Why You Should Question “Buy And Hold” Advice

I recently received an email from an individual that contained the following bit of portfolio advice from a major financial institution:

“Despite the tumble to begin this year, investors should not panic. Over the long-term course of the markets, investors who have remained patient have been rewarded. Since 1900, the average return to investors has been almost 10% annually…our advice is to remain invested, avoid making drastic movements in your portfolio, and ignore the volatility.”

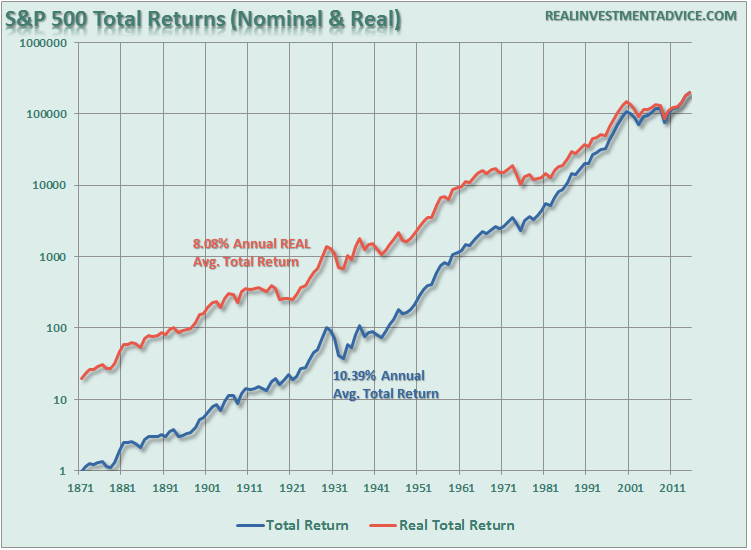

First of all, as shown in the chart below, the advice given is not entirely wrong – since 1900, the markets have indeed averaged roughly 10% annually (including dividends). However, that figure falls to 8.08% when adjusting for inflation.

(Click on image to enlarge)

It’s pretty obvious, by looking at the chart above, that you should just invest heavily in the market and “fughetta’ bout’ it.”

If it was only that simple.

There are TWO MAJOR problems with the advice given above.

First, while over the long-term the average rate of return may have been 10%, the markets did not deliver 10% every single year. As I discussed just recently, a loss in any given year destroys the “compounding effect:”

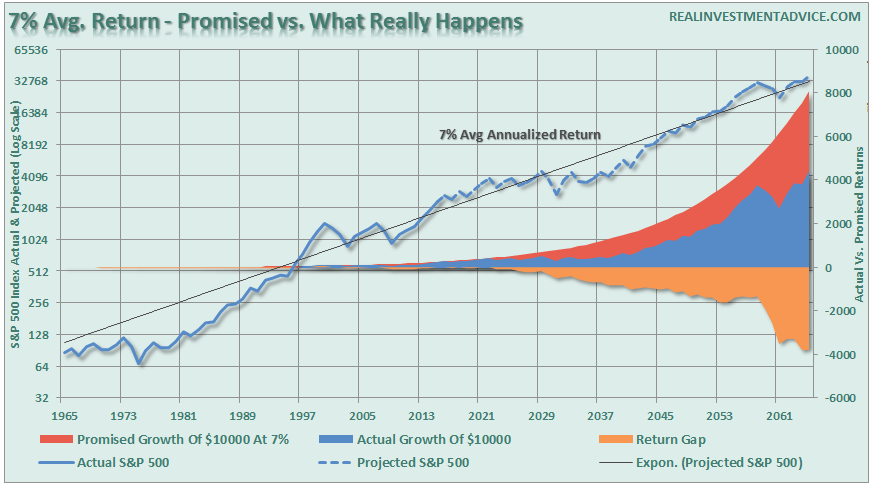

Here is another way to view the difference between what was “promised,” versus what “actually” happened. The chart below takes the average rate of return, and price volatility, of the markets from the 1960’s to present and extrapolates those returns into the future.

(Click on image to enlarge)

When imputing volatility into returns, the differential between what investors were promised (and this is a huge flaw in financial planning) and what actually happened to their money is substantial over the long-term.

The second point, and probably most important, is that YOU DIED long before you realized the long-term average rate of return.

The Problem With Long-Term

Let’s consider the following facts in regards to the average American. The national average wage index for 2014 is 46,481.52 which is lower than the $50,000 needed to maintain a family of four today.

