Image Source: Pexels

Something strange has occurred in the bond market. Despite expectations for interest rate cuts by the U.S. Federal Reserve (Fed), yields have risen since the start of the year, with the U.S. government's 10-year bond yield climbing nearly 70 basis points (bps) this year through April 10. This is a sharp reversal from what occurred in the fourth quarter of last year when the 10-year yield collapsed by 71 bps. Such swings aren't normal from a historical perspective. But bond market volatility remains elevated, and such variance from period to period has been the recent norm.

So, what's going on?

U.S. economic resilience is helping push up yields

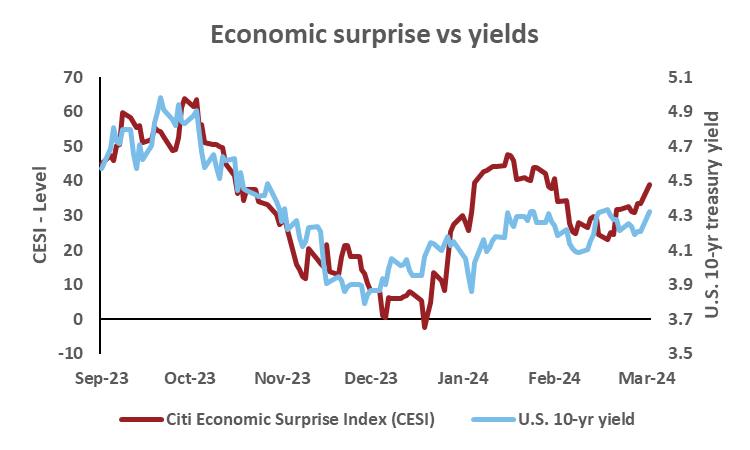

At the risk of oversimplifying, it's the economy. The U.S. economy isn't showing any immediate signs of substantive slowing, as macroeconomic data has trended better than expected. The Citigroup Economic Surprise Index (CESI) tracks economic data releases relative to consensus expectations. Chart 1 shows the CESI for the U.S. trended lower over the fourth quarter of 2023, meaning economic data was disappointing relative to expectations. Unsurprisingly, the 10-year yield fell. However, the data has been better than expected since the start of 2024, as illustrated by the increasing CESI. In nearly synchronous fashion, the 10-year yield has risen along with the encouraging data.

Chart 1

Source: LSEG DataStream, Russell Investments. As of 4/1/2024.

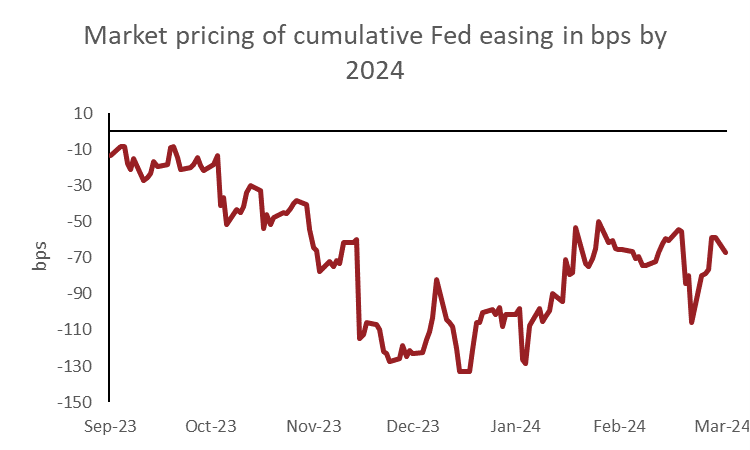

In turn, better-than-expected economic performance has caused a significant repricing of market expectations for the Fed’s interest rate path. Chart 2 shows that at the end of 2023, markets were pricing nearly 150 bps, or six 25-bps rate cuts by year-end of 2024. However, the resiliency of the U.S. economy has caused a shift in the outlook for rate cuts to around 50 bps of easing, or about two cuts, as of early April. Therefore, the move in yields is logical. Rising yields reflect the outperforming economy and the market's expectations for fewer interest rate cuts. To rephrase an old John Maynard Keynes saying, when the facts change, the markets adjust accordingly.

Chart 2

Source: LSEG DataStream, Russell Investments. As of 4/1/2024.

While that helps explain what has occurred over the past six months, the more important question is: what could be a probable path for Fed policy in the future and its impact on yields? As noted above, expectations are the Fed cuts about twice by year-end, with the first starting in July or September—this seems reasonable.

But wait, why should the Fed be easing if the economy is doing well? Wouldn't that put the broader disinflation trend at risk?

We don't think so.

Disinflation is likely to continue

While inflation this year has been slightly above expectations, the broader disinflation trend is intact. For instance, the Fed's preferred inflation gauge, the core personal consumption expenditures (PCE) price index, peaked at 5.6% year-over-year in 2022 and has declined to 2.8% as of February. In other words, significant progress has been made. While there will be bumps along the way, encouraging signals from forward-looking indicators for shelter—which has been a key contributor to the stickiness of inflation—and wage-sensitive components that influence prices indicate the core PCE index may be within the Fed's comfort zone of around 2.5% by year-end.

