Rising inflation has finally pushed the yield of the US 30-year T-bond above 5%. This has pushed the Dividend Discount Value (DDV) of the DJIA (DIA) to the point where it is the most expensive ever recorded. A sizeable correction is long overdue. For the price of the DJIA to be in equilibrium with its DDV, it would need to fall by 42% or more, with further probable increases in the long bond rate.

The Present

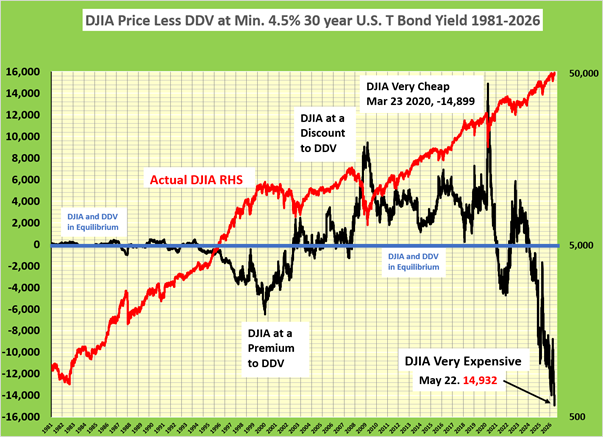

On May 22, 2026, the price of DJIA closed at a record 50,580, which pushed it to a record premium of 14,991, to its Dividend Discount Value (DDV) of 35,648. This 42% premium is greater than was the record discount of 14,899 attained on March 23, 2000. at the nadir of COVID-19 despair.

Any rise in the long bond without an offsetting rise in the DJIA dividend will only increase the premium of the DJIA to its DDV, making the DJIA even more expensive than ever. Alternatively, the price of the DJIA could drop to reduce the premium to its value.

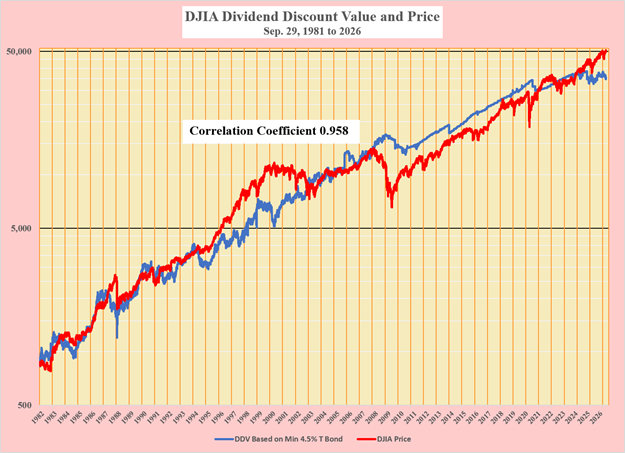

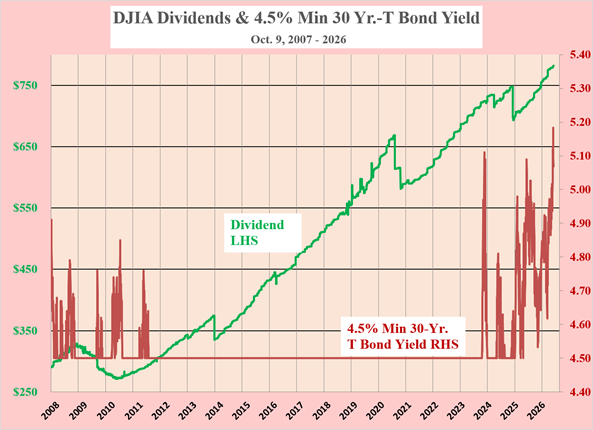

The next chart shows the difference between the DJIA and its DDV compared to the actual price since 1981. The blue line shows the daily calculated DDV of the DJIA, and the red line its daily price since the end of the Great Bear market in bonds on September 29, 1981, when the 30-year T bond hit 15.2%.

The causal correlation between the daily price and DDV of the DJIA at 0.958 is phenomenally high over such a long period. From this, there is a high probability that the two lines should soon merge.

