I just refreshed my favorite U.S. breakeven inflation chart (below), and I was surprised by how placid pricing has been. This article gives a few observations regarding the implications of TIPS pricing.

Background note: the breakeven inflation rate is the inflation rate that results in an inflation-linked bond — TIPS in the U.S. market — having the same total return as a conventional bond. If we assume that there are no risk premia, then it can be interpreted as “what the market is pricing in for inflation.” I have a free online primer here, as well as a book on the subject.

(As an aside, I often run into people who argue that “breakeven inflation has nothing to do with inflation/inflation forecasts.” I discuss this topic in greater depth in my book, but the premise that inflation break-evens have nothing to do with inflation only makes sense from a very short term trading perspective — long-term valuation is based on the breakeven rate versus realized inflation.)

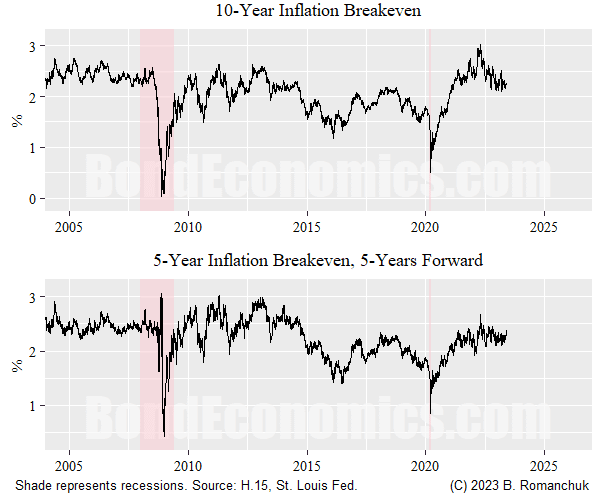

The top panel shows the 10-year breakeven inflation rate. Although it scooted upwards after the pandemic, it is below where is was pre-Financial Crisis, and roughly in line with the immediate post-crisis period. (Break-evens fell at the end of the 2010s due to persistent misses of the inflation target to the downside.) Despite all the barrels of virtual ink being dumped on the topic of inflation, there is pretty much no inflation risk premium in pricing.

The bottom panel shows forward breakeven inflation: the 5-year rate starting 5 years in the future. (The 10-year breakeven inflation rate is (roughly) the average of the 5-year spot rate — not shown — and that forward rate.) It is actually lower than its “usual” level pre-2014, and did not really budge after recovering from its post-recession dip. (My uninformed guess is that the forward rate was depressed because inflation bulls bid up the front break-evens — because they were the most affected by an inflation shock — while inflation bears would have focused more on long-dated break-evens, with the forward being mechanically depressed as a result.)

Since I am not offering investment advice, all I can observe is the following.

-

Since it looks like one would need a magnifying glass to find an inflation risk premium, TIPS do seem like a “non-expensive” inflation hedge. (I use “non-expensive” since they do not look cheap.) Might be less painful than short duration positions (if one were inclined to do that).

-

Breakeven volatility is way more boring than I would have expected based on the recent movements in inflation. The undershoot during the recession was not too surprising given negative oil prices and expectations of another lost decade, but the response to the inflation spike was restrained.

-

The “message for the economy” is that market pricing suggests that either inflation reverts on its own, or the Fed is expected to break something bigger than a few hapless regional banks if inflation does not in fact revert.

More By This Author:

Degrowth Versus SustainabilityWill The Fed Keep Reacting With A Lag To Lagging Data?

Another Bank Bites The Dust

Comments

Log in or sign up to join the conversation.