Beijing, China

Mixed news - but no real improvement in total

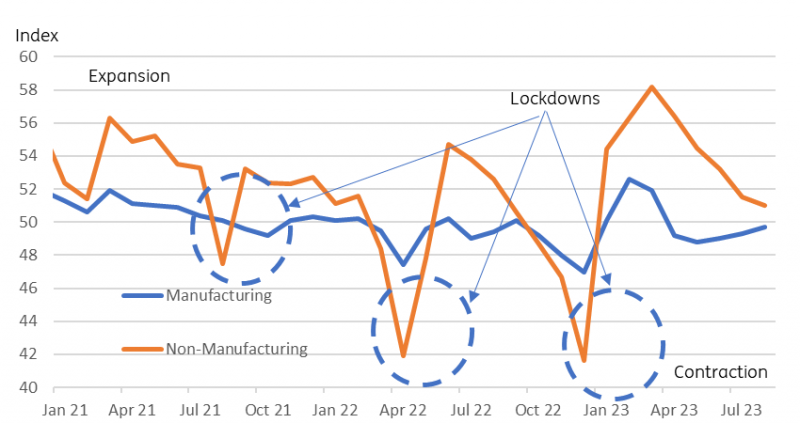

The latest official PMI data were not uniformly bad. The manufacturing index actually rose slightly, to 49.7, and this is the third consecutive increase since the May trough of 48.8. But it remains below the 50-level that is associated with expansion, and so merely represents a moderation in the rate of decline. That may be of some comfort to those of a sunny disposition.

The non-manufacturing series, which had reflected the bulk of the post-re-opening recovery, fell further in August. The index of 51.0 was a little lower than the forecast figures (51.2) but it is at least still slightly above contraction territory.

China official PMIs (50 = threshold for expansion / contraction)

CEIC, ING

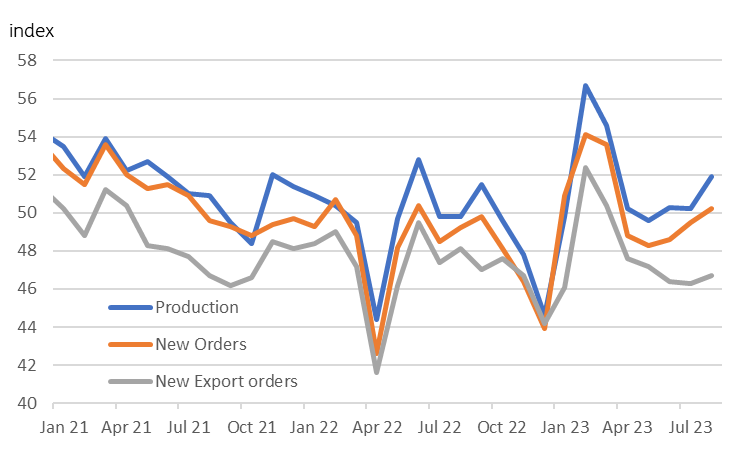

Brighter signs in manufacturing

Looking at the components underlying both series and starting with the manufacturing series: the latest data show an improvement in production to a point which actually points to expansion. That has to be tempered by the forward-looking elements of orders. Here, the data is mixed. Total orders have improved to hit the 50 threshold signalling that contraction has ended. This must be mainly domestic orders, as the export orders series remains bombed out. But that at least provides some encouragement about the near-term outlook.

Manufacturing PMI components

CEIC, ING

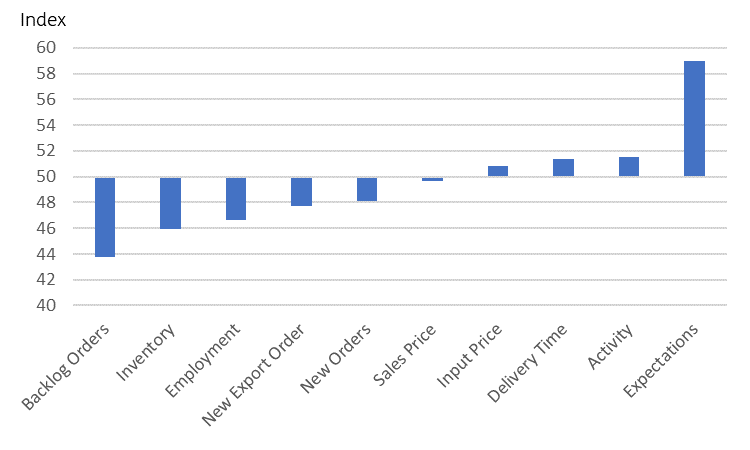

Outlook for service sector remains negative

The forward-looking elements of the service sector PMI index remain in contraction territory, unlike their manufacturing counterparts, and that suggests that the headline index has probably not yet troughed and will fall further. A glimmer of hope may be in the export series, which, while clearly continuing to signal contraction, did fractionally rise this month.

Overall, though, both series seem to be converging on a point close to 50 consistent with an economy that is neither expanding nor contracting. Things could be worse. But markets are not likely to take too much comfort from this set of data.

Non-manufacturing PMI sub-components

CEIC, ING

More By This Author:

High 2024 Borrowing Needs In Poland No Longer Fundable Locally

Inflation’s Second Wave: Are We Really Watching A 70s Rerun?

Rates Spark: Losing Buoyancy

Comments

Log in or sign up to join the conversation.