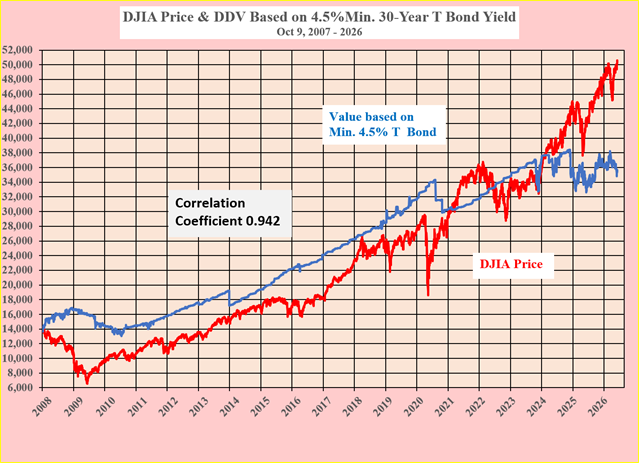

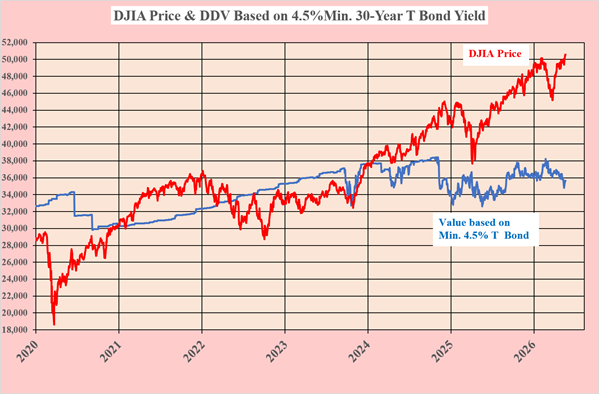

Such an outcome could stem from either the DJIA’s DVD rising or its price falling, or both. The next two charts are the same as above, but on linear scales and from two different starting points, the pre-Lehman peak and the start of COVID-19.

Most of the heavy lifting of the DDV in both shorter-term charts is attributable to the increase in the DJIA dividend, as the 30-year T-bond yield has been below 4.5%. It is only over the past 18 months that the 30-year T-bond yield has had any impact on the DDV, and that has been negative as it rose above 4.5%. Keeping the DDV below 38,413 since Trump was elected on November 4, 2024.

Looking to the future

So far, this paper has used only historical daily data. No forecasts have been used to calculate the DVD and to compare it with the DJIA. With high probability of the relationship continuing, the value and price should revert to equilibrium.

The payout ratio of the DJIA is 40%, well below the 47-year historical average of 56%, so it is unlikely that weakness in the DDV will stem from a falling dividend. It seems much more likely that long-term bond rates will rise with the ever-mounting US Government debt at $39.2 trillion, along with Trump’s shenanigans, both with the war in the Middle East and domestically with his construction of monuments to his own self-aggrandizement.

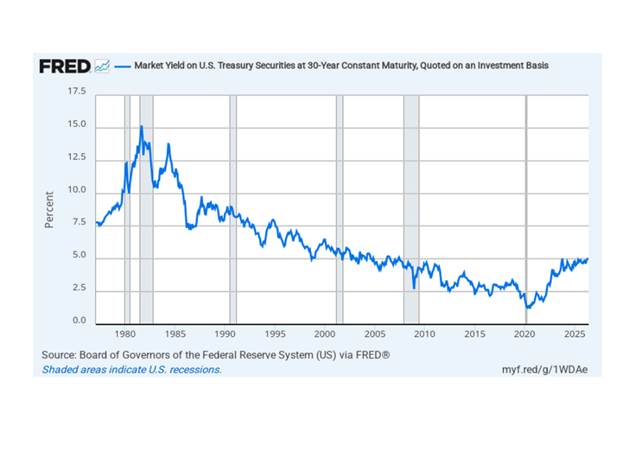

Perhaps we are about to see a repeat of the rising inflation and long-term rates of the period from 1965 to 1981, which was followed by the four-decade bull market in bonds that ended on March 9, 2020. The 30-year t-bond closed at 1.0% following an intra-day low of 0.5%. Since then, rates have been on the rise and now exceed 5%.

