Image Source: Pexels

Global leading indicators remained robust heading into autumn, despite softening compared to levels at the start of the year. Uncertainty always lurks in financial markets, and currently, (at least) three major questions are weighing on investors—threatening the ongoing optimism in the global economy and financial markets:

- U.S. Trade Policy and Tariffs: Did the White House, back in April, effectively throw a boomerang that's now returning to hit both the U.S. and global economy in the face?

- Sustainability of the AI Investment Boom: Is the surge in tech and AI-exposed equities evidence of a genuine transformation, a bubble that is about to pop with predictably adverse consequences for markets and the economy.

- Global Bond Market Sell-Off: Investors are raising questions about long-term fiscal sustainability in the U.S., U.K., France, and Japan, even speculating about the erosion of monetary policy independence in the U.S. A crisis of confidence in one or more of these large bond markets could trigger turbulence across opaque, illiquid private credit markets, spilling over into the real economy.

Friday’s disappointing U.S. employment report has reignited fears that Mr. Trump’s trade strategy is less “3D chess” and more a spectacular economic goal, possibly pushing the U.S. into recession or, at minimum, a sharp slowdown. This would be negative for markets and the global economy.

However, the weak labor data also acts as a ‘bat signal’ to the Fed, prompting it to align with global peers by easing monetary policy. A rate cut is almost certain this month, with growing speculation about a 50 basis-point move to jumpstart momentum. This underscores the unusual dynamics of the current global policy cycle.

Historically, the Fed has led both tightening and easing phases. But this time, it has lagged, initially due to economic strength, and more recently, due to inflation risks from tariffs. Tariffs may still act as a stagflationary constraint on the Fed’s policy response—so U.S. inflation between now and year-end will be critical to watch—but for now, labor market weakness is driving the Fed toward a dovish pivot.

I still believe global leading indicators support a “glass half full” interpretation, though this could change quickly. The current expansion phase has lasted 16 months, which is a relatively long period based on the historical cyclical swings in global leading economic indicators, and both U.S. tariffs and bond market stress have the potential to derail it.

Still, from a traditional cyclical standpoint—where global activity lags monetary policy—the environment could hardly be better. The chart below illustrates that the global rate cycle is now as supportive for growth as it was during the peak of Covid-era stimulus. And that’s before the world’s largest central bank has even started easing.

Bullish, and the Fed is about to join the party.

Cyclical upturns don’t typically spontaneously combust. They’re usually ended by central banks tightening policy in response to inflation. Currently, global monetary policy is still riding the soft-landing wave, having eased from post-Covid peaks.

The key risk now is a resurgence in inflation, which would likely force central banks to pivot back toward tightening, and quickly, especially given an initial condition of elevated inflation. That’s the price of a soft landing.

(Click on image to enlarge)

Still expanding.

8 of 20 leading indicators were trending upward in August—down from 10 in July, but steady with May and June. This suggests a sustained, though weakening, upturn in global economic activity since early 2025. The upturn from the 2022 trough and subdued 2023 conditions remains intact—but further declines could signal a downturn.

Coincident indicators slipped further at the end of Q2, but remain strong overall. Global growth in industrial production and trade, based on CPB data, averaged 3.5% year-over-year in Q2, down slightly from 3.8% in Q1, which was boosted by tariff front-running in March. Leading indicators suggest continued strength through Q3 and into early Q4.

The three-year rolling Z-score of the global leading economic indicators—often a reliable early signal—improved further over the summer. It erased spring weakness (since revised) and is now re-accelerating from already high levels.

