TM Editors' note: This article discusses a penny stock and/or microcap. Such stocks are easily manipulated; do your own careful due diligence.

Pure play in active VR - Called the "Peloton (PTON) for Gamers"

Leveraging the "Made for Meta" Ecosystem

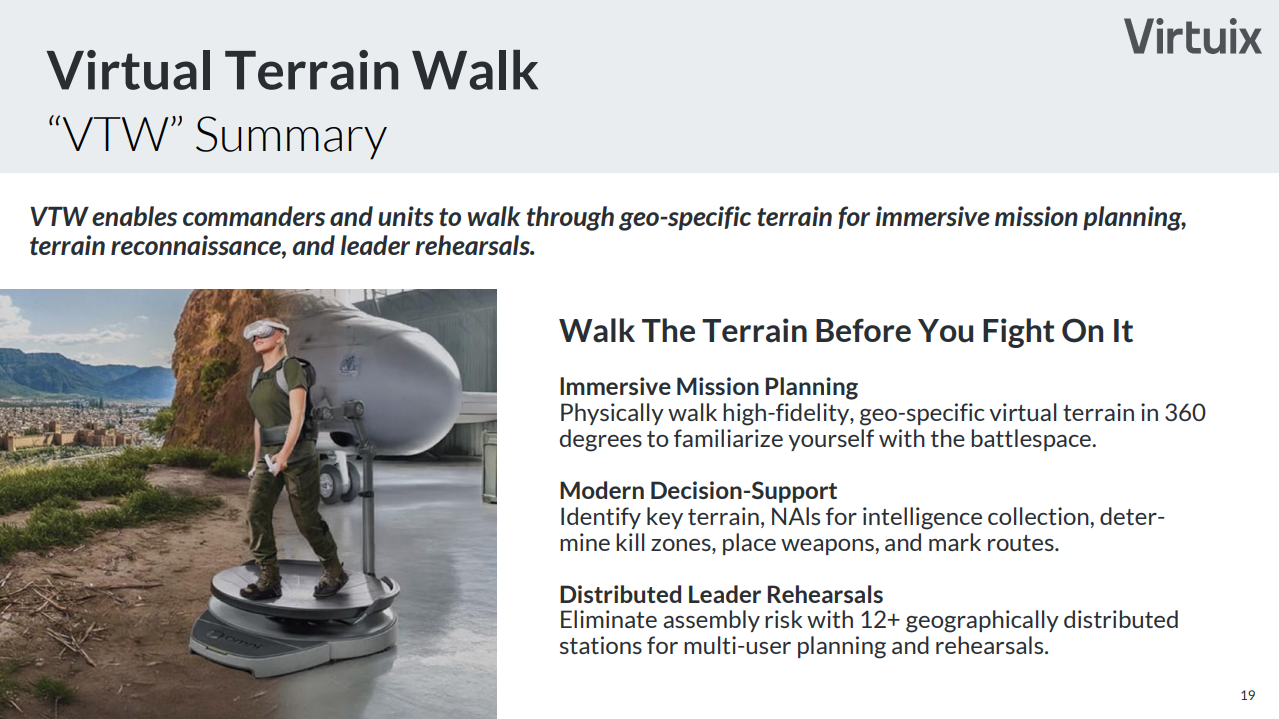

Defense Department interest accelerating - Virtual Terrain Walk

Virtuix Holdings (Nasdaq: VTIX) is one of the pioneers of VR and its current offerings of Xtreme Gaming, fitness, and defense simulations positions it to be a disruptor in Meta Platforms Inc. (Nasdaq: META) VR ecosystem and the US Military’s modernization. VTIX isn’t just a VR accessory maker, they are the essence of the next evolution of the market. Their hardware sales were at capacity while new games were driving recurring sales from their installed customer base. This led to a 1.5 yr backlog that is being relieved by an expansion of their manufacturing line.

Refinements being made in META’s “Made for Meta" program which connects the Omni One into the largest VR user base on the planet is really just a dress rehearsal for the military business. Their Virtual Terrain Walks (VTWs) are vital to the military mission as they tackle the challenges of military readiness, responsiveness, and cost scalability in one package. The diversified revenue streams derisk the business as they make incremental steps toward military contracts that have the potential to take sales to a parabolic trajectory. The stock is consolidating from a bumpy IPO and consolidating in front of a massive potential defense contract.

