↵

Image Source: Unsplash

Wall Street just sent a major signal, and most investors probably missed it.

This morning, two heavyweight firms, BNP Paribas and Morgan Stanley, downgraded key names in both the REIT and regional banking sectors.

BNP pulled the plug on the REIT complex (AVB, ESS, UDR, MAA, EQR), calling for Neutral or Underperform ratings.

Morgan Stanley downgraded M&T Bank (MTB), Wells Fargo (WFC), and U.S. Bancorp (USB), citing muted loan growth, valuation risk, and a murky macro backdrop.

To the average investor, this looks like just another reshuffling of analyst opinions.

But the move to downgrade both REITs and regional banks at the same time should send a tremor through the market, especially for anyone still holding onto the “Fed cuts mean buy the banks and real estate” playbook.

That’s where the trap lies.

This is Why “Things are Different” This Time

Historically, lower rates are a tailwind for both groups. Regional banks benefit from increased loan demand across mortgages, small business, and commercial real estate.

REITs see margin improvements as they refinance high-cost debt. But this time is different, and Wall Street clearly knows it.

Start with REITs.

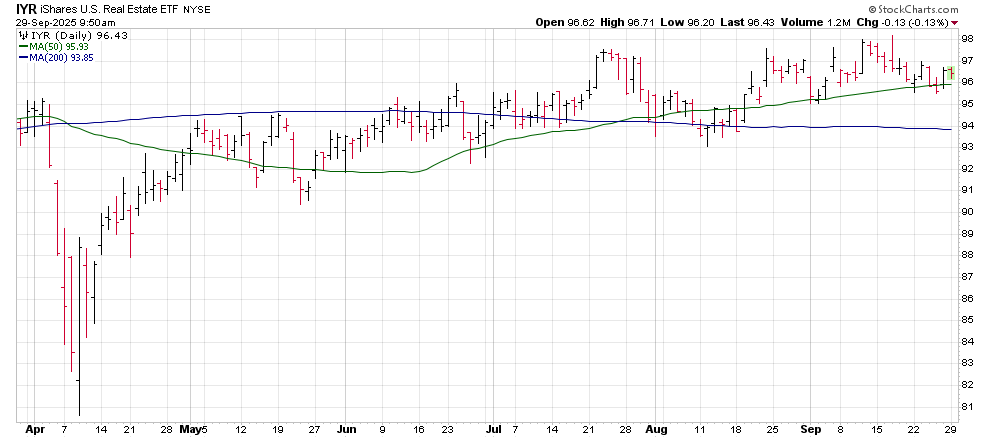

The iShares U.S. Real Estate ETF (IYR) has been dead money since May.

(Click on image to enlarge)

This is despite increasing confidence in a fourth-quarter Fed pivot. If rate cuts were all that mattered, REITs would be moving. They aren’t, because the underlying fundamentals are eroding.

Commercial real estate is structurally impaired.

Office buildings in major metro areas are still sitting half-empty. The “return to office” narrative never played out the way corporate America hoped.

Instead of expanding square footage, companies are downsizing and sharing space. That means lower occupancy, tighter margins, and less cash flow… the three pillars that support the REIT model are all under pressure.

On the residential side, nothing has been resolved.

Housing inventory remains depressed, prices are still elevated, and mortgage demand is soft.

Buyers are sidelined by affordability, not just rates. The 10-year and 30-year portions of the bond market remain elevated, and that's keeping long-term mortgage rates higher than expected, despite the Fed’s moves.