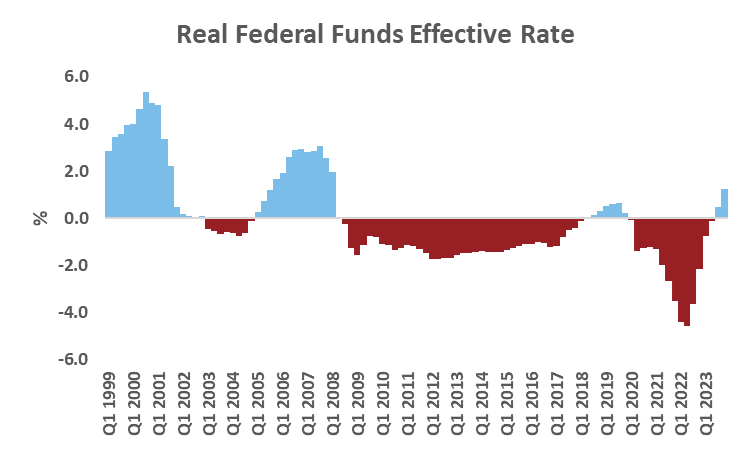

If our view on inflation is directionally correct, then it's also important to consider real rates. As much as we think about interest rates in nominal terms, arguably more critical for the economy are the level of real interest rates—that is, the nominal rate adjusted for inflation. Looking through this lens, Chart 3 shows that Fed’s target rate is the highest it’s been since prior to the Great Recession of 2008-09. Regional banks continue to face some stress, and auto and credit card delinquencies and bankruptcies are rising, indicating that the high rates are causing harm to certain parts of the economy. Therefore, if the Fed keeps its target rate unchanged and disinflation persists, real rates will continue to grind higher, culminating in unnecessary tightening and risking the chance of achieving the elusive soft landing.

Chart 3

Source: LSEG DataStream, Russell Investments. Real rate based on the difference between the effective Federal Funds target rate and four-quarter average of core-PCE. As of December 2023.

What’s the outlook for U.S. government bonds in the months ahead?

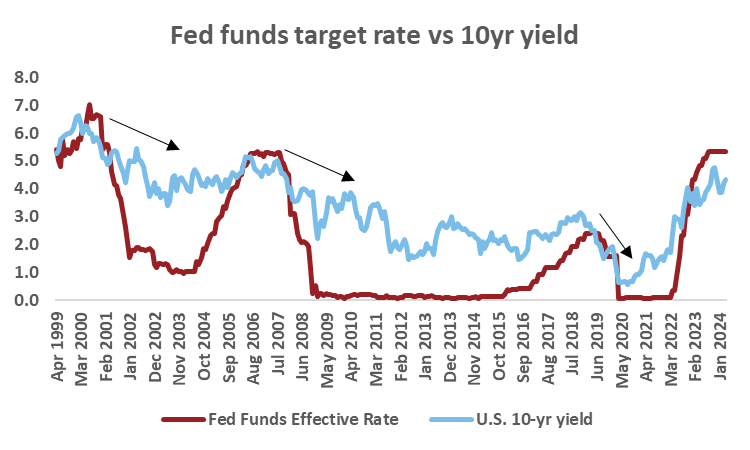

As noted in our second-quarter global outlook, the probability of achieving a soft landing has increased. However, that's predicated on the Fed cutting its policy rate later this year. We also expressed our positive outlook for government bonds, which would benefit in a recession that forces aggressive policy easing but also work in a soft-landing scenario. Chart 4 shows that Fed rate-cutting cycles coincide with falling 10-year yields.

The Fed's projections indicate that the long-run neutral rate, the target rate that is neither stimulative nor restrictive, is about 2.5%. The neutral rate is a heavily debated topic, and there are strong opinions with some arguing it could be higher. We believe it's slightly higher at 3%; nonetheless, even if it's slightly higher, the current federal funds effective rate of 5.3% is far from neutral. While the Fed won't be in a rush to cut to neutral, that is its likely direction of travel over time. Our probability-weighted fair value for the U.S. 10-year Treasury yield is approximately 3.9%, which is roughly 65 bps lower than the 4.5% level as of April 10, 2024. This, in turn, keeps our outlook positive towards government bonds.

Chart 4

Source: LSEG DataStream, Russell Investments. As of 4/1/2024.

The bottom line

Markets dynamically respond to shifts in economic data in real-time, but investors shouldn't be as reactive with their asset allocation. We believe proactively staying disciplined and diversified across multiple geographies and asset classes is how objectives are best achieved over the long term.

More By This Author:

Is U.S. Inflation Still Heading In The Right Direction?

1970s: U.S. Oil Crisis. 2020s: U.S. Net Oil Exporter. What's The Shift Mean For Energy Markets?

What’s The Outlook For U.S. Q1 Earnings Season?

Comments

Log in or sign up to join the conversation.