Company Background

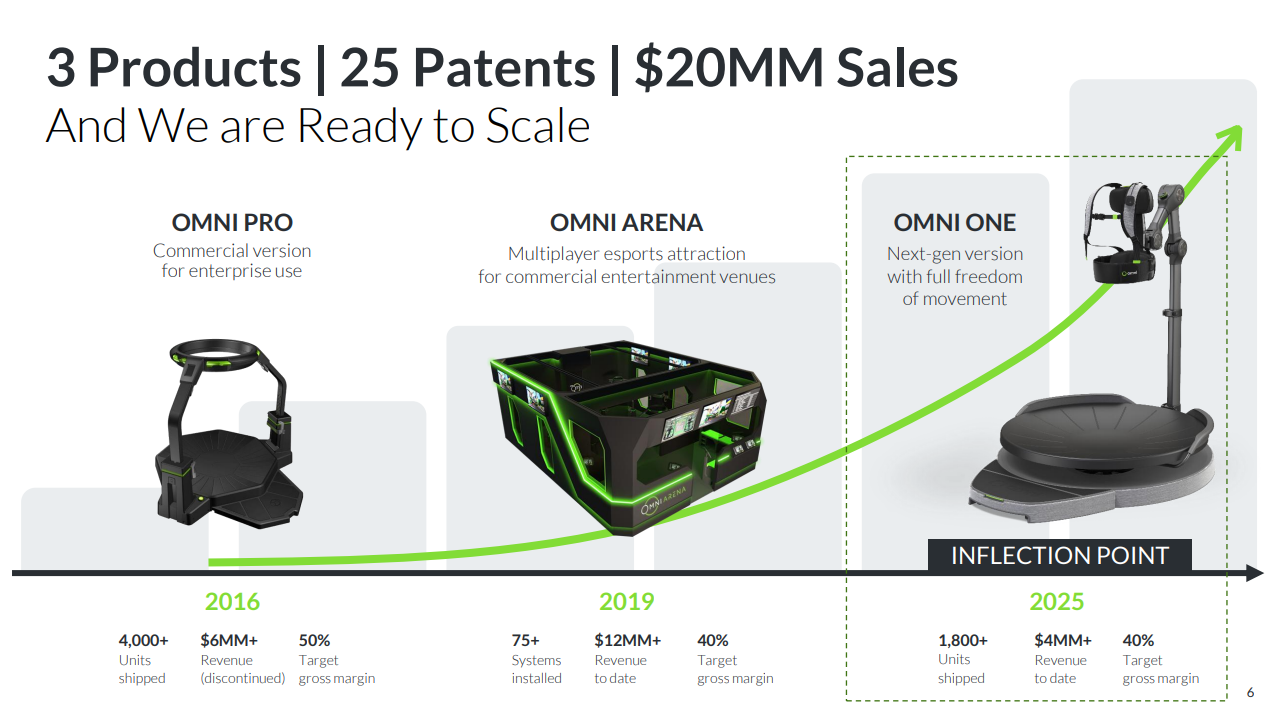

Virtuix, founded in 2013 by CEO Jan Goetgeluk—a former J.P. Morgan banker who quit his job to work full time after developing his prototype. His quest was to solve the problem of walking around in VR without needing a huge space and bumping into things. They call this issue the VR locomotion challenge. VTIX’s patented Omni treadmill, allows for 360-degree walking, running, and crouching. They solved this challenge in 2013 when they launched their kickstarter campaign that ultimately shipped out 3000 units by mid 2017. During the campaign he pitched Mark Cuban, Robert Herjavec, Barbara Corcoran, Kevin O’Leary, Daman John on Shark Tank, but nothing came of it until Mark Cuban invested in a star studded private offering of multiple rounds that stretched over 10 years and ultimately landed the company $50 million.

Early successes include shipping over 4,000 Omni Pro units to arcades in 45 countries and 80 Omni Arena installations. They continue generating recurring revenue from maintenance and upgrades. Outside of headsets, the Omni Pro units represent the largest hardware platform in VR. In 2024 they unveiled the Omni One which was a nex-gen home version with a library of 50 VR games.

After diversifying its revenue mix the company decided to go public via direct listing on Nasdaq in January 2026 at $8.75. Its investment banker Maxim raised $11 million in equity and a $50 million equity line. The proceeds shored up its manufacturing capacity to 3,000 units per month which represents $100 million in potential revenue.

META Market Potential

The global virtual‑reality market is forecast to grow at over 20% annually and hit around $235 billion by 2030, but if we look at the AR/VR software market subset it was pegged at $51 billion in 2024 and projected to explode toward $700 billion by 2034. Many may not realize it but the VR and Extended Reality (XR) ecosystems encompass tens of millions of users on just Meta's Quest platform. There is an expansive library of games and experiences for users to choose from. VTIX is now part of the “Made for Meta” program which started in mid February and allows piggy backing off of META’s enormous user base. Omni One, VTIX’s marquis product, is a certified, full-body motion platform and is endorsed by the world’s largest VR platform. This META partnership balloons the customer base from hardcore VR enthusiasts to the mass market who already own META headsets and are active users of META’s apps and games.

