We’ve Been Here Before – And It Ended With An Epic Crash

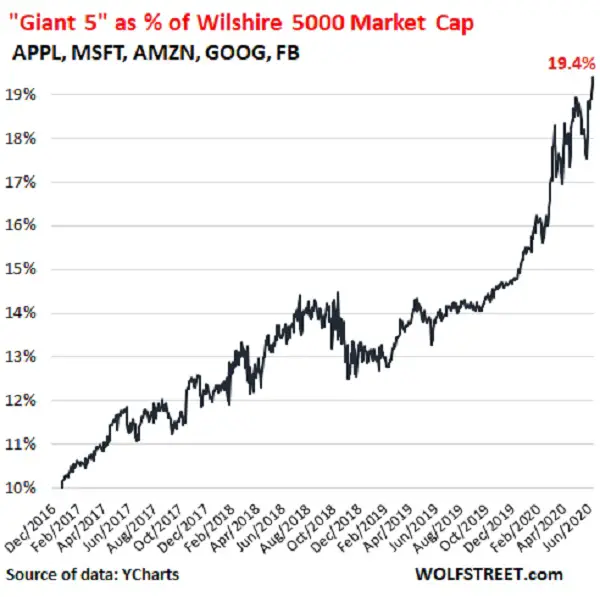

Wolf Richter yesterday published some charts that, for anyone with a sense of stock market history, are pretty ominous. It seems that the major market indexes that recently soared back to record highs are being elevated by an amazingly small number of stocks – Apple, Microsoft, Amazon, Google and Facebook to be specific — which he calls the “Giant 5.”These stocks now account for nearly one-fifth of the Wilshire 5000 stock index’s value:

That kind of dependence on just a handful of companies is intuitively scary. What’s even scarier is that we’ve been here before, and each time the result was ugly.

In the 1960s and early 1970s the US stock market was dominated by a group of large-cap stocks that took on a life of their own, elevating the market far beyond what it would have been without them. See if this Investopedia entry sounds familiar:

The Nifty 50 refers to the fifty most popular large-cap stocks that traded at high valuations in the 1960s and 1970s. They included household names such as Xerox (XRX), IBM, Polaroid and Coca-Cola (KO). Due to their proven growth records and continual increases in dividends, the Nifty Fifty were viewed as “one-decision” picks: investors were told to buy and never sell.

Many Nifty 50 stocks sported price-to-earnings (P/E) ratios as high as 100 times earnings. They propelled the bull market of the early 1970s, only to come crashing down in the 1973-74 bear market.

Then in the 1990s, a group of Big Tech stocks strikingly similar to today’s Giant 5 so dominated the market that they gained global significance:

From Bill Fleckenstein’s book Greenspan’s Bubbles:

In May 1999, former Fed Chair Paul Volcker told an audience, “The fate of the world economy is now totally dependent on the growth of the U.S. economy, which is dependent on the stock market, whose growth is dependent on about 50 stocks, half of which have never reported any earnings.”

Volcker saw the bubble. Greenspan missed it. Just a few weeks after Volcker’s speech, Greenspan testified before Congress, saying “Bubbles generally are perceptible only after the fact. To spot a bubble in advance requires a judgment that hundreds of thousands of informed investors have it all wrong. Betting against markets is usually precarious at best.” But the so-called “informed investors” were acting in response to Greenspan’s policy of lowering rates to help the financial markets.

In 2000, inevitably, the bubble popped. Minutes of FOMC meetings show that Greenspan was blind to the fact that the market had been racing up precisely because of his reckless monetary policy. The market crash ruined many naive speculators. Meanwhile, economic researchers began to take issue with Greenspan’s beloved productivity growth. One found that productivity had actually decreased during the late 1990s.

Here’s what happened to the Nasdaq index when that generation of Big Tech stocks returned to their intrinsic value in 2000:

Now back to the current variation on this theme, which Wolf Richter summarizes as follows:

This is how dependent the stock market, and broad portfolios reflecting it, have become on the “Giant 5.” It’s not that there aren’t a bunch of other companies that have gained as much or more than the “Giant 5” in percentage terms – there are – but in dollar terms, and in weight in the market, they just don’t measure up to these five giants.

Apple and Microsoft both are now worth over $1.5 trillion. Amazon is at nearly $1.4 trillion, Alphabet at $1.0 trillion. These are gigantic valuations. They also speak of an immense concentration of power in a single company.

Among the losers in that rest of the market are companies that used to be the largest in the US stock market, such as Exxon-Mobile, which since January 26, 2018, has lost 48% of its value. The entire and once vast oil-and-gas sector has gotten crushed.

The market, and broad portfolios, are immensely dependent on the Giant 5. That was great on the way up – on their way to becoming giants, when their share of the overall market doubled in three-and-a-half years, from 10% in January 2017 to nearly 20% today.

But if they sell off – there are myriad reasons why giants sell off, as all prior giants have found out – the impact of these five companies is going to be proportional to their giant size.

In general, I agree that the market has the potential to go down if another stimulus isn't passed soon. However, regarding FANG stocks I think there is a distinct separation between these stocks. Although Google and arguably Apple aren't too overvalued, especially given slow growth, no inflation, and low interest rates, other stocks like Facebook and Netflix are a bit rich for their implied growth to say the least.