The Soaring Risk Of Flying In Bernanke’s Helicopter

“Although the term ‘helicopter money’ is very frequently used in economics, it is doubtful whether such a policy will bring the results people really want. The following example shows why.

Let us assume that the Bank of Japan one day mailed 1 million yen in new bank notes to every Japanese citizen. The person who finds 1 million in his mailbox will probably feel very happy at that moment, because he things he is richer by that amount. The problem is what happens next.

When the person finds out that every Japanese person has also received 1 million, he would turn pale. Because at that instant he would realize that what he can buy with that amount has just shrunk dramatically.” – Balance Sheet Recession: Japan’s Struggle with Uncharted Economics and its Global Implications (2003) Dr. Richard Koo, page 55

This week, the helicopters descended on global markets, helping push the Dow and S&P 500 to another all time high as July monthly options come to a close this Friday. No need to deleverage just yet…right? Pile into risk on trades; central bankers have your backs.

“Something Big” Indeed Came – Bernanke’s Japan Visit Unveils “Helicopter Money”, Sparks Monster Rally, Zero Hedge, July 11, 2016

Helicopter Money ‘The Next Step’ in Monetary Policy Says Fed Official Loretta Mester, ABC News Australia, July 12, 2016

So let’s compare comments made this week in the press regarding Bernanke’s actual visit with members of the Bank of Japan and Prime Minister Shinzo Abe, comments that stem from ideas Bernanke discussed on his blog at the Brookings Institute 3 months ago.

Here is What Ben Bernanke Told the Bank of Japan, ZH, July 12 ‘16

“Mr. Bernanke visited Tokyo at a time of intense speculation that Mr. Abe may resort to so-called ‘helicopter money’, a radical form of monetary easing advocated by the former Fed chief. The strategy involves a central bank directly financing government spending or tax cuts. Japan once implemented the measure in the 1930s-40s and ended up stoking sky-high inflation.”

What Tools Does the Fed Have Left? Part 3: Helicopter Money: Bernanke Blog at the Brookings Institutes, posted on April 11, 2016

“Some have suggested an alternative approach in which the central bank prints money and gives it away—so-called “people’s QE.” From a purely economic perspective, people’s QE would indeed be equivalent to a money-financed tax cut (Friedman’s original helicopter drop, although perhaps more targeted). The problem with this policy, which would certainly be illegal in most or all jurisdictions, is not its economic logic but its political legitimacy: The distribution of what are effectively tax rebates should be subject to legislative approval, not determined unilaterally by the central bank.”

Since the bell was rung on June 24th , the day after the Brexit vote was counted the night before, the FTSE 100 dropped 592 points or 9.2% in under a day, but then over the last 13 days racked up 929 points for a 16% gain. A sign that all is well, or a big rally before the next wave of selling?

Clearly, the “helicopter money” headlines that started this week were after a 2-week rally in US and European stocks.

The reason was clear. Japanese stocks were close to a critical line, and needed a rally to help hold up equity markets as we came through July monthly options week. So in three days, we have a 1338-point rally, producing a gain of 8.8%.

If we then include the fact that the S&P 500 broke its May 2015 all time high on Monday the 11th, and the Dow did the same on Tuesday, May 12th, while the last 3 weeks have produced the lowest yields in centuries in the US and Britain, then it is clear that something is very wrong with the view of “helicopter money is part of our unlimited tool chest” being espoused by Bernanke, Mester, and other socialist central planners.

Only a fool would believe that given enough intervention by central banks stock prices need never deflate again. The 6,000-point drop between June 2015 high and June 2016 low in the Nikkei make that painfully clear.

Only a delusional nut would believe that interest rates could be suppressed indefinitely merely by bringing out more central planning schemes.

¥ 10 Trillion Versus ¥ 135 Trillion

Let’s focus on Japan, and run through a recent article, an article released in April 2013, and a chart of how well “conquering deflation” with massive intervention and debt has worked since 2013 when Japanese leaders launched the largest “stimulus” measures in the nation’s history.