The introduction of this platform to the META universe will drive recurring revenue of $44 per new user. Not only will there be additional hardware sales from friend referrals, but historical trends show the users will subscribe to the monthly Omni Online subscription for leaderboard access, and purchase an average of one new VTIX library game per month. While this consumer base is massive and will grow through word of mouth and marketing it pales in comparison to the potential of the industrial and defense market. These customers have unique customization requirements, and need them to be implemented quickly and securely.

Fitness Market Tailwinds and Beyond AI

While the META market is huge, the Omni One is also competitive in the fitness category. A couple of minutes in the Omni One playing a game and fitness enthusiasts will see the potential for disruption. The global fitness‑equipment market is expected to grow at roughly 5–6% per year and approach $24 billion by 2034. Peloton (Nasdaq: PTON) is a dominant player in the space generating $2.4 billion in revenue in 2025 and has 6.3 million active users through its app and connected hardware. An interesting anecdote is that both PTON and VTIX had their kickstarter campaigns back in 2013 but no one envisioned the Omni One as the “Peloton for Gamers” VR fitness play.

These industrial applications span multiple sectors, including corporate training, education, healthcare, and real estate design. The ease of creating virtual environments facilitated by AI has facilitated the growth in this category. AI helps create virtual environments where employees can perform tasks and then get evaluated on their performance, or where real estate professionals can show clients remote properties.

The Multiplier: Virtual Terrain Walks (VTW)

The most compelling catalyst for VTIX is the Virtual Terrain Walk (VTW). One of the reasons the American military boasts such a successful track record in special operations boils down to training and intelligence. The units train in real life mockups but these take time to build and they are expensive to build. What happens if the location is changed last minute? Current simulations have expensive projection systems in remote locations and can only be used by a couple of users at a time and don't give the full 360 degree effect. Room scale VR systems with headsets are cheaper but can only be used for small mission areas relegated to under a 45ft room. Mission practice is vital, but live-fire exercises are prohibitively expensive, logistically complex, and physically taxing. The Omni One capability enables multiple soldiers from anywhere in the world with access to the platform to logon and join a mission and enter a virtual world that was created in hours and replicated down to the last inch and allow the virtual firing of weapons and all sorts of wartime scenarios to be simulated.

Virtuix’s VTWs solve for three critical variables in a single package:

Readiness: Soldiers can walk through 1:1 digital twins of real-world mission sites.

Responsiveness: Rehearsals can be spun up in hours, not weeks.

Cost Scalability: The cost of a digital "walk" is a fraction of the fuel and equipment wear-and-tear of a physical exercise.

Diversified Streams & Big Defense Upside

Virtuix’s revenue is diversified into 3 main buckets, consumer, enterprise, and defense. At the moment the majority of the revenue is legacy revenue from the arcades, but that is being eclipsed by the new “Made by Meta" initiative and backed by an expanded manufacturing facility. The company does have military sales but they are not of the size and scale that is possible.

Consumer: High-end home fitness and gaming.

Enterprise: Commercial VR centers and arcades.

Defense: Tactical training and mission rehearsal licensing.

These underlying revenue streams de-risk the investment allowing the management team options to pivot if economic issues or supply chain issues come into play. The consumer and enterprise segments provide for steady growth and leave open the explosive upside of a military contract over a number of years and in the millions. VTIX is essentially marking time until the military gets comfortable to embrace the VTIX monopoly as the only virtual platform capable of immersing soldiers into their environment. You can't do war-games on any other platform.

Competition & Defensible Moat

When you develop an incredibly innovative product the tendency is to say you have no competition, but a case can always be made for competition. VTIX basically created the omni-directional treadmill, but the market place is expanding. There are a couple of copy cat companies like KAT VR, Cyberith and Xelerate VR that make up the bulk of the market. All the other competitors are primarily hardware based and are private companies without deep financial pockets. There are a number of comparison videos that talk about the pros and cons but the consensus is skewed toward the Omni One.

Because Virtuix had a first market mover advantage by forming the market they enjoy an extremely solid defensible moat. Here is why.

Patent Protection: VTIX has 25 issued patents and has protected its core locomotion mechanics that allows people to run and get a workout at the same time.

