Favorable risk-reward options set up revolving around the PDUFA date

Fortress's balance sheet of $381 million and runway until the end of 2027 lowers the downside risk

NS Pharma Partnership to pay $80 mil in a milestone payment upon approval and up to $1.4 billion for development and sales-based milestones for the U.S. & Japan and the EMEA

Exosomal platform technology, StealthX, is grossly undervalued given its potential as a delivery vehicle with targeting capabilities

Accommodative regulatory climate & Positive top line readout in both primary and secondary endpoints increase deramiocel's likelihood of approval

Bullish Investment Thesis - Capricor Therapeutics (CAPR) top-line readout has de-risked the stock heading into its PDUFA date of August 22, 2026. Their fortress balance sheet, the supportive regulatory climate, and high probability of approval from both analysts and advocacy groups have created a bullish backdrop for selling put options ahead of the FDA approval date.

CAPR option contracts have high implied volatility (IV) around the FDA PDUFA date. The timing of the option expiration in relation to the PDUFA announcement creates a favorable put premium selling strategy that yields a good return without bearing the risk of the FDA decision. The FDA’s new commissioner is all about greater flexibility when considering regulatory approval timing. Deramiocel fits their criteria for an expedited decision. The upside bias of this highly anticipated readout and underlying fundamentals reduces the risk of a losing trade if the price remains stable or rises.

Limited Treatment for Duchenne Muscular Dystrophy

Duchenne Muscular Dystrophy (DMD) is a rare genetic disease that affects about 15,000 patients in the United States and primarily amongst young men. It's a muscle-wasting condition that eventually impacts the heart and respiratory muscles due to the body's lack of the protein called dystrophin. The body needs this protein to maintain muscle stability. Without it, the cells become damaged and die, which eventually accumulates and leads to muscle fibers breaking down. The heart is predominantly affected by this lack of protein production, leading to cardiac issues, a poor quality of life, and eventually death for the patients.

Existing Treatments Fall Short

Sarepta Therapeutics. Inc. (SRPT) gene therapy is called Elevidys. It, along with steroids, represents the standard of care (SOC) for patients with Duchenne Muscular Dystrophy (DMD). This one-time therapy costs a patient $3.2 million. After a couple of deaths, Elevidys was given a black box warning for liver injury and failure. Although Elevidys is an approved drug, it failed to meet its trial endpoints, which means it is just a stopgap measure that helps the patients maintain motor function. Other approaches employ exon-skipping therapies, which help the body create shortened but functional proteins. These therapies require intravenous infusion.

Deramiocel Bridges the Treatment Gap

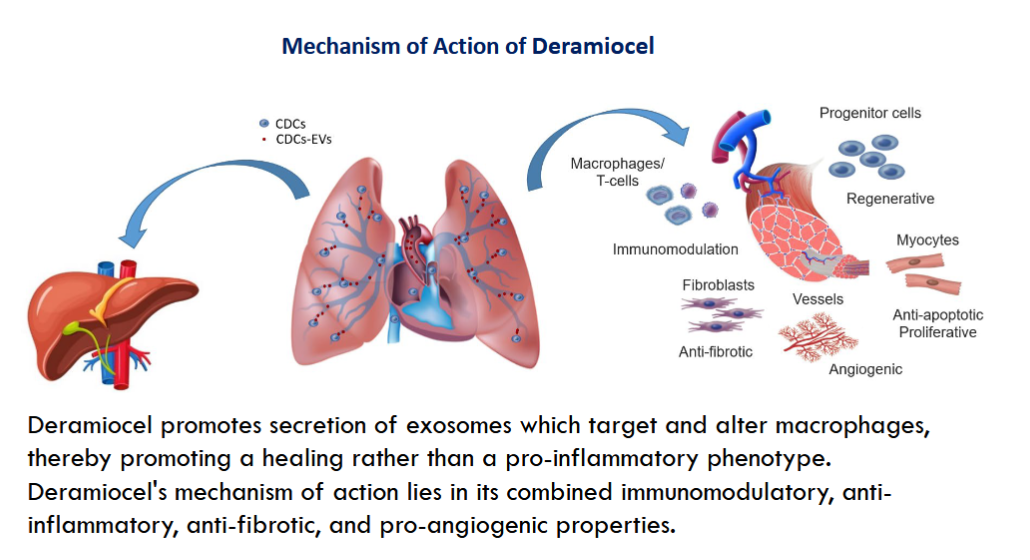

Deramiocel is CAPR’s leading target for patients with DMD. The most notable complication is the deterioration of the heart, leading to cardiac dysfunction. Deramiocel was designed to bridge this gap by providing the cardiosphere-derived cells (CDCs), which are basically circulating heart cells. After administration, the CDCs lodge in the lungs and start secreting exosomes along with growth factors that stimulate tissue repair and reduce inflammation. These exosomes make their way into the circulatory system via the capillaries in the lungs. From the lungs, they travel throughout the body as a drug delivery vehicle, but end up accumulating in the heart, where it's needed the most to combat the inflammation. The outer membrane of the exosomes resembles heart tissue, so it makes sense that the heart readily accepts these exosomes.

