Walking on Sunshine

The market has pivoted from walking on eggshells to walking on sunshine, and that shift in tone is everything. What began as a cautious overnight drift, with oil probing higher on lingering doubts around Strait of Hormuz access, flipped decisively once the US session came online. De-escalation headlines out of Washington, Jerusalem, and Beirut did not just calm nerves; they rewired positioning. Oil lost altitude from above $100, equities caught a bid that refused to let go, and suddenly the tape was no longer trading fear of disruption but hope, even if “North Sea Brent” says nope. The S&P extended into its longest winning streak in six months, not because the risks disappeared, but because the market judged that the clock had been pushed back again.

At the centre of it all sits the same fulcrum that has defined this entire 2-month-long episode. Hormuz is not just a waterway; it is Iran’s negotiating leverage, cast in sedimentary rock and salt domes. As long as talks are ongoing, the equation is clear, Iran’s leverage is Hormuz, and the question is whether they are prepared to give it up. That tension remains, embedded in the physical market, where prompt barrels remain tight and the underlying system has not meaningfully loosened. But markets are not trading the current state of play; they are trading the trajectory, and right now that trajectory bends towards de-escalation.

What is striking is how cleanly price has completed the roundtrip. The entire drawdown has been erased, volatility has collapsed back into its box, and the positioning reset has done its work. This is no longer a fragile market being held together by hope. It is a market being carried by flows. Systematic buyers are re-engaging, with CTAs flipping back to long and expected to add further size into strength. The mechanical bid is back in the system, and that matters more than any single headline because it feeds on itself. When flows turn, they do not tiptoe; they compound.

Overlay that with a subtle but important shift in the macro backdrop. The latest run of US data has taken some of the sting out of stagflation fears. Inflation signals are easing at the margin, while growth indicators are firming, nudging central bank expectations toward a more dovish stance. That combination is oxygen for risk. Bonds are bid not out of panic but out of recalibration, gold is catching a parallel flow as a portfolio stabilizer rather than a crisis hedge, and even bitcoin (BTC.X) is riding the same liquidity tide. The dollar, which never fully owned this crisis despite the scale of the oil shock, is now softening as rate expectations adjust.

Underneath the surface, the market’s internal wiring has also changed. Earlier this year, rallies repeatedly stalled against a wall of dealer long gamma, a structural ceiling that dampened momentum. That ceiling has now flipped. Dealer positioning has rotated such that upside moves are no longer suppressed but amplified, while downside moves are more likely to be absorbed. In effect, the market has installed an upside accelerator and a downside shock absorber. It is an upside-down stabilizer, and in this configuration, strength begets strength.

None of this resolves the core uncertainty. The durability of any ceasefire, the credibility of negotiations, and the true reopening of the Strait of Hormuz remain the anchors that will ultimately decide whether this is a bridge to something lasting or just another well-timed pause. But for now, the market is not waiting for certainty. It is trading the probability distribution, and that distribution has shifted just enough to let risk breathe again.