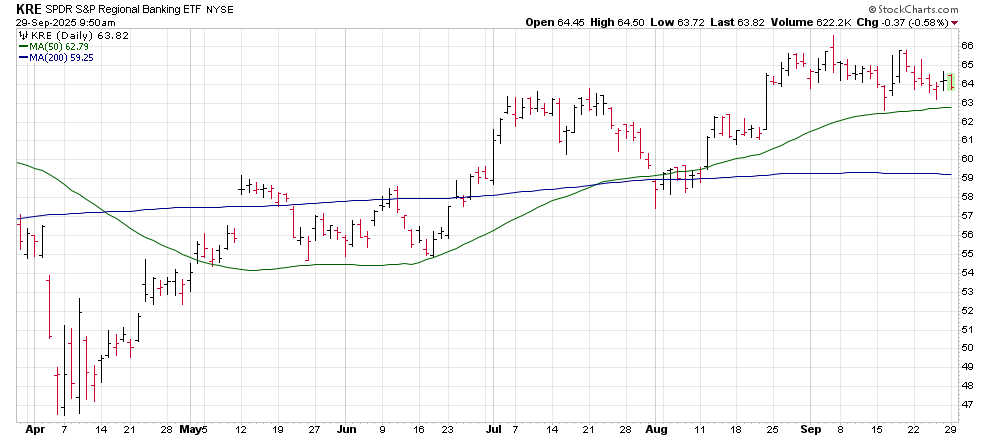

For the regional banks, that’s a direct hit.

These are the institutions most exposed to local real estate and small business lending. If credit demand doesn’t materialize, and existing loans start to sour under slower growth and sticky inflation, regional banks will face both top-line and balance sheet pressure.

(Click on image to enlarge)

Bottom line

The classic “buy the REITs and banks into a Fed cut” setup doesn’t work here. Not this cycle.

If you’re looking for opportunity in financials, skip the regionals.

Go upstream to the big names with trading desks and global exposure - Goldman Sachs (GS), Citigroup (C), Morgan Stanley (MS). These banks are able to “trade” their way through these interest rate quagmires and hold less loan risk.

You’ll notice Wells Fargo (WFC) didn’t make that list.That’s because WFC it still carries major exposure to mortgage origination.

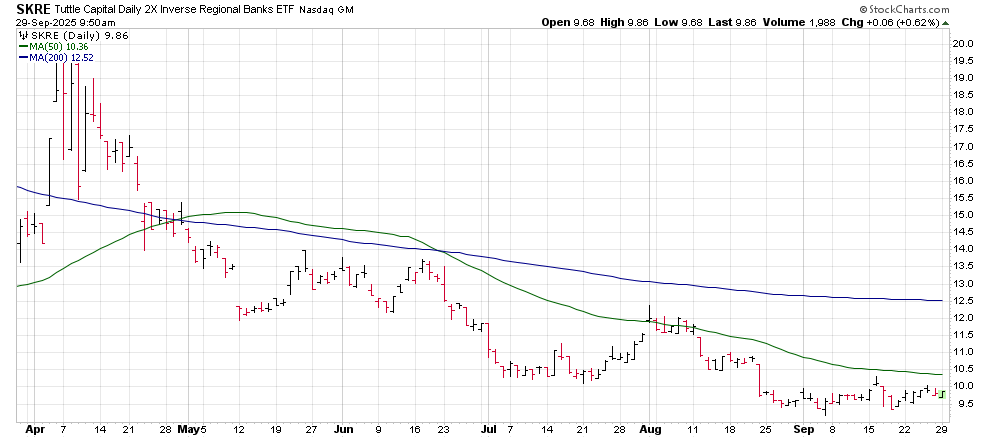

How to Trade the Regional Bank Weakness

And if you’re looking to trade the downside in regionals, the Tuttle Capital Daily 2X Inverse Regional Banks ETF (SKRE) is your tactical tool.

This ETN delivers 2x the inverse daily move of KRE. Just remember, this is a short-term trade, not a long-term hold. Use it with discipline and with clear downside targets in mind.

(Click on image to enlarge)

More By This Author:

Costco Beats Earnings But COST Stock Falls: Is This A Warning Or An Opportunity?

Palantir Stock Is Down Again: Is This A Discount Or A Bull Trap?

Today's Market Movers: Tariffs, TikTok, And Oil

Comments

Log in or sign up to join the conversation.