Source: Capricor

Platform Technology - StealthX Grossly Undervalued

Almost 47.8% of all drug sales are biologics (including monoclonal antibodies - Mabs) and about 52.2% are small molecules. All the other types of drugs are in the rounding error5% and that is where exosomes currently sit as a drug class. Exosomes are very versatile because they have virtually no limits on what they can target compared to monoclonal antibodies, and they can carry bigger and more delicate payloads that include nuclear material or even drugs. They can also be freeze-dried and stored for a long period without losing their potency. They are essentially a new class of biologics that are not prone to elicit an immune response unless programmed that way. StealthX is a vaccine technology designed to have the exosomes display antigens to stimulate the body's immune system. They are part of the project NexGen, which is focused on creating a vaccine for a virus that doesn't exist yet.

Exosomes are tiny (30 - 100 nm) sacs of a cell that can be modified to exhibit certain cellular receptors and loaded with drugs or biological cargo. They are essentially a targeted drug delivery vehicle that is similar in function to monoclonal antibodies. A key journal article shows the potential of exosomes as a delivery vehicle. These exosomes were targeted with a brain-homing peptide and, with near surgical precision, were able to cross the blood-brain barrier and ultimately deliver a silencing gene to Glioblastoma Cancer Stem cells. The dramatic in vitro results showed a near eradication of glioblastoma stem cells using the exosomes combined with chemotherapy.

While this is not Capricor’s immediate focus, it demonstrates the enormous potential of using exosomal targeting to deliver therapy without impacting the immune system the way monoclonal antibodies do. Capricor has its hands on a platform technology that can essentially target different tissue types versus just one or two receptors, the way monoclonal antibodies do. Capricor’s platform drug delivery vehicle is grossly undervalued, given the potential to more effectively target drugs and deliver payloads to their targets with greater safety.

Positive Tectonic Regulatory Shift

The new FDA Commissioner Marty Makary really came out swinging on how the FDA is going to do things differently. In a January interview, he boasted about 42 FDA reforms in the 10 months that he had been at the helm. The one that most applies to CAPR is that cell and gene therapies will not be held to the high GMP standards of drug manufacturing. The manufacturing requirements will be “customized to the drug and the population being treated.” Then he also talked about the plausible mechanism pathway that combines the science of determining the Mechanism of Action and common sense to an approval pathway.

These were not hallowed words because on February 27, he tweeted about a lung cancer drug approved in 44 days after filing. This was followed by a multiple myeloma drug approval 55 days after filing on March 5th. Then two weeks later, he summed it up with another approval record video tweeted on March 16th. Drugs showing promise to change patient outcomes were receiving quick approval without regard to filing deadlines.

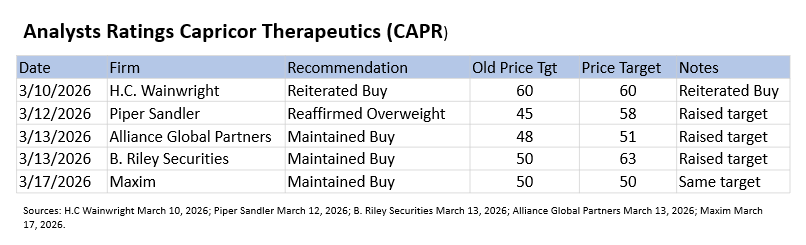

Analyst Sentiment - Raising Price Targets

There are 10 firms covering CAPR. In March, a number of firms raised their ratings. H.C Wainwright indicated deramiocel represented a transformational step following last year’s regulatory uncertainty. B.Riley (RILY) mentioned that the new data reinforced their conviction in a smooth path to potential Deramiocel approval at the August 22 PDUFA. Maxim commented that the probability of approval favors Capricor this August. There is a strong consensus that deramiocel will get FDA approval.

Why Early Release

Patient advocacy is at a very high level for Capricor. The Parent Project Muscular Dystrophy is an advocacy group that has been around since 1994. Over the span of the organization, they have invested $55 million into research and, most importantly, leveraged $850 million of federal funding. The result of their efforts was a 10-year increase in the lifespan of DMD patients. The website maintains news updates on the DMD therapeutics and the relevant drug developers like RegenxBio (RGNX), PTC Therapeutics, Inc. (PTCT), Solid Biosciences (SLDB), and Dyne Therapeutics (DYN). The group also has a YouTube channel where they have done webinars with the drug companies, and the CAPR videos have been the most popular by over a 3:1 ratio. There are also very powerful patient videos choreographed to push the FDA toward approval. The video generated over 63K page views as Aiden Leffler told his story about efficacy.