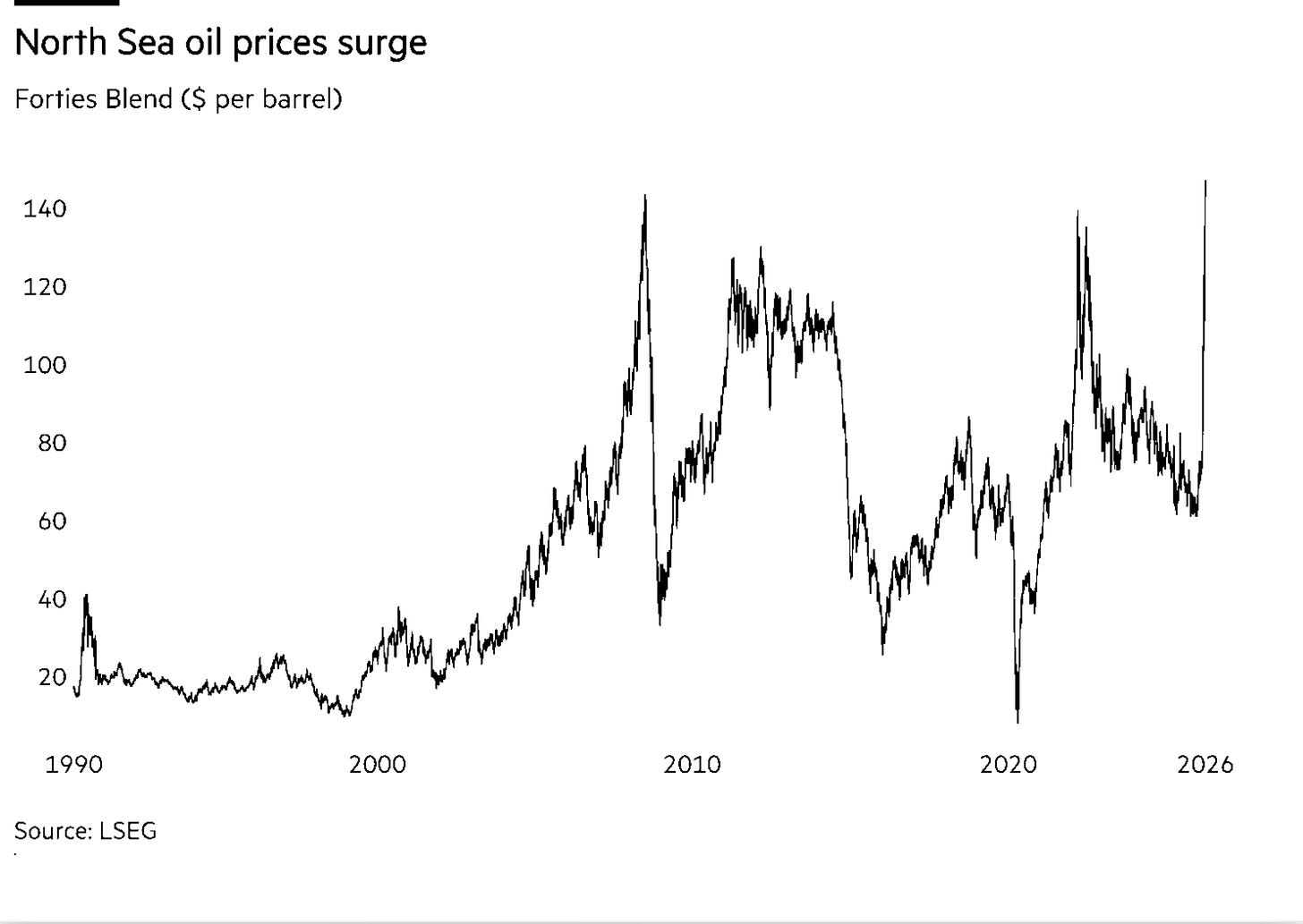

Physical Oil Screams Scarcity While Paper Still Whispers Calm

The market is no longer trading oil as a commodity. It is trading oil as access. And right now, access is broken.

North Sea barrels have become the last lifeboats in a system where the main shipping lane is still effectively under lock and key. Forties Blend surging toward $147 is not just a price spike, it is a distress signal from the physical market, a flare shot into the sky to tell you that immediate supply is no longer a given. While futures hover near $97, trying to anchor expectations to a world that may soon reappear, the prompt market is screaming that the world we trade today has already changed.

This is what true dislocation looks like. The paper market trades belief. The physical market trades reality. And right now, reality is bidding aggressively for anything that can be loaded, shipped, and delivered without asking permission from the Strait of Hormuz.

The breakdown is no longer subtle. When Brent contracts for difference blow out beyond $30 and liquidity disappears from the exchange itself, the plumbing of the market is no longer functioning as designed. Hedging tools vanish, price discovery fractures, and deals migrate into the shadows. That is not volatility. That is stress migrating through the system.

And the source of that stress is not theoretical. The Strait of Hormuz is not closed on paper, but it is constrained in practice. Only a trickle of ships is moving, many tied directly to Iran, while the rest of the world waits for clearance that may or may not come. Control has shifted from open water to controlled passage, from free flow to conditional access. The market is now pricing not just disruption, but the precedent that disruption can be monetized.

Asia sits closest to the fault line. With roughly 80 percent of its energy flows tied to Hormuz, the region is effectively trading energy on a conditional basis. Every refinery bid in Europe and Asia is a reflection of that fear, a scramble to secure molecules before the clock runs out. Because once the market decides the Strait is functionally closed, even if not officially declared, price no longer rises in increments. It gaps.

What makes this more dangerous is that supply elsewhere is not stepping in cleanly. Saudi disruptions have quietly removed capacity at the exact moment the system needs redundancy. The East-West pipeline, designed as a geopolitical bypass, is now partially offline. That is the equivalent of losing your emergency exit while the fire alarm is still ringing.

And this is why the futures market feels detached. Futures are trading on the assumption that time heals. That ships will eventually move, that logistics will normalize, that diplomacy will catch up with disruption. But the physical market is trading the cost of waiting. Even if the Strait reopens tomorrow, it takes weeks for flows to normalize, inventories to rebuild, and confidence to return. The clock does not reset instantly. It grinds forward through logistical lag.

So what you are seeing is not a contradiction. It is sequencing. The physical market moves first. The futures market catches up later.

The ceasefire was supposed to calm the system. Instead, it has exposed the fault lines. Because a ceasefire without flow is not resolution. It is simply a pause with conditions attached. And in markets, conditional access is just another form of scarcity.

The barrel is no longer just pricing inflation. It is pricing control. And until control over Hormuz returns to something resembling normality, the physical market will continue to trade like a system under siege, no matter how calm the futures curve tries to look

Comments

Log in or sign up to join the conversation.