- 63% of can’t deal with a $500 emergency

- 76% have less than $100,000; and

- 90% have less than $250,000 saved.

If we assume that the average retired couple will need $40,000 a year in income to live through their “golden years”they will need roughly $1 million dollars generating 4% a year in income. Therefore, 90% of American workers today have a problem.

However, what about those already retired? Given the boom years of the 80’s and 90’s that group of “baby boomers” should be better off, right?Not really.

- 54% have less than $25,000 in retirement savings

- 71% have less than $100,000; and

- 83% have less than $250,000.

(Now you understand why “baby boomers” are so reluctant to take cuts to their welfare programs.)

The average American faces a real dilemma heading into retirement. Unfortunately, individuals only have a finite investing time horizon until they retire. Therefore, as opposed to studies discussing “long term investing” without defining what the “long term” actually is – it is “TIME” that we should be focusing on.

When I give lectures and seminars I always take the same poll:

“How long do you have until retirement?”

The results are always the same in that the majority of attendee’s have about 15 years until retirement. Wait…what happened to the 30 or 40 years always discussed by advisors?

Think about it for a moment. Most investors don’t start seriously saving for retirement until they are in their mid-40’s. This is because by the time they graduate college, land a job, get married, have kids and send them off to college, a real push toward saving for retirement is tough to do as incomes, while growing, haven’t reached their peak. This leaves most individuals with just 20 to 25 productive work years before retirement age to achieve investment goals.

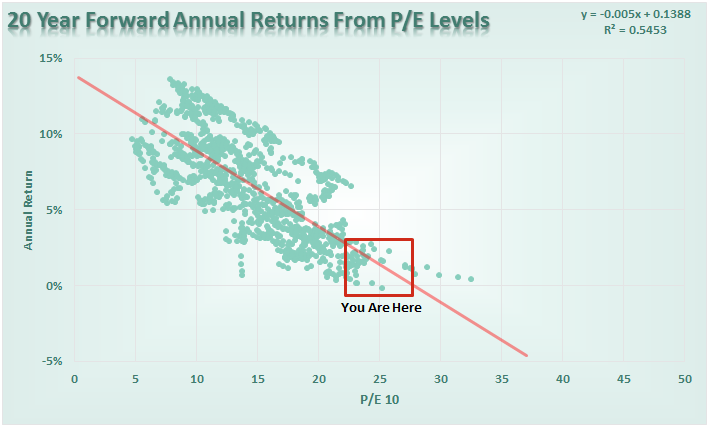

Here is the problem. There are periods in history, where returns over a 20-year period have been close to zero or even negative.

(Click on image to enlarge)

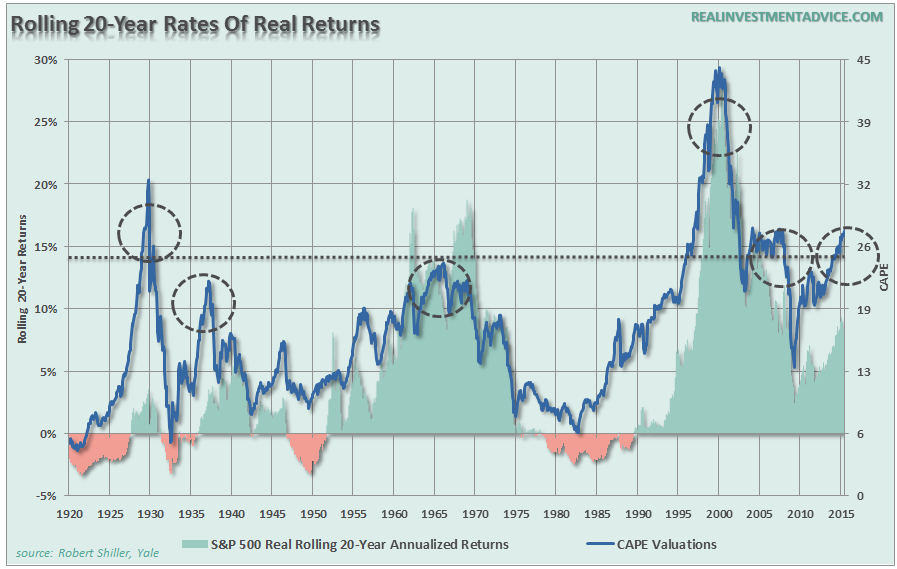

(Click on image to enlarge)

This has everything to with valuations and whether multiples are expanding or contracting. As shown in the chart above, real rates of return rise when valuations are expanding from low levels to high levels. But, real rates of return fall sharply when valuations have historically been greater than 23x trailing earnings and have begun to fall.

