We have written before about strategies for retiring early, such as our How To Retire At 50 post. Retiring early can look like a herculean task for many people, though, requiring big cuts in current spending, or boosting saving and investing to levels that seem out of the question.

So let's consider a more typical scenario: A person or a couple, doing all (or most) of the right things financially, who gets to their 40s and wants to make sure they're on track for retiring around the usual time, in their mid-60s. Are there things that the retirement-conscious investor in her 40s should be thinking about that weren't very important a few years earlier?

The short answer is, probably not all that much. Keep on keeping on: The rules for planning for retirement are largely still the same rules once you get to your 40s. If you have been diligently saving and investing in 401(k)s and IRAs thus far, don't stop now.

That said, here are a few things to consider.

Check in on your risk tolerance

How did you handle the market's gyrations circa 2008? Would you handle them the same way now, several years on?

Panic selling in your 30s or earlier, while not ideal, is probably not a retirement-delaying event. After all, you're still decades away from retiring, and time is your friend in such a case.

But the closer you get to retirement (which you are, every day), the more serious the repercussions of veering off course can be. Self-knowledge is critical here: If you know a 10% market correction would keep you up at night, and a 15% (or worse) correction would cause you to abandon your plan, sell all of your investments, and go to cash, it could be time to have a fresh look at how your retirement assets are allocated.

A more conservative approach will almost surely mean slower growth. But if the markets head south, your investments should not drop in value as much. And if such an approach would keep you from bailing on the markets entirely in case of a correction, it might be worth considering.

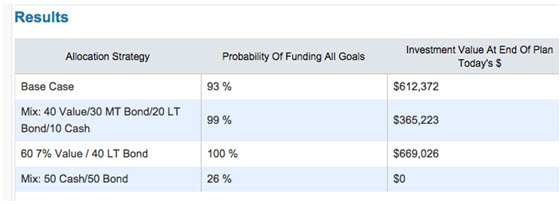

WealthTrace's Asset Allocation Scenarios functionality can help walk you through the options. You can use this feature of the program to see how various asset allocation strategies could affect your plan compared to your current (base case) allocation strategy.

Whoa, only 26% probability of funding all goals?? Maybe the sleepless nights during times of market volatility are worth it.

Get the 529 plan funded

A lot of people are rightly concerned about health care costs as they age, but the real wildcard for a lot of families is education funding. Will Junior go to college? If so, how much of Junior's college costs will you want to cover? What will college cost in 10 or 15 years? Private school, or public school? So much of it is impossible to predict accurately, so the cost is difficult to estimate.

If you have kids that you are planning to send to college and you don't know what a Section 529 plan is, stop reading this post immediately and start Googling--this is important! But hopefully you know what we are talking about, and, depending on your kids' ages, you have begun funding the plan(s), or at least have it on your radar screen.

WealthTrace can help with running a range of numbers. For example, let's assume you have a child that you expect will start at a four-year university several years from now. You want to cover as much of the cost as possible. With WealthTrace, you can enter the expense in today's dollars, and then have the program handle the calculation of what that cost might look like several years from now and beyond. In this example, we're assuming the all-in costs of college will increase by 10% annually between now and when you become an empty nester, and then by 5% during the college years:

Can Junior really finish college in four years? Maybe we ought to make that five years, just in case.

Once you have that expense entered, you can use the sliders on the site to stress-test your assumptions. What is the effect on your plan if you bump up college costs by, say, $25,000 per year? You can see the results of your changes right on the screen, instantaneously.

(And while we're on the topic, is private school--pre-college, that is--under consideration? If so, you are going to need to plan for it. WealthTrace can handle this in a similar fashion.)

Play catch-up

If you're already maxing out your 401(k) contributions, you won't be able to make additional contributions ($6,000 annually as of this writing) until you turn 50. But there are other ways to save, of course.

If you run your numbers through WealthTrace and find that you're a bit behind where you need to be, consider finding a way to sock away a little more. WealthTrace can help you run through such what-if scenarios to help you find out how they might affect your retirement plans. Could (for example) an extra few thousand dollars saved per year in your 40s shave a couple of years off of your target retirement date?

A little here, a little there . . .

Another option would be to bump up the aggressiveness of some of your investment choices, taking into account the aforementioned tolerance for risk. More growth stocks and fewer value stocks, for example.

Crossing the 40 line shouldn't mean any wholesale changes to your strategy should be needed. As long as your risk tolerance and life goals are about the same as before, just keep checking your financial plan periodically to make sure you're still on track.