Conoco Phillips (COP) HQ Sign - by MattGush via iStock

Short-sellers of out-of-the-money (OTM) ConocoPhillips (COP) put options expiring in one month can make 1% or more. COP stock has fluctuated with oil prices as the war in Iran has waned. Investors can play this by shorting OTM COP puts.

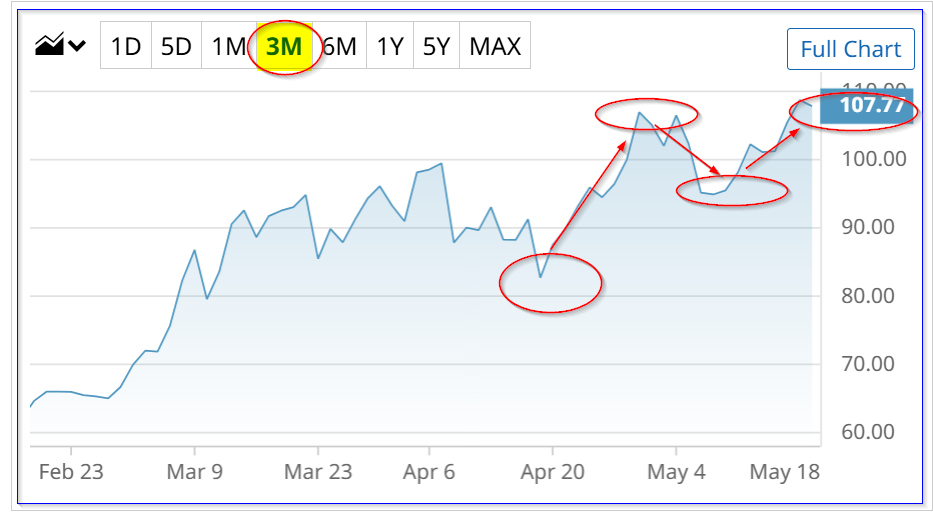

COP closed at $116.98 on Friday, June 12, up about 1.4%. But, it's still down from a peak about a month ago on May 19, when it closed at $125.11. However, its low has been only $113.98 on May 29 in the last 3 months since the Iran war started.

COP stock - last 3 months - Barchart - June 12, 2026

This is similar to what has happened with the ups and downs in the June 2026 WTI crude oil (CLM) futures price, as shown in the Barchart chart below. It shows that CLM dipped at the beginning of May as COP did, but has risen since then, with a dip recently.

June 26 WTI Crude Oil (CLM) - Barchart - June 12, 2026

This may have led to higher-than-normal put option prices, as investors expect another dip in oil prices. I discussed this in a Barchart article a month ago: “ConocoPhillips Put Options Look Attractive to Short Sellers as Oil Rises” (May 18, 2026).

Shorting 1-Month Cash-Secured Puts

In the article, I pointed out that the $115.00 put option expiring June 18 had a midpoint premium of $1.92. That strike price was 6% below the trading price on May 18, $122.41 (i.e., “out-of-the-money”).

That provided a short-seller with a cash-secured yield of 1.667% (i.e., $1.92/$115.00). As of Friday, June 12, the price has floated down to $1.14. However, it's still out of the money, albeit only slightly. That's because COP is at $116.98, so the $115.00 exercise price is just $2.00 lower (i.e., 1.69% OTM).

As a result, it may make sense for the investor to roll this play over to the next month.

Rolling the Play Over to the Next Month

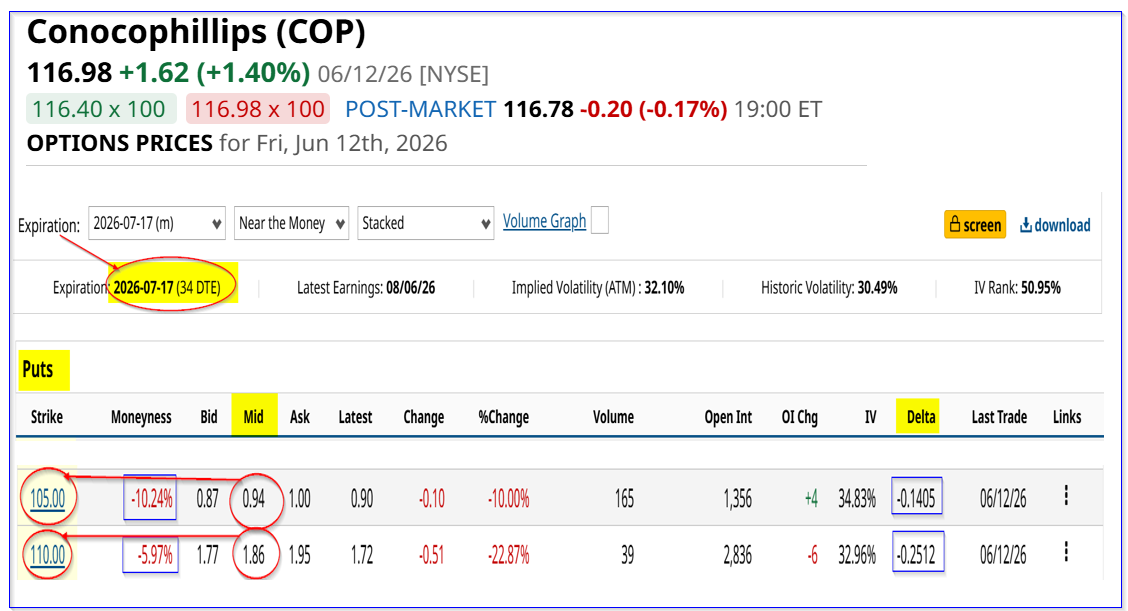

For example, the July 17 expiry $105.00 put option, over 10% below Friday's close, still has a midpoint premium of 94 cents. That still provides an attractive yield play of about 90 basis points: $0.94/$105.00 = 0.00895 = 0.895%

COP puts expiring July 17 - Barchart - June 12, 2026

Moreover, after rolling the play over (i.e., paying $1.14 to close the June short-put play), the investor would have a net debit of 20 cents (i.e., $0.94-$1.14) per put shorted (i.e., -$20 per contract).

However, given that the investor made $1.92 in the original play, the net credit is $1.92-$0.20, or $1.72 for the two months. That works out to a 2-month yield of:

$1.72/ ($115 + $105)/2 = $1.72/$110 = 1.56% for 2 months

As a result, it makes sense to short the $110.00 July 17 put contract, which has a midpoint premium of $1.86. A rollover still provides a net credit of:

$1.86 / $110 = 0.0169 = 1.69% for 1 month

And, after deducting the rollover cost of $1.14, the net credit would be $0.72. Therefore, the two-month yield is:

$0.72 + $1.92 = $2.64 two month income

$2.62 / ($115 +$110)/2 = $2.62 / $112.50 = 0.0233 = 2.33% over 2 months

Summary and Conclusion

The bottom line is that this is an attractive way to play COP. For example, if this play is repeated every 2 months, the annualized expected return is

2.33% x 6 = 13.98%, almost 14%

That is a very attractive way for value investors to play COP over the long run. It provides a great return along with a potentially lower buy-in point for value investors.

Comments

Log in or sign up to join the conversation.