Image source: Pixabay

US consumer spending is on track to drive third-quarter GDP growth of perhaps 3-3.5%. However, this is not sustainable. American consumers are running down savings and using their credit cards to finance a large proportion of this. With financial stresses becoming more apparent and student loan repayments restarting, a correction is coming.

Inflation pressures are moderating

Today’s main data release is the July personal income and spending report and it contains plenty of interesting and highly useful information. Firstly, it includes the Federal Reserve’s favoured measure of inflation, the core Personal Consumer Expenditure deflator, which is a broader measure of prices than the CPI measure that is more widely known. It rose 0.2% month-on-month for the second consecutive month, which is what we want to see as, over time, that sort of figure will get annual inflation trending down to 2% quite happily.

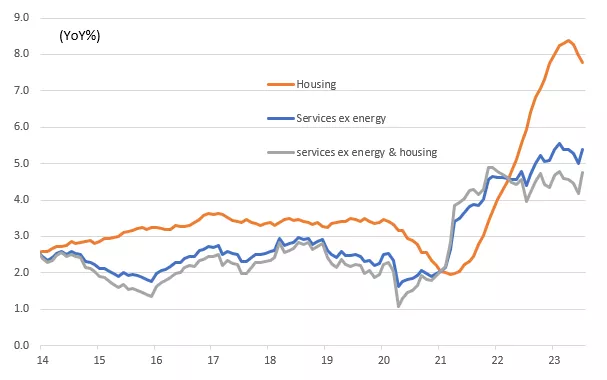

Services PCE deflator (YoY%)

Image Source: Macrobond, ING

The slight negative is the core services ex housing, which the Fed is watching carefully due to if being more influenced by labour input costs. It posted a 0.46% MoM increase after a 0.3% gain in June so we are not seeing much of a slowdown in the year-on-year rate yet as the chart above shows. With unemployment at just 3.5%, a tight jobs market could keep wage pressures elevated and mean inflation stays higher for longer so we could hear some hawkishness from some Fed officials on the back of this. Nonetheless, the market is seemingly shrugging this off right now given signs of slackening in the labour market from the latest job openings data and the Challenger job lay-off series.

Consumer spending is strong but is unlikely to be sustainable

We then turned to personal spending, which was strong, rising 0.8% MoM nominally and 0.6% MoM in real terms. This gives a really strong platform for third-quarter GDP growth, which we are currently estimating to come in at an annualised rate of somewhere between 3% and 3.5%. However, the key question is how sustainable this is – we don't think it is. The robust jobs market certainly provides a strong base, but wage growth has been tracking below the rate of inflation. Note incomes rose just 0.2% MoM in July. Maybe it is that confidence of job security that is encouraging households to seek to maintain their lifestyles amidst a cost-of-living crisis, via running down savings accrued during the pandemic and supplementing this with credit card borrowing.

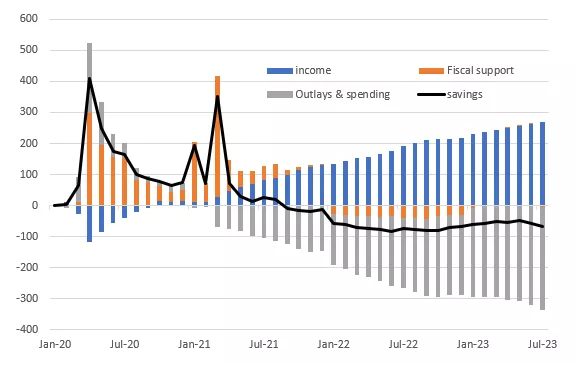

The problem is savings are finite and the banks are tightening lending standards significantly. Credit card borrowing costs are the highest since records began in 1972 so there is going to be a lot of pain out there. The chart below shows the monthly flows of excess savings since the start of the pandemic. Fiscal support (stimulus checks and expanded unemployment benefits) more than offset falling income resulting from job losses in 2020. Meanwhile, less spending versus the baseline due to Covid constraints further boosted the accumulation of savings.

Contributions of monthly changes in income and spending to the flow of savings ($bn)

Image Source: Macrobond, ING

Then through 2021 spending picked up, but then through 2022-2023, the nominal pick-up in incomes has been less than the increase in spending. Consequently, we have seen savings flows reverse and now we are running them down each and every month, which is not sustainable over the long term.

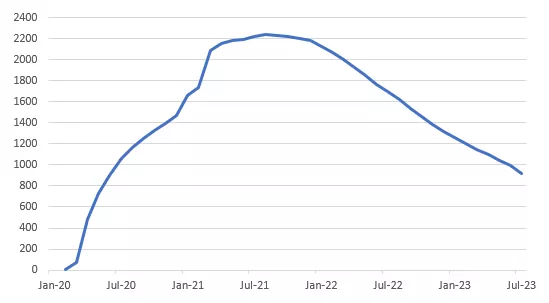

Stock of excess savings peaked at $2.2tn, but we have been aggressively running this down ($tn)

Image Source: Macrobond, ING

Excess savings will soon be exhausted and financial pressures will intensify

Based on this data, the $2.2tn of excess savings accumulated during the pandemic, $1.3tn has already been spent. At the current run-rate, it will all be gone by the end of the second quarter of 2024 and for low and middle incomes that point will come far sooner. With banks far more reluctant to provide unsecured consumer credit, based on the Federal Reserve’s Senior Loan Officer Opinion survey, the clear threat is that many struggling households may soon find their credit cards are being maxed out and they can’t obtain more credit. With student loan repayments restarting, we expect consumer spending to slow meaningfully from the late fourth quarter onwards and turn negative in early 2024.

More By This Author:

Italian Inflation Continued To Decelerate In August

FX Daily: Low Vol Environment Continues

China PMIs Remain Downbeat

Comments

Log in or sign up to join the conversation.