The Financial Times reports that the yield curve inverted, albeit by just 1 basis point:

Uh oh

Does this mean a recession is more likely than before?

Yes.

Does this mean that a recession is likely in the next 12 months?

Probably not.

Does this mean that monetary policy is too tight?

Hard to say.

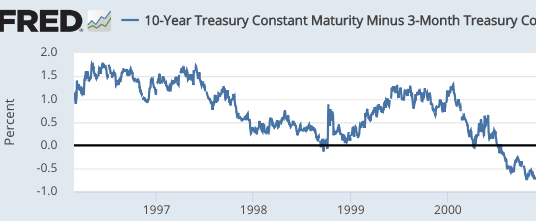

In my view, the current situation reminds me most closely of 1998, when the US economy was pretty strong at a time when the global economy was weakening. That year also saw a mild inversion, which turned out to be an incorrect recession forecast:

Ah, more reassuring

In its entire history, the US has never experienced a soft landing, in the sense of having a recovery extend for many years after unemployment had fallen close to the natural rate. Since unemployment has fallen close to the natural rate, that fact alone should make us worried. On the other hand:

1. Australia and the UK have experienced soft landings in recent decades.

2. In previous US expansions, you didn’t have MMs beating the drum for stable NGDP growth, level targeting. (Yes, I’m joking.)

When unemployment falls to the natural rate, problems are almost always just around the corner. In 1966, the yield curve inverted when unemployment fell below 4%, and again there was no recession. But there was a problem just around the corner—high inflation.

So low unemployment is a very dangerous time for the US. We are a clumsy country, which fails to achieve soft landings. That’s the real story here, which is even deeper that the “inverted yield curve means recession” story. Low unemployment and inverted yield curves are a warning of choppy waters ahead, of monetary policy in danger of drifting off course, one way or another.

In my view, the stock market decline at the end of 2018 was partly due to a perception that rates should not be increased, while the Fed was planning another set of rate increases in 2019. (Other worries such as trade, global growth, etc., also played a role).

When the Fed backed off, stocks rallied. Despite today’s sell-off, stocks are at very lofty levels and hence stock market investors likely don’t foresee a recession during the next 12 months. Neither do I. But it would be foolish to deny that the recent yield curve inversion makes a recession more likely than before, say a 25% risk rather than a 15% risk.

Comments

Log in or sign up to join the conversation.