Financial Analysis

Capricor is sitting on $318 million in cash and has enough runway to fund operations through 2027. In December 2025, they raised $161.9 million via a public offering, along with $75.1 million from an ATM offering at $28.88/share. This financing helped create the cash horde that gives them plenty of contingency options that cover them through their PDUFA date in August and beyond the commercial launch and the ramping up of their manufacturing facility in San Diego. Typically, the short narrative will look at the threat of dilution after approval, but their proactive fundraising has silenced the dilution narrative.

In 2025, they showed a net loss of $105 mil vs $40.5 in 2024. They burned $30.2 million in Q4, and that is in line with their guidance on the conference call of $25-$30 million.

They also have a partnership with Nippon Shinyaku (NS Pharma), which represents $10 million in non-dilutive funding from reaching a development milestone, but the bigger picture is the upside of the deal. According to the terms of their partnership, they would receive $80 million in a milestone payment and up to $705 million in additional payments from double-digit royalties on sales in the United States and Japan once they get their FDA approval. There is also a European component that drives up the potential milestone value to $1.5 billion. CAPR is also eligible for a Rare Pediatric Disease Priority Review Voucher (PRV) from the FDA. In January 2026, Jazz Pharmaceuticals (JAZZ) sold its shares to an unnamed buyer for $200 million.

Their current market cap is $1.74 billion, but this is discounting a portion of their expected approval. .

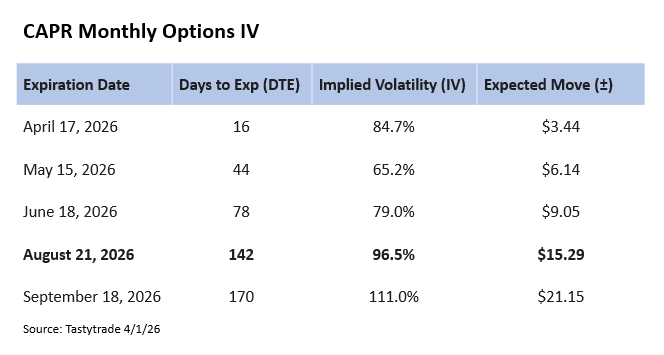

Option Setup - Selling Put Premium

Implied Volatility peaks in September, but the August expiration offers the best risk-to-reward ratio. The elegance of selling puts for the August 21 expiration is that it falls one day short of the official PDUFA date of August 22. It creates a window of opportunity that lets the investor harvest the full amount of the premium without taking the binary risk of the FDA approval decision. The strategy is ideal because the investor reaps a handsome reward before the PDUFA date. Should the decision come early, the odds are heavily skewed toward an approval, which would lift the stock and bode well for the strategy.

Another way to look at this is if the FDA decision drops before the PDUFA date, there’s a very good chance it will be positive based on historical precedent (> 90%). If a rejection is in the works, the FDA will drag things out, giving the sponsor every opportunity to correct any deficiencies that should arise. In summary, if deramiocel gets an early FDA nod, the stock will pop, and the short puts will expire worthless, allowing investors to pocket the premium. If there is no early announcement, investors will pocket the premiums earned over a number of months and be out of the position before the binary readout occurs, dramatically lowering the risk of failure.

The stock is currently in a tight holding pattern, and consolidation is likely into the readout. As the stock volume dries up, the option premiums will erode as well. This setup enables a sizable payout without having to face the volatility of an FDA approval announcement and the potential of a sell-the-news risk.