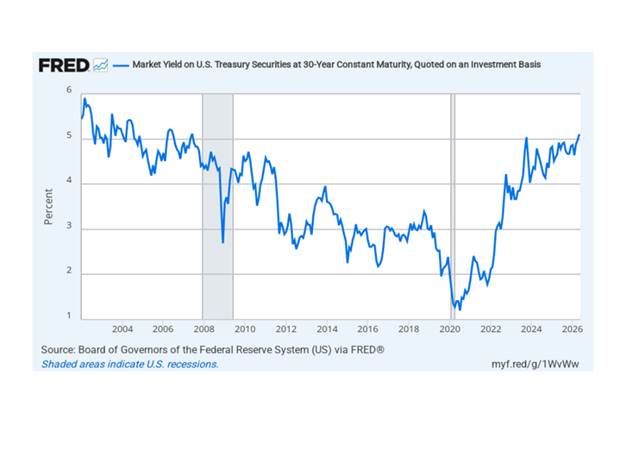

In the next chart, the 30-year T bond yield moved up to the 5% level in October 2023 when Janet Yellen, as the Secretary of the Treasury, decided to move from refunding expiring long-term bonds with much lower rates in shorter maturity notes at lower rates. A practice copied by her successor, Scott Bessent, whenever the 30-year T-bond approached 5%. It would also appear that this is the reason why Trump has wanted the FED to lower the Fed Funds rate ever since he returned to the White House.

However, with the recent surge of inflation, we are close to the end of that game, and if the recent PPI measure of 6% is any harbinger of what is to come for the CPI, we could well be on our way to a repeat of the 1965 to 1981 bear market in bonds. With the National Debt already at $39.2 trillion, this spells disaster.

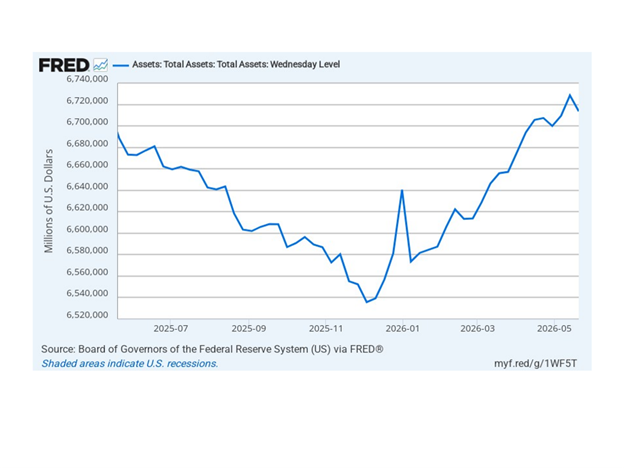

The FED seems to recognize this with what seems to be the beginning of a new round of Quantitative Easing

It looks as though Stephen Miran’s plan to shrink the FED’s balance sheet has been defenestrated along with his departure from the FED.

History may not repeat itself, but it does seem to rhyme and while the above may be true there are even more salutary lessons to be learned from 1929 with its many similarities to the madness of today including the gambling dens of the 1920s bucket shops and the gambling going on today in the form of Prediction Markets for Trading the Future of the outcomes of events such as sports, elections, stock prices, wars, oil and other commodities. Even more addictive is the out-and-out gambling on Bitcoin, which has a price but no obvious value.

Stock market performance seems to be concentrated in an ever-diminishing pool of names. In particular, the AI companies seem to be driven higher solely by “momentum”. It strikes me that there are an awful lot of people chasing things they know very little about. This suggests very strongly that it is time to offload.

But what about the likes of Nvidia (NVDA)? The Company has performed spectacularly. However, superb growth and fantastic margins should have the same effect as high prices, which are their own best cure. Competition is already being attracted from around the world and should continue until substitution brings prices and margins down. Thus, stocks that are discounting the status quo ad infinitum are also priced to perfection and should be sold.

The pending SpaceX IPO

The only person to benefit from this hype is Elon Musk. I wonder if this will be the pin that bursts the bubble.

Comments

Log in or sign up to join the conversation.