One of the hardest distinctions for investors is separating a crowded trade from a bubble. A bubble typically rests on fantasy: minimal earnings, no durable cash flows, and little path to justify lofty prices. Dot.com names in the late 1990s and housing valuations in the 2000s were recent examples of bubbles. A crowded trade is different. It centers on real businesses with genuine profits, demand, and growth. The risk isn’t a fabricated story—it’s too much capital chasing the same narrative simultaneously, driving prices beyond what even robust fundamentals support.

Parts of the semiconductor and memory sector appear to fit this description today. Micron (MU), SanDisk, and Western Digital (WDC) are established players, not speculative shells. They appear to be riding a genuine boom in AI infrastructure, high-bandwidth memory (HBM), enterprise SSDs, data center storage, and supply constraints. Margins have expanded, cash flows have strengthened, and pricing power has returned. This is far from 1999-style vaporware.

But crowded trades can still become overvalued. The warning sign: when investors shift from “What is this worth?” to “How high can it go?” That mindset can transform strong businesses into risky stocks.

The DCF Framework

The basic discounted cash flow (DCF) model remains the foundation for valuation:

Intrinsic Value ≈ Future Free Cash Flow / (Discount Rate − Long-Term Growth Rate)

Using the simplified Gordon Growth version: Value = FCF × (1 + g) / (r − g)

Where:

FCF = normalized free cash flow

g = long-term growth rate

r = discount rate

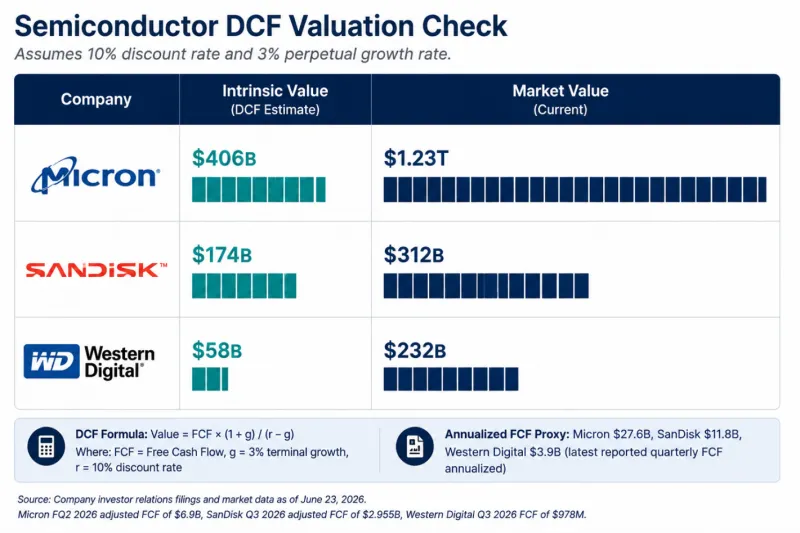

For cyclical semiconductor and memory companies, a higher discount rate is warranted due to cash flow volatility. In my opinion, a 10% discount rate and 3% terminal growth rate are defensible starting points, implying a roughly 14.7x multiple on normalized FCF. For higher-quality compounders, a lower rate (e.g., 8%) and slightly higher growth (e.g., 5%) yield multiples around 34x.

A 10% discount rate and 3% terminal growth rate are reasonable starting assumptions because they attempt to balance two competing realities. On one hand, companies such as Micron, SanDisk, and Western Digital are participating in a very real AI- and data-center-driven boom, with stronger demand, improved pricing, and much higher cash generation than the market saw during prior downcycles. On the other hand, they remain cyclical memory and storage businesses whose cash flows can swing sharply as supply responses emerge, pricing normalizes, or hyperscaler spending slows. A 10% discount rate reflects that volatility and the risk that today’s elevated margins and free cash flow may not represent steady-state earnings power.

Likewise, a 3% terminal growth rate is not meant to capture the current boom; it is meant to reflect a mature, long-run growth rate more in line with nominal economic growth once the industry moves beyond the present shortage cycle. In other words, the purpose of these assumptions is not to deny the strength of the current cycle, but to avoid capitalizing peak conditions as if they will persist indefinitely.

The Semiconductor Trade: Real Growth, Stretched Valuation

Here are rough intrinsic value estimates using annualized cash flow based on recent free cash flow quarterly results:

Illustration created with AI using ChatGPT.

These are valuation observations about the stocks, not bearish calls on the underlying businesses. Micron benefits centrally from AI memory demand. SanDisk’s flash and enterprise storage are seeing explosive growth from AI infrastructure buyers. Western Digital is gaining from stronger pricing, improved margins, and storage demand. Fundamentals are currently solid.

The concern is that markets are capitalizing peak-cycle cash flows as if they were permanent—a risky proposition in a historically cyclical industry. Memory and storage markets have long cycled between shortages and oversupply. Tight supply drives rapid margin expansion and soaring earnings, but new capacity or cooling demand tends to reverse that leverage.

