The S&P 500 In Week 1 Of July 2016

There really wasn't much of note to comment about in the first full week of July 2016, at least, until Friday, 8 July 2016, when something interesting happened. Let's flip the order that we normally recap the previous week's action for the S&P 500 and review the more significant headlines from the Week 1 of July 2016.

Tuesday, 5 July 2016

- Wall Street skids as global growth worries resurface

- Fed's Williams says Brexit effect as expected, no big deal

- Economic growth worries, oil slump drag Wall St. lower

Wednesday, 6 July 2016

- Fed's Tarullo says no rate hikes needed until inflation is more solid

- Fed minutes suggest rate hikes on hold until Brexit impact clearer

- Wall Street ends up on cautious U.S. rate outlook

Thursday, 7 July 2016

- World stocks rise, but Wall St. dips with oil ahead of jobs report

- Energy weighs on Wall St. but Costco shines

Friday, 8 July 2016

- Oil edges up but biggest weekly drop in Brent since January

- S&P 500 ends just shy of record high close

- Hilsenrath Analysis: June Jobs Report Raises Chances of Fed Rate Increase in September -

- Divided Wall St. clings to view of one 2016 rate hike after jobs data: poll

The last two headlines represent something of a dueling narrative with respect to the prospects of a Fed rate hike, where we can use our futures-based model of how stock prices work to see which narrative won the week.

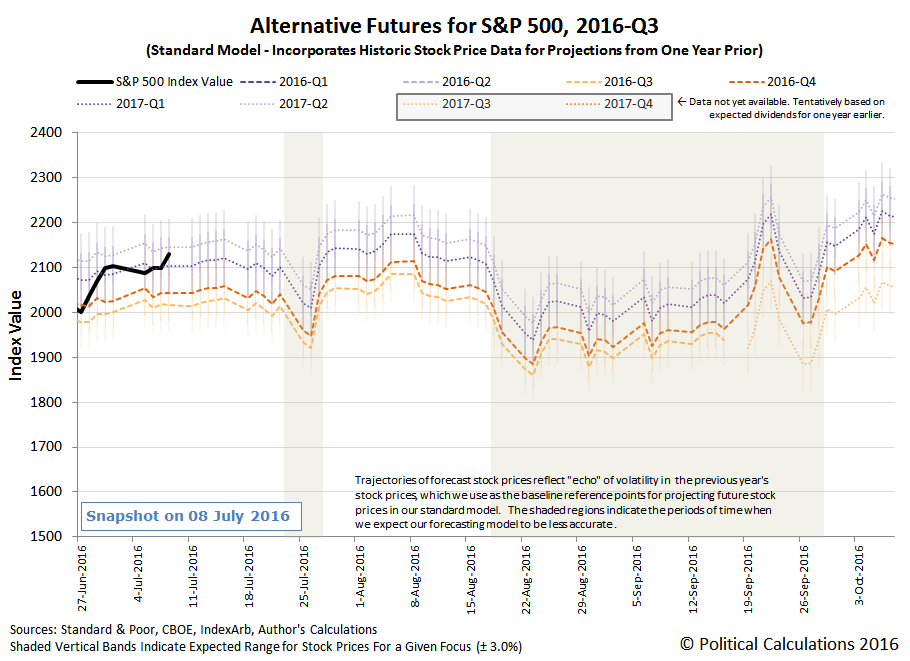

Here's how that will work. Going into Friday, 8 July 2016, and actually since the latter part of Week 5 of June 2016, our model was indicating that investors were collectively focusing on 2017-Q1 in setting their expectations for the future of stock prices. If Hilsenrath's analysis is correct, and investors start anticipating that the Fed has become more likely to hike short term interest rates in September 2016, we should see the level of the S&P 500 move toward a level consistent with investors focusing on 2016-Q3 - the future quarter in which the action will be taken.

But, if investors don't anticipate such a move, as indicated by Reuters' polling, they should either continue focusing on the expectations associated with 2017-Q1 as they make their current day investment decisions or shift their forward-looking focus to a more distant future, like 2017-Q2, in the case where they don't anticipate any such action will take place in the near term.

Our alternative futures chart for the S&P 500 reveals the answer of which narrative carried more weight with investors on Friday, 8 July 2016.

(Click on image to enlarge)

The clear answer is that they shifted their attention toward the more distant future of 2017-Q2, suggesting that they do not anticipate the Fed doing anything to increase U.S. interest rates before that time.

That can change, as the random onset of news events might cause investors to shift their attention back toward the nearer term, which at its current level, would suggest the potential for the S&P 500 to fall in such a case. For that matter, the market might respond to a speculative noise event, either positive or negative, that could send prices in the corresponding direction with respect their current level, if only for a short period of time.

A third possibility would involve a fundamental change in the expectations for future dividends, which would alter the alternative trajectories our model projects. With 2016-Q3 earnings season getting underway on Monday, that's a market shaping factor that cannot be discounted.

Right now however, the chart above is also showing the pending headache that we're going to have to cope with this quarter. Because our futures-based model incorporates historic stock prices, the echoes of past volatility can affect its ability to accurately project the levels where stock prices will be in the future, which we've shown as the shaded regions in the chart. Those regions coincide with the one-month anniversary of the Brexit noise event, and later in the quarter, with the aftershock of the one-year anniversary of China's stock market meltdown from August 2015.

We have developed a way to deal with the echoes of that past volatility in our model, which we would do by rebaselining the historic stock prices we use to a different period of time - one that doesn't share the same level of volatility.

The challenge we have now is how best to do that. Last year, we used data from 2013 to work around the problem that the historic volatility that occurred in 2014 created for our model's accuracy, but we wonder if there isn't a better, less specific-time dependent way to approach the problem.

We've come up with a new outline for dealing with the echo effect that we're considering taking for a public test drive throughout much of this quarter. We don't know how well it might work, or even if it will work. Right now, all we know for sure is that we have just a few weeks to put a working solution together before it becomes necessary.

It's going to be a fun quarter!

Disclosure: None.

Thanks sir