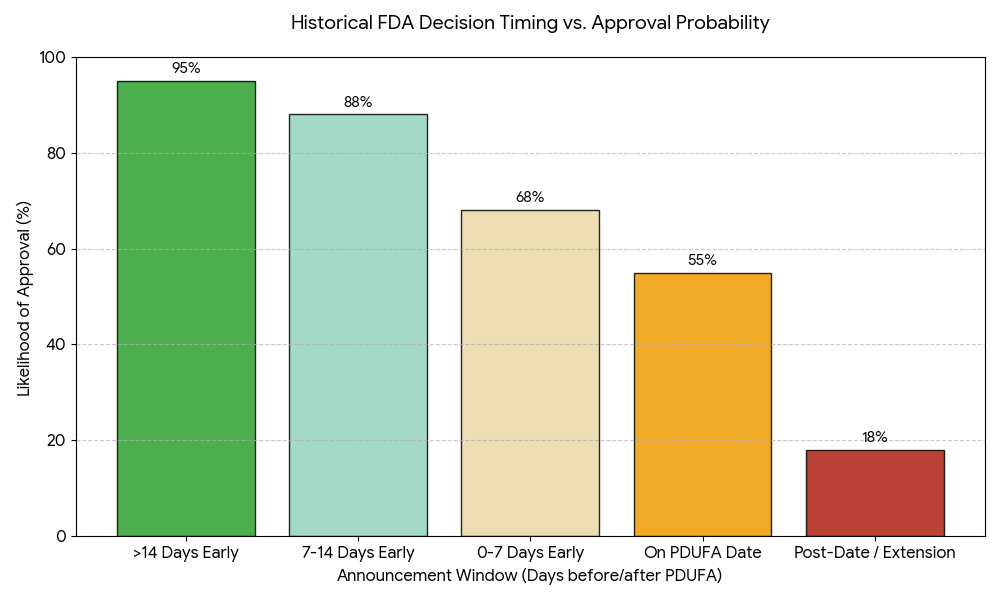

Early Decisions are Primarily Positive

Historical performance reports on FDA PDUFA decisions before the goal date show that greater than 90% of cases are reported before the goal date. According to the recent FDA annual reports, 47 out of 50 drugs were approved in 2024 (94%), and 44 out of 46 drugs in 2025 (95.7%) were approved before their target PDUFA dates. Another statistic shows that 90% of approvals are before the PDUFA date. The possible reason is rooted in the back-and-forth correspondence between the company and the agency if they find issues that would result in a denial, referred to as a Complete Response Letter (CRL). The mindset of the FDA is that they want to give the company every opportunity to address any deficiencies before the deadline.

Author Created from Jefferies, BioPharmCatalyst, and Evaluate Pharma

Risks

CAPR is not a stranger to regulatory delays. Their CRL in 2025 ended up being a minor setback, but they were quick to provide the FDA with the data they needed. A regulatory delay could bleed out their cash reserves and result in further dilution. Another possibility is an approval, but a restrictive label that limits their total available market. Once they get into commercialization, they may find that insurance companies may view this as a supplement treatment instead of an essential treatment that they must reimburse. This could dampen their peak sales forecasts. Another factor that could affect the adoption is the requirement for an IV infusion every 3 months. Patient compliance is typically better with oral pills. Depending on the price before the announcement investors could experience a buy the rumor sell the news volatility. There is no real fallback position if they fail the trial because their StealthX exosomal platform is still in the early stages.

The shorts are hanging on to hope that there are some hiccups in the CMC manufacturing, which would give the FDA pause on approving the therapy. The top line readout met its primary and secondary endpoints, but the short points to the small sample size and the proximity to the statistical endpoint have the potential to fall short when the FDA does its own analysis. Any delay requiring more data could send the stock careening down to single digits, which is where it began its ascent.

Investment Summary

Capricor Therapeutics has been a battleground stock. They have navigated a lot of regulatory hurdles to get to this point. They have a strong following of supporters and DMD advocates looking for drugs that work. The existing treatment options, like Elevidys, fall short. Putting aside the black box warning, Elevidys attempts to manage the muscle wasting, but they drop the ball when it comes to treating the heart, and it is the cardiac dysfunction that ultimately takes lives. Deramiocel doesn't just treat the symptoms; its cardiosphere-derived cells actively target and repair the damaged cardiac tissue. It is a massive clinical bridge for a gap that has been left wide open for years.

From a trading perspective, CAPR is de-risked in ways most clinical-stage biotechs can only dream of:

The Balance Sheet is a Fortress: With $318 million in the bank, the standard bear argument of "imminent dilution" is dead in the water. They have enough capital to coast through the PDUFA and fund their commercial launch well into 2027.

Massive Commercial Backing: Their partnership with NS Pharma isn't just a handshake; it guarantees over $700 million in milestones plus double-digit royalties post-approval.

Platform Technology: Their exosomal drug delivery platform represents the evolution of small molecules and biologics into a rising new class of drugs.

Regulatory Tailwinds: With the FDA recently pushing through drug approvals in record times and moving away from rigid, one-size-fits-all manufacturing standards for cell therapies, Capricor is pushing on an open door.

While there are always execution risks in commercialization and insurance reimbursement, the risk-to-reward ratio here is heavily skewed to the upside. Whether you are playing the equity for a long-term breakthrough or leveraging the rich premiums in the options chain, Capricor represents one of the most compelling risk-managed biotech setups on the board.

Comments

Log in or sign up to join the conversation.