| ||||||||||||||||||||

| ||||||||||||||||||||

| ||||||||||||||||||||

| ||||||||||||||||||||

| ||||||||||||||||||||

| ||||||||||||||||||||

|

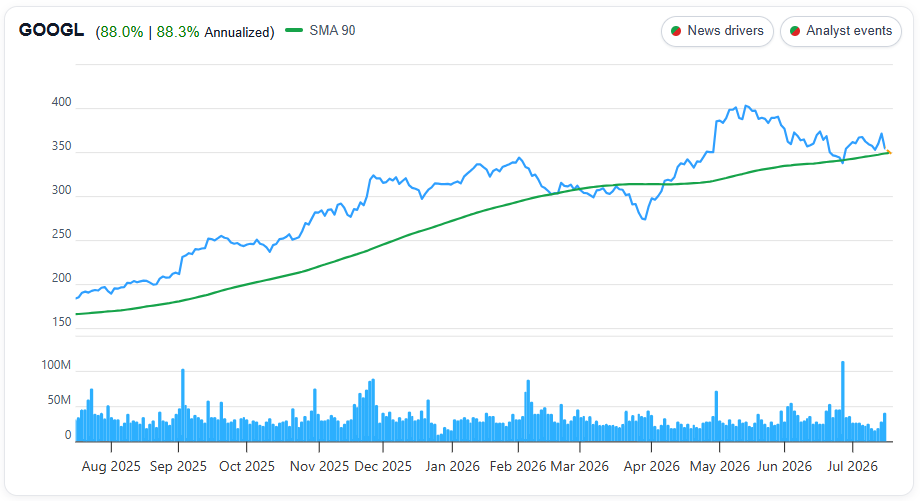

Alphabet’s $200 Billion Execution Scare

Alphabet shed $200 billion in market value after Gemini AI delays sparked execution fears.

At the time of publication, Alphabet Inc. (GOOGL) and Meta Platforms (META). The author has no position in the other securities mentioned. The author does not plan to initiate or change a position within 72 hours of publication. The author was not compensated by any company mentioned in this article.

InvestorsGrow and the Morning Note are published for informational and educational purposes only. Nothing in this email or on InvestorsGrow.com should be considered personalized investment, financial, legal, tax, or accounting advice, or a recommendation to buy, sell, or hold any security. The content is general in nature and does not take into account your investment objectives, financial situation, risk tolerance, or individual needs. Investing involves risk, including the possible loss of principal. Past performance is not indicative of future results. Opinions are as of the publication date and may change without notice. Data and information are believed to be reliable but are not guaranteed. The author, InvestorsGrow, affiliates, and/or contributors may hold, buy, or sell securities discussed. Article-specific positions, compensation, or conflicts are disclosed where applicable. You are solely responsible for your own investment decisions and should conduct your own research and consult a qualified professional before making financial decisions.

Full disclosures and terms are available at InvestorsGrow Disclosures & Terms

Comments

Log in or sign up to join the conversation.