Image Source: Unsplash

"The market can remain irrational longer than you can remain solvent"

Attributed to John Maynard Keynes.

For this to hold true one must be in the market, usually on the short side when the market is clearly running ahead of its Dividend Discount Value (DDV). One can remain solvent by being out of the market and in either cash, near cash or even gold awaiting the return of sanity.

This was true in 1987, the second half of the 1990s through the 2000s and since Trump was re-elected in November in 2024.and the 30-year T-bond moved above 4.5%. Each period has been an example of irrational exuberance and extremely so today.

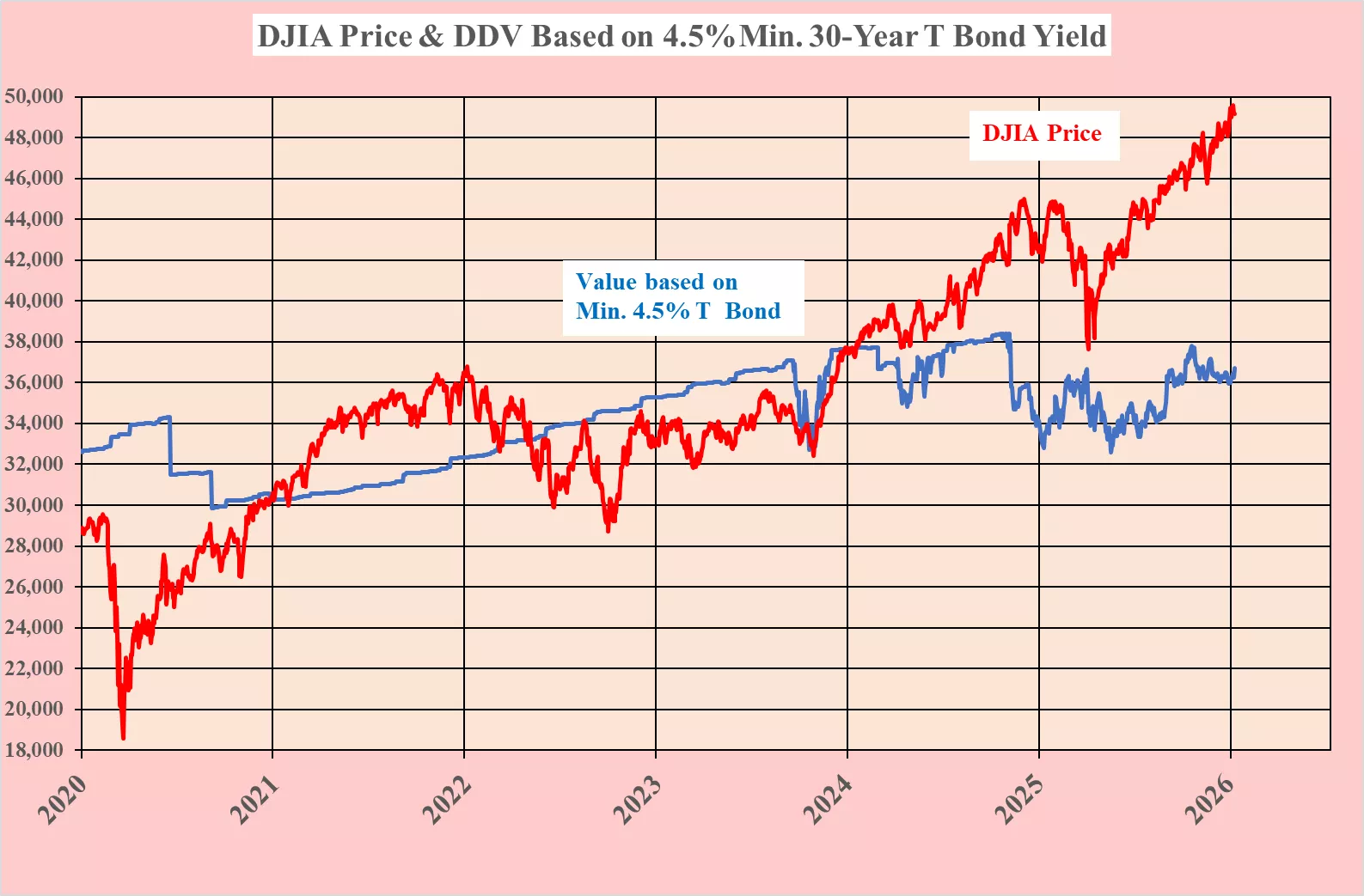

So far this year the DJIA has been at a record premium to its DDV. On Jan 12 the DJIA closed at a record 49,590. This was at a 13,234 point, or 36%, premium to its DDV. This almost as great as the 14,899-point discount to its DDV the DJIA closed at on March 23, 2020 when COVID 19 caused a sell-off of the DJIA.

Any rise in the long bond without an offsetting rise in the DJIA dividend will only increase the premium of the DJIA to its DDV making the DJIA even more expensive than ever.

At a 30-year T-bond yield of 5% the premium would rise to 41% and beyond, as shown in the following table.

The next chart shows the difference between the DJIA and its DDV compared to the actual price since 1981. The blue line shows the daily calculated DDV of the DJIA, and the red line its daily price since the end of the Great Bear market in bonds on September 29, 1981, when the 30-year T bond hit 15.2%.

The causal correlation between the daily price and DDV of the DJIA at 0.964 is phenomenally high over such a long period. From this, there is a high probability that the two lines should soon merge.

Such an outcome could stem from either the DJIA’s DVD rising or its price falling, or both. The next two charts are the same as above, but on linear scales and from two different starting points, the pre-Lehman peak and the start of COVID-19.

Most of the heavy lifting of the DDV in both shorter-term charts is attributable to the increase in the DJIA dividend, as the 30-year T-bond yield has been below 4.5%. It is only over the past 15 months that the 30-year T-bond yield has had any impact on the DDV, and that has been negative as it has risen above 4.5%. Keeping the DDV below 39,022.

Looking to the future

This paper has used only historical daily data. No forecasts have been used to calculate the DVD. With high probability of the relationship continuing between the DJIA value and price it should revert to equilibrium.

The payout ratio of the DJIA is 40%, well below the 45-year historical average of 57% so it is unlikely that weakness in the DDV will stem from a falling dividend. It seems much more likely that long-term bond rates will rise with the ever-mounting US Government debt at $38.6 trillion along with Trump’s military shenanigans et al. adding billions to the budget deficit.

Perhaps we are about to see a repeat of the rising inflation and long-term rates of the period from 1965 to 1981. This seems increasingly likely as Donald Trump wants to rid himself of an independent FED and have much lower short-term rates as did Richard Nixon in 1972.

History may not repeat itself, but it does seem to rhyme and while the above may be true there are even more salutary lessons to be learned from an excellent book that my wife gave me for Christmas. Entitled “1929” by Andrew Ross Sorkin in which there are many similarities to the madness of today including the gambling dens of the 1920s bucket shops and the gambling going on today in the form of Prediction Markets for Trading the Future of the outcomes of events such as sports, elections, stock prices and commodities. Even more addictive is the out and out gambling on Bitcoin which has a price but no obvious value.

A must read for every student or practitioner of finance or economics.

More By This Author:

DJIA At 29% Premium To Its DDV. Caveat Emptor.

DJIA - Bears Are Roaring

DJIA Price Exceeds Its Value By Historical Record - Sell

Comments

Log in or sign up to join the conversation.