Higher interest rates may amplify the issue. Elevated rates discount future cash flows more heavily: a business worth 25x FCF at a 7% discount rate might command only 15x at 10%. This dynamic hits hardest for stocks where today’s prices embed distant, optimistic cash flows. Crowded trades can thus become fragile—the fundamental AI story can remain valid even as multiples compress.

The Boom Is Real, But Expectations Are Lofty

The bullish case for semiconductors is compelling. Demand for AI accelerators, high-bandwidth memory, enterprise SSDs, networking, and data center capacity continues to outstrip supply in key segments. Industry forecasts point to persistent shortages and capacity constraints through much of 2026, supporting elevated pricing and profitability for Micron, SanDisk, and Western Digital. Hyperscalers consistently report AI infrastructure as supply-constrained.

This differs markedly from classic tech bubbles. Unlike the dot-com era, today’s leaders generate substantial earnings, free cash flow, and returns on capital. The challenge isn’t demand—it’s whether prices have already discounted years of outsized success.

A key driver is unprecedented hyperscaler spending. The four majors (Amazon (AMZN), Microsoft (MSFT), Alphabet (GOOGL), Meta (META)) spent roughly $410 billion on capex in 2025. Projections for 2026 range from $650–$725 billion or higher—a 60–80%+ jump in a single year. Goldman Sachs has raised its cumulative estimate for these hyperscalers from 2025–2030 to ~$5.3 trillion (from $4.5 trillion previously), with 2026 spending nearing or exceeding $757 billion in some scenarios and potentially surpassing $900 billion by 2027 according to their June article, “Private Markets Are Expected to Have a Growing Role in Data Center Financing.”

Individual guides are striking: Amazon ~$200B, Microsoft $120–190B, Alphabet $175–190B, Meta $125–145B. Combined, these four could outspend the entire U.S. energy sector’s annual infrastructure investment.

These figures explain the crowding into memory and semiconductor suppliers. Sustained spending would underpin strong demand for chips, memory, storage, and related infrastructure well into the future.

Yet significant uncertainty remains around the ultimate return on investment. Markets are assuming that today's extraordinary AI spending will eventually generate sufficient revenues and profits to justify the capital being deployed, but the economics are still largely unproven. Many AI services continue to be subsidized, pricing pressure is emerging in certain areas, and competition among model providers remains intense. Investors can easily measure how much capital is being spent; what remains far less certain is the long-term monetization of those investments. History shows that bubbles often form when markets begin extrapolating current growth and spending trends indefinitely into the future. While the AI opportunity is real, assuming today's pace of hyperscaler capital expenditures can continue indefinitely—and earn attractive returns indefinitely—is a leap of faith that has yet to be fully validated.

Bridgewater Associates has warned that the AI investment cycle has entered a “more dangerous phase,” with infrastructure spending accelerating faster than revenue generation. Goldman Sachs has highlighted how capex is increasingly consuming operating cash flow and displacing share repurchases. Prediction markets and some institutions are pricing in risks of moderated hyperscaler spending, custom chip development, or cost-cutting that could pressure suppliers.

Bears have voiced similar concerns for over a year—yet demand has repeatedly exceeded expectations, spending forecasts have risen, and earnings estimates have climbed. The debate persists: bulls emphasize accelerating demand and constraints; bears question ultimate returns on this scale of investment. The resolution will distinguish temporary valuation excess from a durable transformation.

Oil, Inflation, and the Rate Problem

The macro environment is critical, as inflation and rates directly influence discount rates. Easing in the Strait of Hormuz or lower oil prices could relieve inflationary pressure, boost sentiment, and give the Fed room to maneuver.

However, oil inventories remain exceptionally tight. According to Reuters, citing U.S. Energy Information Administration data, total U.S. crude inventories—including both commercial stocks and the Strategic Petroleum Reserve—fell to 758.5 million barrels in mid-June, the lowest level since March 1985. While hopes of a reopening of the Strait of Hormuz have fueled expectations for lower oil prices and easing inflation, the underlying supply picture remains far less comfortable.

With inventories already near four-decade lows, the market has little margin for error should another supply disruption emerge. That leaves inflation vulnerable to renewed energy shocks and raises the possibility that interest rates remain elevated as Chairman Warsh last week implied a greater concern over current inflation rates. For crowded growth trades whose valuations depend heavily on future cash flows, higher discount rates remain a significant risk that may not be fully appreciated by investors.

