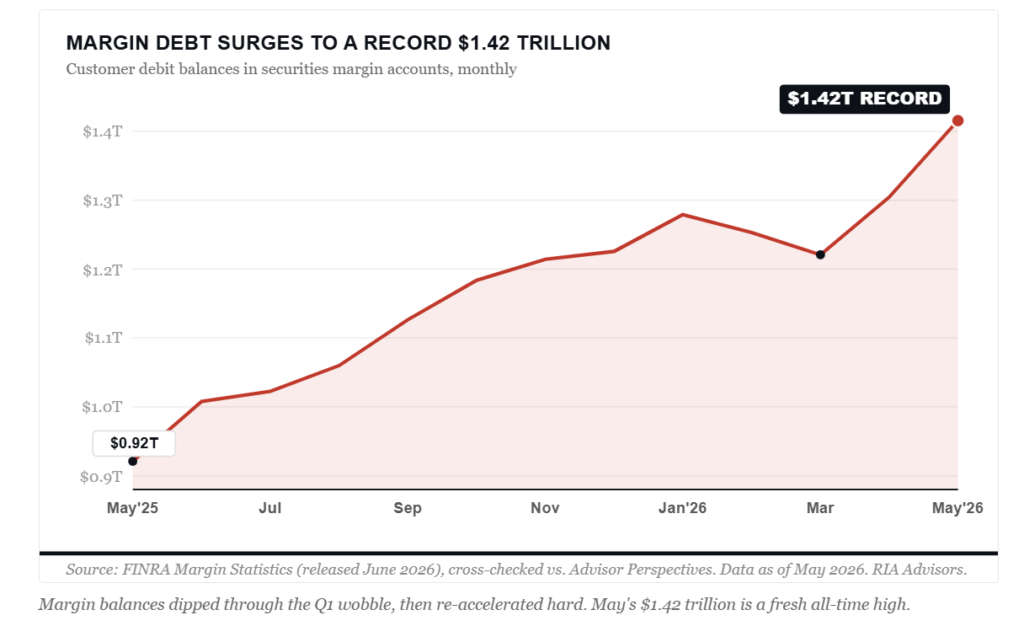

Market Trading Update

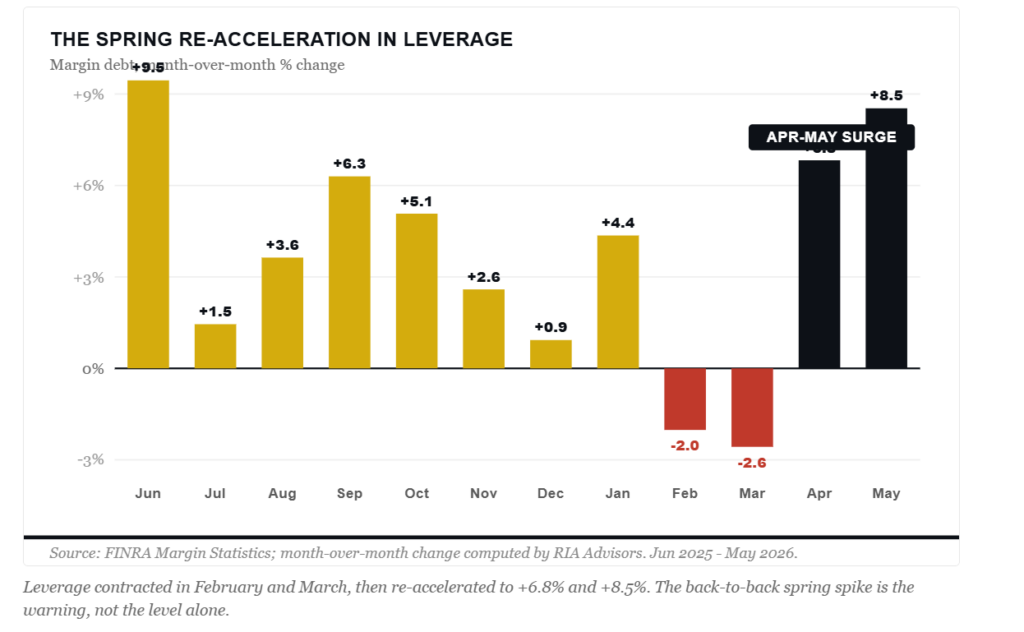

Yesterday, we discussed the semiconductor sector and the current bullish bias. Speaking of bullishness, margin debt is another sign of bullishness that continues to support the market.