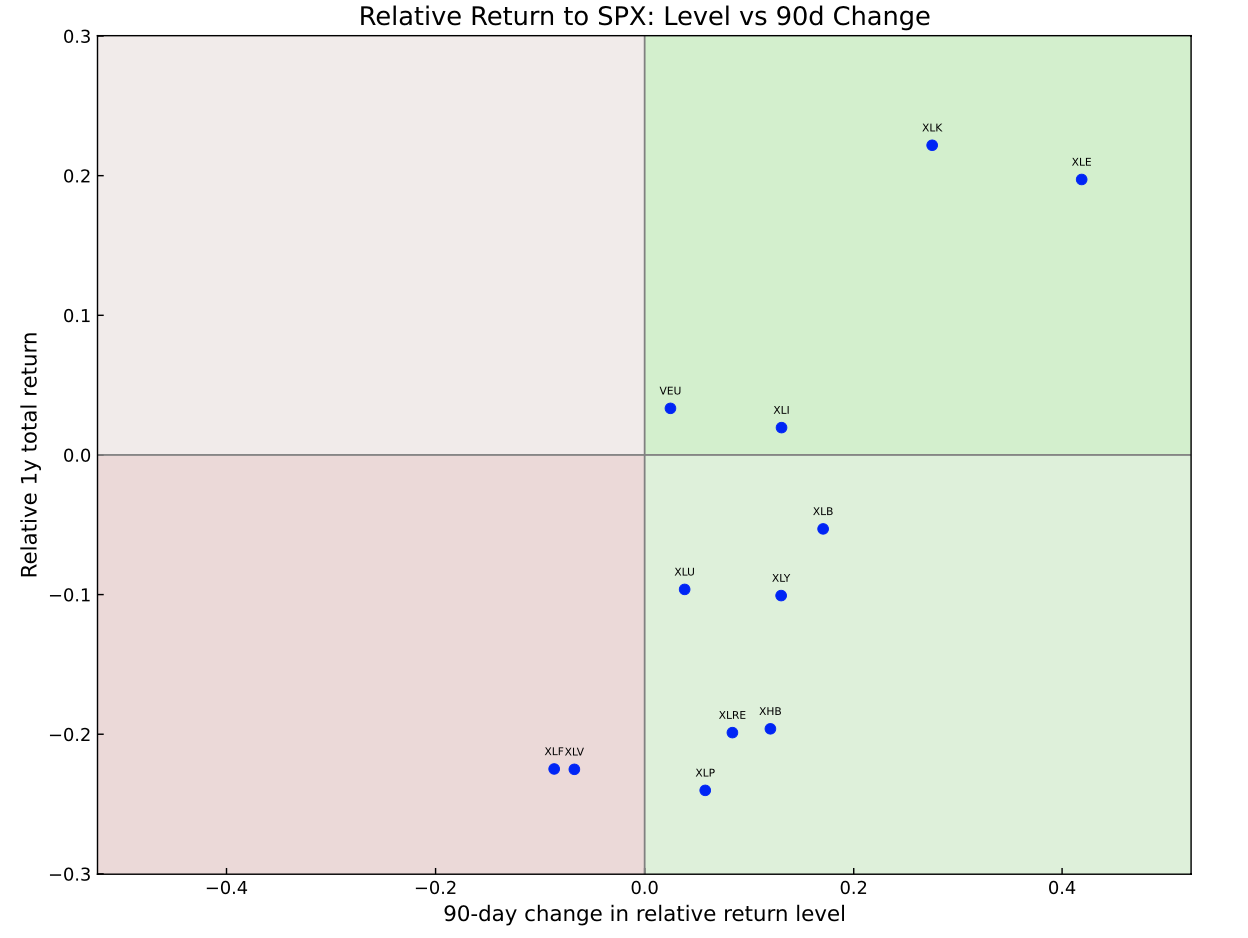

Equity markets have largely held their gains from the “Liberation Day” lows, but have wobbled recently on U.S. slowdown concerns. Still, the broader trend in leading indicators remains supportive for cyclically-exposed equities.

The first principal component (PC1) of global leading economic indicators remained in a downtrend in August. PC1 reflects common cyclical patterns across countries and typically peaks during synchronized downturns. Its current weakness implies divergence and hints at underlying resilience in the global economy.

Country-level data are starting to diverge based on August's data, though the core of the sample remains situated in the upper-right quadrant, with leading indicators above their long-run average and rising. Weakness in Asia is a surprising message from the August report, with leading economic indicators in China and Japan pushed towards the lower left—leading economic indicators below average and falling—joining Turkey.

Leading economic indicators in Spain, South Africa, and Brazil are above their long-run average, but with negative momentum. In the top-right, the U.K. stands out as a surprise, and positive, outlier, joined by Germany, Mexico, and South Korea.

Mexico is interesting, since its leading economic indicator has now completed a recovery, which I speculated about in May, when I noted that “Mexico stands out as the only country in the sample with strengthening positive momentum from a low base—typically the best setup for positive returns in cyclical asset.” The EWW ETF is pushing towards six-month highs as I type.

More By This Author:

Equity Sector Rotation Chartbook For August 2025 - Order Is Restored, For NowA Question Of Time

Things To Think About - Is AI Plateauing? And Monetising U.S. Hegemony

Comments

Log in or sign up to join the conversation.