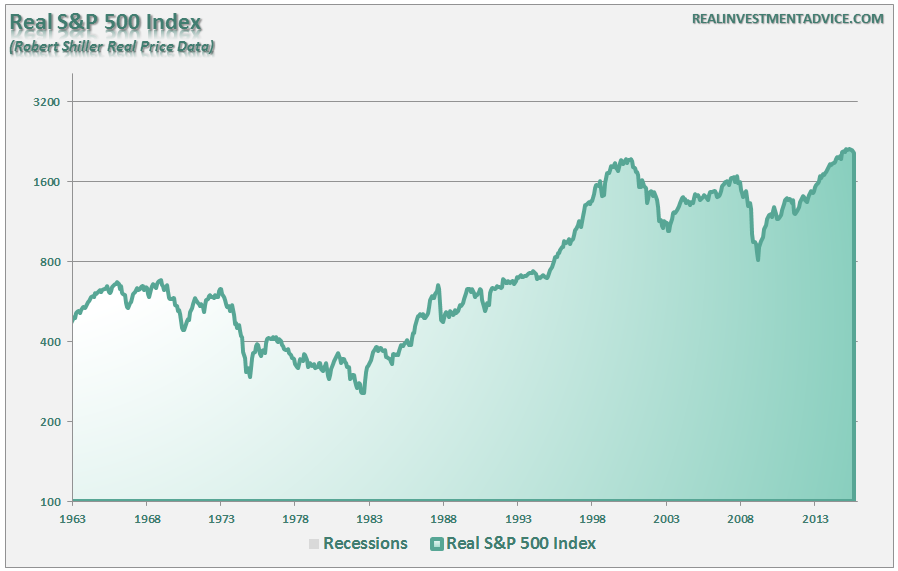

But the financial institution, unwilling to admit defeat at this point, and trying to prove their point about the success of long-term investing, drags out the following long-term, logarithmic, chart of the S&P 500. At first glance, the average investor would agree.

(Click on image to enlarge)

However, the chart is VERY misleading as it only looks at data from 1963 onward and there are several problems:

1) If you started investing in 1963, at the end of 1983 you had less money than you started with. (20 Years)

2) From 1983 to 2000 the markets rose during one of the greatest bull markets in history due to a unique collision of variables, falling interest rates and inflation and consumers leveraging debt, which supported a period of unprecedented multiple (valuation) expansion. (18 years)

3) From 2000 to Present – the unwinding of the stock market bubble, excess credit and speculation have led to very low annual returns, both a nominal and real, for many investors. (15 years and counting).

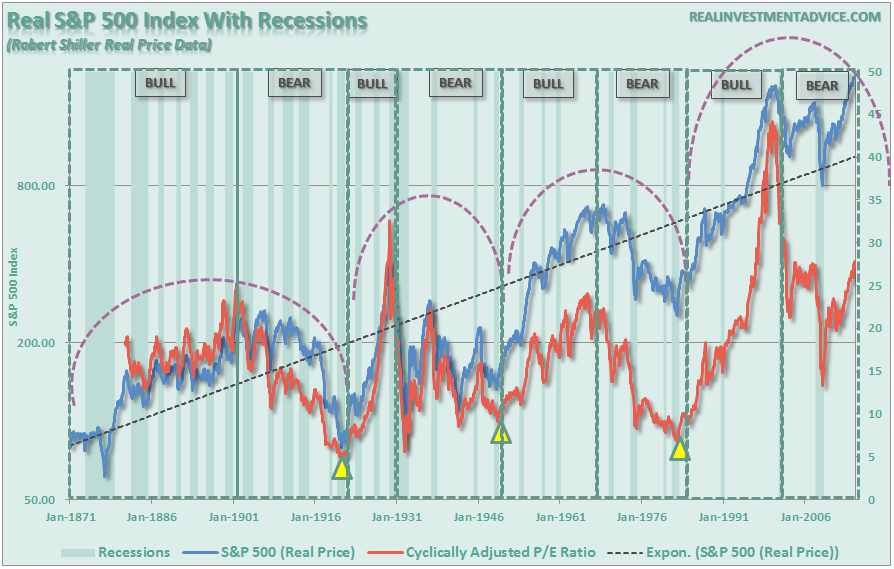

So, as you can see, it really depends on WHEN you start investing. This is clearly shown in the chart below of long-term secular full-market cycles.