Margin debt just went vertical. FINRA released the May data, and customer margin balances jumped to a record $1.42 trillion, an 8.5% surge in a single month and the second straight monthly increase. That’s $111 billion of fresh borrowed money chasing stocks in thirty days. Year over year, margin debt is up 53.7%, the steepest annual expansion outside the 2021 blowoff and the 2000 peak.

Make no mistake, this is the “gasoline” we’ve written about repeatedly. Rising leverage fuels bull markets on the way up, because borrowed dollars buy more shares, prices climb, borrowing capacity expands, and the cycle feeds itself. It’s a feedback loop, and right now it’s running hot. As we covered in Margin Debt Sets Records, extreme leverage relative to market cap or GDP has preceded every major bear market over the past 70 years.

Here’s where it gets interesting. The Q1 pullback actually drained margin balances for two months, from January into March. Then the spring rally landed, and leverage came roaring back, up 6.8% in April and 8.5% in May. That two-month sprint off the March low, nearly 16%, is the part that should grab your attention. Callum Thomas at Topdown Charts ranks the current rate of expansion as the fourth fastest on record, a reading that has historically shown up a few months ahead of major tops.

The cash side tells the same story. Net of free credit balances, investors owe a record $992 billion more than they hold in cash, the deepest negative reading on record. Margin debt against GDP now sits at 4.45%, nearly 47% above its long-term average. Investors aren’t just leveraged. They’re leveraged with almost no dry powder behind it, a fragility we flagged in Margin Balances Suggest Risks Are Building.

Margin debt is not a timing tool. It’s the kindling. The match is whatever finally turns the tape.

The bottom line is what we always remind subscribers. Margin debt won’t tell you when to sell. As Howard Marks put it, “fear of missing out has taken over from the fear of losing money,” and that condition can run far longer than it should. The previous three topping signals on this indicator each took several months to resolve. So this isn’t a sell-everything alarm.

But it is a setup. The trouble with leverage is that the unwind isn’t at the investor’s discretion. When the tape turns, broker-dealers force the selling, margin calls cluster, and forced liquidation begets more forced liquidation. We walked through that exact mechanism in Speculative Narrative Unwinds. For now, we’re watching breadth and the rate of change closely. Stay invested, but tighten your risk discipline. The kindling is stacked.

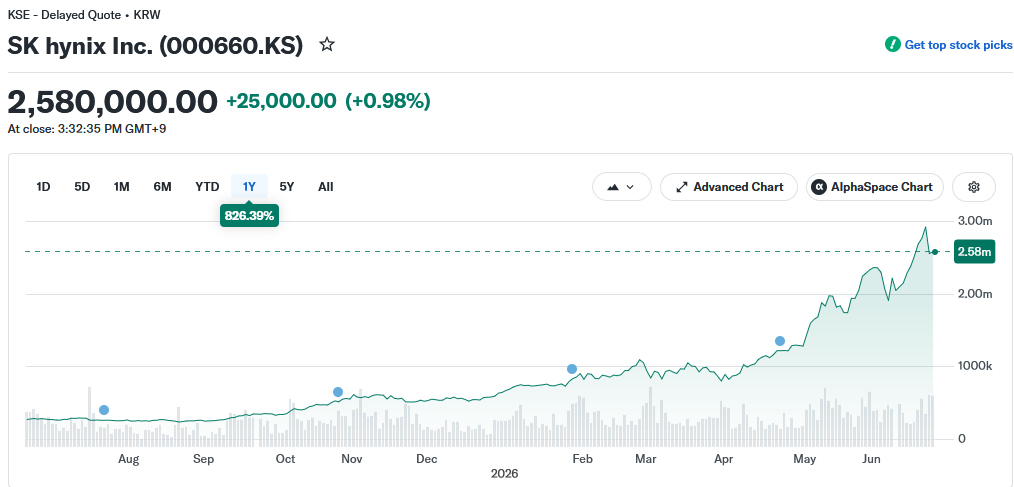

SK Hynix Adds To The Equity Supply Surge

On Tuesday night, Korean memory chip maker SK Hynix announced plans for a $29.4 billion US listing. This would be the biggest American Depositary Receipt offering in history, surpassing Alibaba’s $25 billion 2014 debut. The offering is expected to begin trading on July 10.