First, the “helicopter” rally that shot the Nikkei up almost 9% in the last 3 trading days is based on a ¥10 trillion stimulus package announced by newly reelected Prime Minister Shinzo Abe.

Abe Orders Drafting of New Stimulus Package to Breathe Life into Japan’s Economy, The Japan Times, July 12 ‘16

“Prime Minister Shinzo Abe ordered economic revitalization minister Nobuteru Ishihara on Tuesday to draft a range of economic measures to bust deflation and raise Japan’s growth potential, including with a supplementary budget for fiscal 2016.

On Tuesday, the Nikkei financial newspaper reported the projects are likely to be worth about ¥10 trillion ($100 billion), including the supplementary budget and government-backed loans to businesses.”

Now journey with me back to April 2013 when the financial world was hit with THE largest QE plan to “defeat deflation” on record. Since January 1990 was the last time the Nikkei produced an all time high, the Japanese culture that deflation is a very real term.

Bank of Japan Unleashes World’s Biggest Burst Of Stimulus in $1.4 trillion (¥ 130 trillion) Shock Therapy, Financial Post, April 4, 2013

“New Governor Haruhiko Kuroda committed the BOJ to open-ended asset buying and said the monetary base would nearly double to 270 trillion yen ($2.9 trillion) by the end of 2014 in a shock therapy to end two decades of stagnation.

‘We took all available steps we can think of. I’m confident that all necessary measures to achieve 2% inflation in two years were taken today,’ he said….”

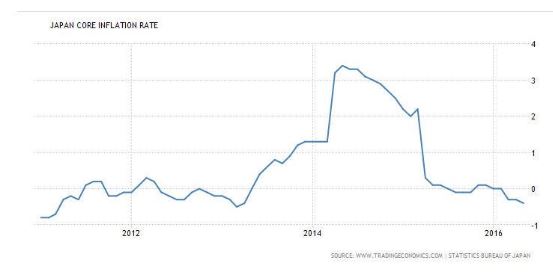

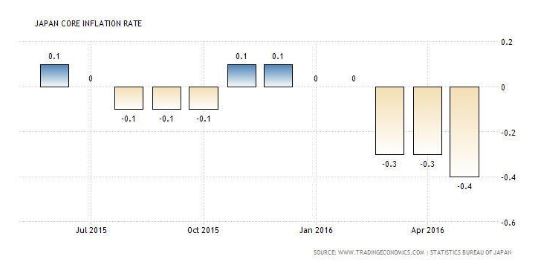

Now we leap forward to July 2016, and look at what impact the mega stimulus from 2013 has had on core inflation in Japan.

As we can see, the 2% inflation target was reached as Japan entered 2014, but by 2015 core inflation was back at zero. As we can see below, the nation is back in price deflation this year, and this after the largest “print money, buy up stocks and government bonds” scheme in world history. If we look back to the start of this article, we can see that the Nikkei dropped over 6,000 points between its June 2015 high and its June 2016 low. Clearly, asset inflation has failed miserably over the last year.

Will printing up less than 10% of what was printed up as Japan came through 2013 and 2014 solve the problems that the mega stimulus announced in April 2013 failed to do, when looking at core inflation over the last 5 years, negative rates on government bonds that began this year, or the Nikkei’s steep decline since its 18 year high last summer?

The Last Buyer At The Top

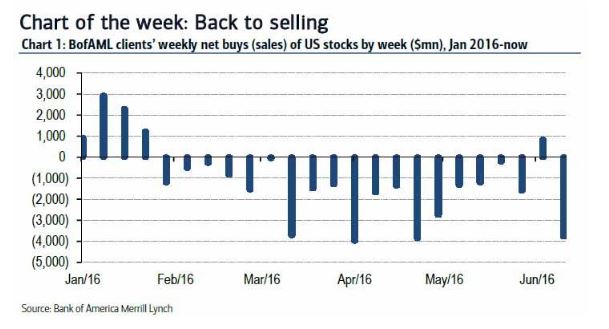

As of July 8th, we know from Lipper Fund Research that US stock based funds had seen 17 weeks of net outflows. This means the trend of net outflows by retail investors had taken place since March 11th.