(Click on image to enlarge)

Here is the critical point. The MAJORITY of the returns from investing came in just 4 of the 8 major market cycles since 1871. Every other period yielded a return that actually lost out to inflation during that time frame.

The critical factor was being lucky enough to be invested during the correct cycle. With this in mind, this is where the financial institutions commentary goes awry with selective data mining:

“Among the key findings: On average, participants who kept contributing to their retirement plans throughout the 18-month period (October 2008–March 2010) had higher account balances than those who stopped contributing; Participants who maintained a portion of their retirement plan asset in equities throughout the entire period ended up with higher account balances than those who reduced their equity exposure amid the peak period of market distress.

(Click on image to enlarge)

Thus, retirement investors who kept contributing to their plan and who maintained some exposure to equities throughout the period were better off throughout the market’s 18-month bust-boom period than those who moved in and out of the market in an attempt to avoid losses. Retirement investors who kept exposure to equities amid the peak of the global financial crisis ended up with higher account balances on average than those who reduced their equity exposure to 0%.”

The main problem is the selection of the start and ending period of October, 2008 through March, 2010. As you can see, the PEAK of the financial market occurred a full year earlier in October, 2007. Picking a data point nearly 3/4ths of the way through the financial crisis is a bit egregious.

In reality, it took investors almost SEVEN years, on an inflation-adjusted basis, to get “back to even.”

Every successful investor in history from Benjamin Graham to Warren Buffett have very specific investing rules that they follow and do not break. Yet Wall Street tells investors they can NOT successfully manage their own money and“buy and hold” investing for long term is the only solution.

Why is that?

There is a huge market for “get rich quick” investment schemes and programs as individuals keep hoping to find the secret trick to amassing riches from the market. There isn’t one. Investors continue to plow hard earned savings into a market hoping to get a repeat shot at the late 90’s investment boom driven by a set of variables that will most likely not exist again in our lifetimes.

Most have been led believe that investing in the financial markets is their only option for retiring. Unfortunately, they have fallen into the same trap as most pension funds which is that market performance will make up for a “savings”shortfall.

However, the real world damage that market declines inflict on investors, and pension funds, hoping to garner annualized 8% returns to make up for the lack of savings is all too real and virtually impossible to recover from.When investors lose money in the market it is possible to regain the lost principal given enough time, however, what can never be recovered is the lost “time” between today and retirement. “Time” is extremely finite and the most precious commodity that investors have.

With the economy on a brink of third recession this century, without further injections from the Fed to boost asset prices, stocks are poised to go lower. During an average recessionary period, stocks lose on average 33% of their value. Such a decline would set investors back more than 5-years from their investment goals.

This leads to the real question.

“Is your personal investment time horizon long enough to offset such a decline and still achieve your goals?”

In the end – yes, emotional decision making is very bad for your portfolio in the long run. However, before sticking your head in the sand, and ignoring market risk based on an article touting “long-term investing always wins,” ask yourself who really benefits?

As an investor, you must have a well-thought-out investment plan to deal with periods of heightened financial market turmoil. Decisions to move in and out of an asset class must be made logically and unemotionally.Having a disciplined portfolio review process that considers how various assets should be allocated to suit one’s investment objectives, risk tolerance, and time horizon is the key to long-term success.

Emotions and investment decisions are very poor bedfellows. Unfortunately, the majority of investors make emotional decisions because, in reality, very FEW actually have a well-thought-out investment plan including the advisors they work with. Retail investors generally buy an off-the-shelf portfolio allocation model that is heavily weighted in equities under the illusion that over a long enough period of time they will somehow make money. Unfortunately, history has been a brutal teacher about the value of risk management.

Disclosure: The information contained in this article should not be construed as financial or investment advice on any subject matter. Streettalk Advisors, LLC expressly disclaims all liability in ...

more

That advice to hold for the 8%-10% long-term average ignores that face on fire & feet in ice is on average "comfortable". If I need my money when market and my capital are in a 50% trough, my capital won't recover. And so many opportunities for greater capital expansion missed if not ready with cash near the bottom.