We have written several commentaries and articles on the coming surge in equity issuance. In The IPO Boom, we liken the new issuance to adding marbles to a jar. To wit:

Think of the stock market as a jar full of marbles. For the new SpaceX and other marbles to fit in the jar, either the jar must be enlarged, or some of the other marbles must shrink.

Given the current monetary environment, the jar, or available capital, is unlikely to grow significantly. The Fed is no longer providing the flood of liquidity that enabled the easy digestion of the SPAC boom in 2020 and 2021. Rates are higher, savings rates are lower, and the equity market is already trading at elevated valuations. Simply put, there isn’t much extra liquidity. Thus, the other option is for the collective market cap of everything else to decline.

In reality, there will be some shrinkage of marbles and an enlargement of the jar. The extent of both will help determine how the IPO boom is received and its impact on other stocks.

The newest marble, so to speak, arrives weeks after the SpaceX IPO and against a pipeline of IPOs, Anthropic, and OpenAI, as well as secondary offerings from many of the large hyperscalers.

SK Hynix’s strategic logic is straightforward. SK Hynix trades at a meaningful discount to Micron, despite being the dominant supplier of high-bandwidth memory chips that power Nvidia’s AI GPU stacks. A US listing gives the company access to a deeper, more liquid investor base. Taiwan Semiconductors did a similar offering, and its US ADR trades at a persistent premium to its Taiwan-listed shares.

As shown below, SK Hynix shares have already surged 300% in 2026 and more than 800% over the last full year, driven by strong HBM demand. The US listing gives American investors a direct path into that trade but adds more supply to a growing wave of supply.

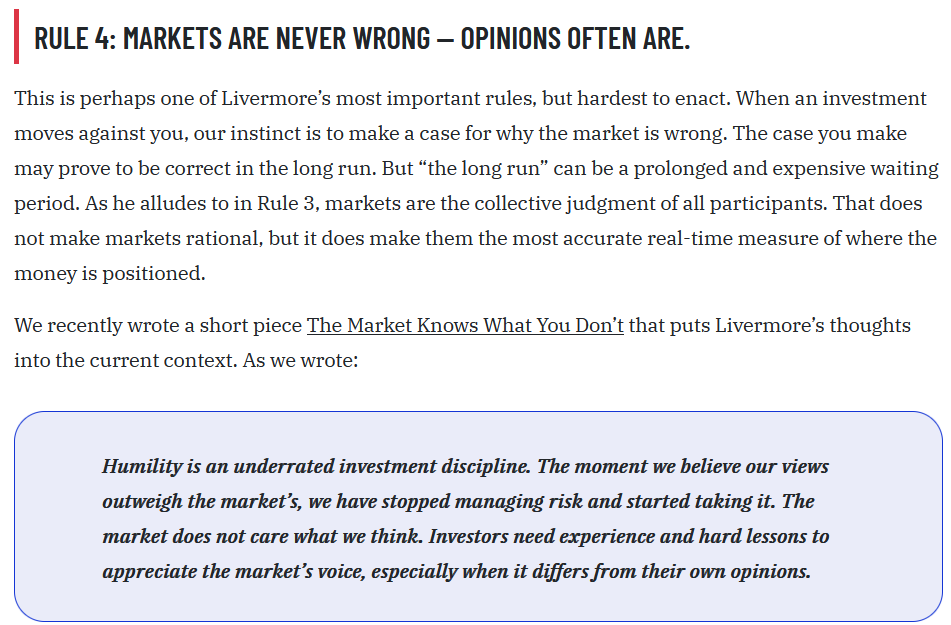

Jesse Livermore: Old Lessons For Today’s Markets

The prolific trading stories about Jesse Livermore and the fortunes he made and lost are well documented in two books. The first, Reminiscences of a Stock Operator (1923), authored by Edwin Lefèvre, is the better-known of the two. The second book, How to Trade in Stocks (1940), was written by Livermore himself. It conveys the many lessons of what four decades of speculation had taught him. Specifically, he presents 21 market rules. While his career was marked by the incredible volatility of his wealth, and some consider him a failure as he died broke, his market knowledge is invaluable. Accordingly, we share his 21 market rules. While the language he uses is outdated, the rules remain prescient.

Tweet of the Day

Comments

Log in or sign up to join the conversation.