Operational Record: There have been sales of over 4,000 pro units and now the Omni One so many of the bugs have been worked out along with the customer support infrastructure that goes with it.

Made for Meta Status: The agreement with META put them on top as a trusted vendor so all the other competitors are being compared to the Omni One and have to fight for their share of the market.

Risks

One of the biggest risks in the consumer market is satiating demand. The increased manufacturing capacity to 3,000 units per month has derisked the company, but other risks remain. Moving the manufacturing to Zhuhai China opened up the possibility of supply reductions due to the ongoing tariff war. Virtuix needs to generate consistent consumer interest and that translates into revenue. If marketing fails to create that demand pull and get the traction it needs to keep growing the consumer base it's going to negatively impact the strategy which now enjoys high demand, high margins, and recurring revenue streams. The push for defense department business represents a binary risk. There is a long lead time in awards and significant investment is needed complying with government regulations. In the end there is no guarantee of an award that could offset the capital investment. Ultimately their continued operating losses are the biggest cause for concern because it makes them reliant on continued financing that leads to more dilution. Offsetting some of these risks is their successful track record and star studded client base backstopping any future financings. Until the company starts generating predictive consistent revenue, the business remains vulnerable to the classic challenges of scaling a business.

Financial Snapshot

Virtuix Holdings had its IPO on January 26, 2026. For the 9 months ended December 31, 2025, they had a 41% increase in YoY revenue to $3.0 million with improving gross margins that went from -17% to 29%. This margin inflection is a key metric in establishing the trend toward profitability as they increased price from $2595 to $3495 and ended the sale of discounted investor units. Margins may very well continue to expand due to the new production facility in China.

Their operating expenses are still problematic. They recorded a quarterly loss of $2.7 million for the quarter ending December 31, 2025. This highlights the need for cash. They raised $11 million in proceeds to have the funds needed to get their product to market when also factoring in their $50 million equity line. Based on the financials, they are burning an estimated $600,000 monthly which gets them through calendar 2026 assuming no extraordinary events.

Founder Led Management

Virtuix is the creation of its founder Jan Goetgeluck as he successfully led from a Kickstarter prototype to a successful Nasdaq listing. He has a JP Morgan pedigree but he has also surrounded himself with a team designed to get him to the next level. A recent addition to the team with the appointment of Brett Moyer who brings public company, capital markets, and operating experience to support the VTIX growth initiatives, highlights Jan’s expanding executive bench. Moyer was the CFO of DataVault AI (DVLT) (Nasdaq: DVLT) and former CEO of WiSA Technologies (WISA) (Nasdaq: WISA). Both of these companies experienced major inflection points while he was there. The management team holds 15.7% of the company and is very much aligned with shareholders in building value. They are at a major infection point with their defense business as they have to continually weigh the benefits and risks of investing in the defense initiative.

Upcoming Catalysts & Milestones

VTIX is in execution mode after their IPO. They need to demonstrate to the market that they have what it takes to expand their user base given the “Made for Meta” mark of excellence. The defense department business could be a game changer and a major inflection point for the company if they land the contracts.

Defense Program Progress: They have a couple of installed systems at the military academies which represents a big foot in the door but they need multi year contracts for the Virtual Terrain Walks (VTW).

European Rollout: Management indicated the European rollout would begin at the end of April. This was a priority for the company to scale its direct-to-consumer (DTC) business outside the USA. It also represents a logistical challenge.

Made for Meta Launch: The “Made for Meta” partnership needs to deliver volume sales given the size of META’s installed base. If they deliver on sales and recurring revenue it could change market perception from wait and see to fear of missing the train. Depending on adoption this could come at any time from now.

Next Earnings Call: This will be the second earnings call for a public company. Investors will be looking for margin improvement and try to get a sense of how sales have been ramping. They will be looking at the need for dilution or if organic growth can propel operations forward.

The Bottom Line

Virtuix has moved beyond the proof-of-concept phase and they need to show investors they can monetize this platform technology. They have an excellent management team, a great product, an incredible partnership with “Made for Meta” but they have to execute. They have all the ingredients in place to scale the business with the manufacturing capacity to do $100 million this year. They have money from the IPO for Marketing, they have the “Made for Meta" designation, they have battle tested customer support, and they have cutting edge technology. VTIX is a market disruptor and has all the elements that they need to succeed in the defense arena. Investors know that this is a long cycle investment but current events are showing that military preparedness is a priority and this puts Virtuix in the cross hairs of a large military contract award that could send revenues parabolic. Investors looking for a "pure play" in VR, VTIX is a ticker to watch.

Comments

Log in or sign up to join the conversation.