The Less Crowded Opportunity: Mega-Cap Compounders

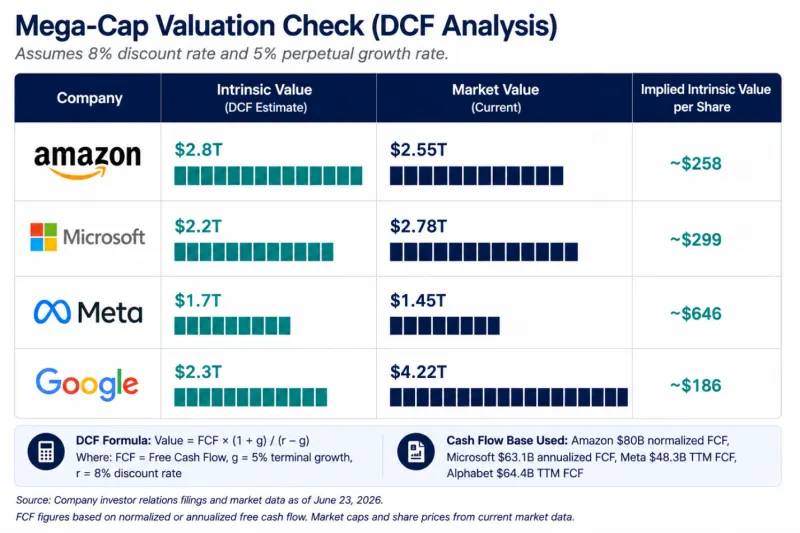

A relative opportunity may lie in the mega-cap platforms—Amazon, Microsoft, Meta, and Alphabet. They are heavy AI spenders too, but benefit from diversified models, strong balance sheets, recurring revenues, dominant moats, and multiple cash flow engines.

Illustration created with AI using ChatGPT.

This framework suggests that several of the mega-cap technology companies may be more attractively valued than many of today's crowded semiconductor trades. Meta appears particularly compelling on a pure DCF basis, while Amazon's valuation may look more attractive. Microsoft may be one of the highest-quality compounders in the market, though its current valuation already reflects significant future success. Alphabet presents a more nuanced case: it remains an exceptional business, but its current market capitalization implies either substantially higher future cash flows, a lower discount rate, or a longer period of elevated growth than our base assumptions.

Ironically, the recent selloff in some mega-cap technology names has been driven largely by concerns over their aggressive AI spending plans. Investors have questioned whether hundreds of billions of dollars in capital expenditures will ultimately generate adequate returns. Yet those same concerns may have created valuation opportunities. While much of the market has crowded into semiconductor and infrastructure suppliers, several large hedge funds appear to be increasing exposure to the platform companies that ultimately monetize AI.

According to first-quarter 13F filings, Bridgewater Associates’ largest reported additions included Amazon, Taiwan Semiconductor (TSM), Micron, Broadcom (AVGO), and Nvidia (NVDA). WhaleWisdom’s tracking of the filings shows that Bill Ackman’s Pershing Square Capital Management initiated a roughly $2.09 billion Microsoft position in the quarter and added approximately $384 million to its reported Amazon holdings. Berkshire Hathaway significantly increased its reported Alphabet stake in the first quarter, adding roughly 36.4 million shares of Alphabet Class A stock, bringing the position to about $15.6 billion at quarter-end. David Tepper’s Appaloosa Management also made notable additions during the quarter, including approximately $446 million of Amazon and $285 million of Micron. All figures are based on reported 13F holdings as tracked by WhaleWisdom and related 13F portfolio summaries.

To be fair, not all institutional investors share this view. Several hedge funds have reduced exposure to AI-related investments due to concerns that valuations have become stretched, AI infrastructure spending may not generate sufficient returns, and current hyperscaler capital expenditure projections could prove overly optimistic. These concerns are legitimate and deserve consideration. However, variations of the same bearish argument have been circulating since early 2025. During that time, hyperscalers have repeatedly increased spending plans, AI demand has continued to exceed expectations, and earnings estimates across much of the semiconductor ecosystem have moved steadily higher. For now, neither side has decisively won the debate. The bulls point to accelerating demand and supply constraints, while the bears question whether the industry's extraordinary spending levels can ultimately earn an adequate return. The answer will likely determine whether today's crowded semiconductor trade represents a temporary valuation excess or the early stages of a longer-term technological transformation.

Bottom Line

Crowded trades and bubbles are not the same thing. The semiconductor trade is crowded, but it is backed by real earnings and real AI-driven demand. That makes it stronger than a classic bubble, but not immune to valuation risk.

The biggest risk is not that Micron, SanDisk, or Western Digital are bad companies. The risk is that investors are paying peak-cycle prices for cyclical cash flows at a time when higher rates make future cash flows worth less.

Meanwhile, some mega-cap technology stocks may offer a better balance between durability, profitability, and valuation discipline. The opportunity is not simply in buying what is growing the fastest. It is in buying growth where the cash flows, discount rate, and valuation still make sense.

In a market full of crowded trades, valuation is not a timing tool. But it is a risk-management tool.

Comments

Log in or sign up to join the conversation.