We know as of June 14th, research by BofA Merrill Lynch reveals that institutional clients were sellers for 20 of the last 21 weeks. This trend would have started the week ending February 19th.

So who decided to DIVE IN since the collapse in global equity markets on June 24th and 27th, and buy, buy, buy! Anyone watching this drama for the last few years will not be surprised by the answer.

Disclaimer: Be a Contrarian, Remember Your History. Bulls become bears, and ...

more

Great read.

Thank you Danielle.

It is sad we have to compare the US to Japan's failed run down the tube of managed economy failure. How have we gotten here. There will be a difference though. We may get inflation, but without growth which may make our experience a lot worse, but hopefully bad enough to stop from going as far as Japan has gone.

Moon. Unless govenments stand up to these global central banks, which they have no track record of doing as a group, then the banks own the nations. Just my two cents. Sure wish it were different.

I share your sentiments.

Thanks David.

Call me a delusional nut. I know you don't mean it, Doug!

I believe there is massive demand for bonds for use as collateral in the new clearing houses for derivatives. If anything, that demand would possibly interfere with the use of helicopter money and NGDP targeting as rates could stay low anyway. After all, the Fed has to protect the collateral from being destroyed by higher rates!

But think about it, real helicopter money would not expand the balance sheet so far out of whack as it is now, and governments would collect more taxes. That would ultimately help the Fed's balance sheet in good times. In bad times, with rates going toward zero, bolstered by demand for bonds, the Fed's balance sheet could grow and it would not be a problem at all. The Lonergan plan does not make every citizen a millionaire, but is more responsible than asset buying, or all nations doing QE at the same time. Lonergan's plan acknowledges that government debt is worse than helicopter money, as properly defined.

The type of helicopter money that Japan could use is to buy Japanese debt, and set the interest rate to zero. That would be a form of helicopter money, but only for the government. The government could then stimulate the economy while debt fades away. That could help. But it isn't as good as Lonergan's plan, IMO.

One thing we know, we are headed to negative bond rates forever if something isn't done. And so call me a nut, but something needs to be done. The alternative is even more nutty, or is it nuttier?

I think all forms of helicopter money are illegal in Japan, so I think this is mostly talk. But laws can be changed.

Gary. I know that we are stuck with central banks pushing us more and more toward the global cliff. Over decades we have embraced the idea of "more debt and faster" as the solution to the latest debt crisis. All we are doing is training each generation that unlimited debt and state intervention is the only way out. That is why we are in the monumental mess we are in.Just my two cents as we watch so many first in history events, and the vast majority of the public totally clueless how much is taking place that the "expert" central planners have never seen before either. Frankly, financial socialism was never a theory I have supported.

I wouldn't call Friedman a socialist. But, I do think central banks rarely do any sort of stimulus for the people. They do it for the wealthy. But that creates dangerous imbalances. That is why I hope they do stimulus for the masses, not UBI, but a one time helicopter money that somewhat expands the balance sheet with no government bonds involved. There are not enough of them anyway.

Gary, I am not calling# Friedman a socialist, but there are direct links between writings of #Keynes and #Marx. Deficit spending was taken from Das Capital. I agree that that #QE has done little to nothing for fueling the trillions created into developing opportunities for jobs and sustainable growth across the entire economy. Instead it has fueled the greatest gap between the highest levels of wealth and the lowest levels of poverty. This is clearly not a successful model. As long as the power to fix the problem is concentrated in the hands of less than a half dozen central banks owned by the global investment banks, I don't see how we are headed in the right direction. Wish I say commitment to the people, but I haven't and don't see it today.

Keynes says spend through government #debt. #Friedman and #Lonergan say pay base money one time to expand the money supply. I think that is more responsible than any government debt expansion. JMO, Doug.

Gary. The track record of central banks has never been a "one and done". These organizations have come to believe there IS nothing that will stop them from printing up more money "when needed".

Sterilized money is all they print. So, they could be hindering the economy. I think they want to hinder any prosperity, because they, again want to protect the collateral, and keep yields low. You watch, slow growth is the new normal and so is massive demand for bonds as collateral.