Phone and computer internet network by Pinkypills via iStock

Palo Alto Networks (PANW) stock has been on a tear. Based on its strong free cash flow and FCF margins, as well as analysts' forecasts, PANW stock could be worth 21% more at over $403 per share. This article will show how this works.

PANW closed up over 9.1% at $332.00 on Monday, June 29. The stock has been on an upward trajectory since its June 2 earnings release for the fiscal Q3 ended April 30, after a brief initial drop.

PANW stock - last 3 months - Barchart - June 29, 2026

What PANW Could Be Worth

Based on my new assessment of Palo Alto Networks' fair market value (FMV) it could be worth between $303 billion and $354 billion. This is between 12.1% and 30.7% higher. That sets its price target 21% higher on average, despite its recent up, or $403 per share.

I discussed its valuation in a recent Barchart article on June 8, “Palo Alto Networks Delivers Strong FCF Margins - Is PANW Worth $350?”

My latest FMV analysis builds on that article.

For example, analysts now project revenue for the next FY ending June 30, 2027, will be $13.78 billion. Applying a 38.5% FCF margin, slightly higher than my prior estimate, but equal to its latest fiscal Q3 trailing 12 months (TTM) adjusted FCF margin:

$13.78 billion x 0.385 adj. FCF margin = $5.305 billion FCF

Moreover, using a 1.75% FCF yield metric, Palo Alto Networks would have a fair market value (FMV) of $303 billion:

$5.305b / 0.0175 = $303 billion FMV

And, using a lower 1.50% FCF yield metric, it's worth more:

$5.305b / 0.015 = $353.7 billion FMV

In other words, based on today's market cap of $270.6 billion, PANW's price target (PT) is worth between 12% and 31% more, or:

$332.00 x 1.12 = $371.84 per share PT

$332.00 x 1.307 = $433.92 per share PT

The average price target is therefore 21.4% higher, or $402.88 per share. That rounds out to $403 per share.

However, there's no guarantee that PANW will rise to this PT. It could take some time. As a result, it might make sense to set a lower buy-in point and get paid for it. That can be done by selling short out-of-the-money PANW put options.

Shorting Out-of-the-Money PANW Puts

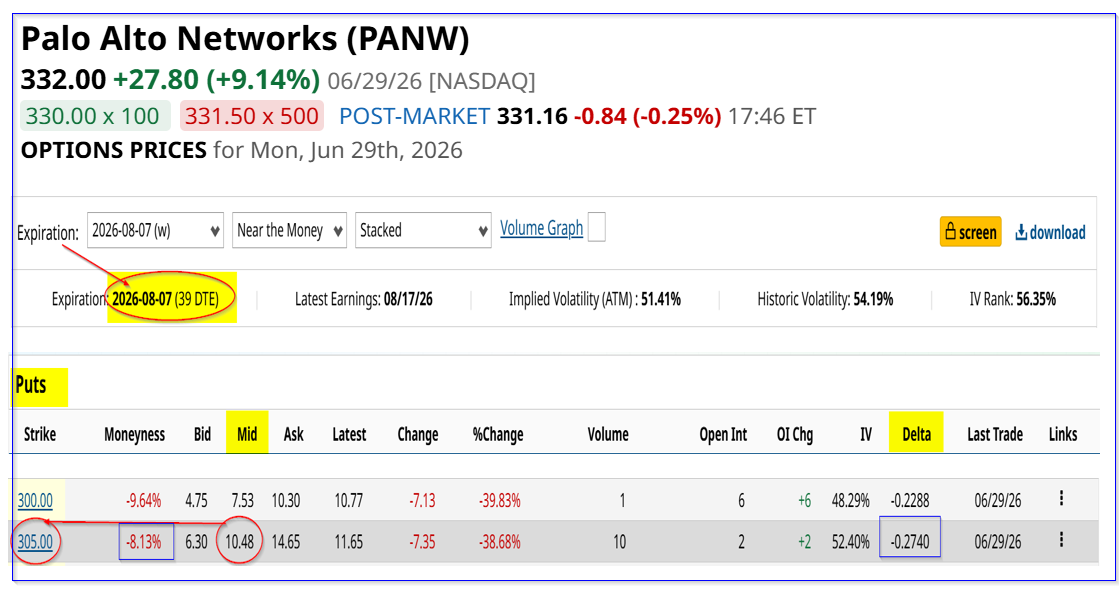

For example, the August 7, 2026, expiry put option chain shows that the $305.00 strike price put option has a high midpoint premium of $10.48.

That means that a short-seller of this put contract can make an immediate yield of 3.436% over the next 39 days (i.e., $10.48/$305.00 = 0.03436 = 3.436%).

PANW puts expiring Aug. 7 - Barchart - As of June 29, 2026

Here is how this works. First, the investor posts $30,500 with the brokerage firm where their account is located. That acts as collateral to buy 100 shares at $305.00, if PANW falls over 8% from $332 to $305 on or before Aug. 7.

Then, the investor can enter a trading order to “Sell to Open” 1 put contract at $305.00. The investor's account will then immediately receive $1,048 (i.e., $10.48 x 100 shs per put contract).

So, the $1,048 received lowers the initial cost to just $29,452. That works out to a net put contract cost of $294.52, or 11.3% lower. That lowers the overall potential buy-in cost for investors.

Moreover, investors can take comfort in the delta ratio, which is low at just -0.274. That implies there is just over a 27% chance that PANW will drop 8% to $305 by Aug. 7.

The bottom line is that this is an attractive way for PANW value investors to get paid while also setting a lower potential buy-in point.

Comments

Log in or sign up to join the conversation.