The Smartest Guy In The Oil E&P Room?

Einhorn's E&P Shorts

David Einhorn slammed a handful of oil frackers" a year ago and laid out his short thesis during the annual Sohn\ Investment Conference in New York. At the time, we did not agree with all of Eihnorn's E&P short picks (assuming Einhorn's short picks include the companies he highlighted in his presentation).

Out of the five companies Einhorn mentioned in his presentation, four of them -- EOG, CLR, PXD, CXO -- are considered to be the best-in-class onshore E&Ps expected to survive this oil down turn. That is, if these four go under, the real Oil Shale Lehman Moment will surely emerge. Whiting Petroleum (WLL) is the only exception with weak balance sheet and asset portfolio. WLL stock is down 72% from a year ago, whereas the other 4 stocks of Einhorn's E&P shorts have held up pretty well. CLR and CXO was up 18% and 11% respectively from a year ago, while PXD and EOG had relatively minor losses of 14% and 2% respectively.

So Eihnorn does not look like the smartest guy in the E&P room.

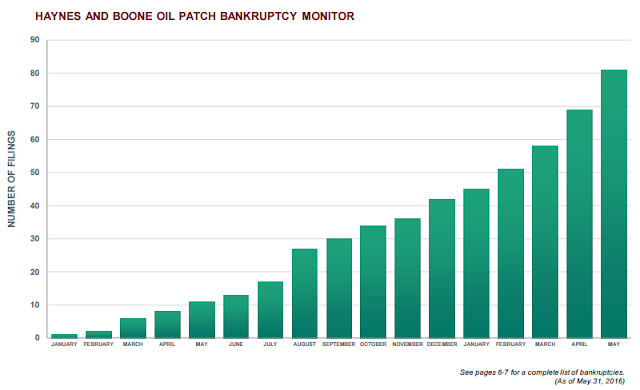

E&P Bankruptcy Spree: 77 and Counting

The oil price crash that started in the second half of 2014 has claimed many E&P victims.According to Haynesboone.com, there are 77 E&P bankruptcies from 2015 to May 2016 and over half of the filed chapter 11's are in Texas. We did warn several months ago that more pain to come in the over-saturated oil E&P sector. There are 110+ publicly traded E&P companies in North America, not counting the integrated major like ExxonMobile (XOM), Chevron (CVX), etc., and not all are healthy enough to survive an oil crash like this.

Noble/Rosetta Deal Was Not "the First of Many" Oil M&As

People were expecting an oil upstream M&A spree where the strong scoop up the weaker competitors at a steep discount. Noble Energy (NBL) did announce a $2.1 B deal in May 2015 to acquire Rosetta Resources (ROSE), a mid-cap onshore E&P with assets in Eagle Ford and Permian basin. This marks the first time since the oil collapse began in October 2014 that a major U.S. oil and gas producer snapped up another company. The Noble/Rosetta deal was a non-cash all-stock transaction where Noble would take on $1.8 Bn debt from Rosetta and valued Rosetta stocks at $26.62 a share.

I remember at the time there were people thinking Rosetta sold itself too quick and too cheap (Rosetta stock 52-week high was $54). Most people, at the time, were not expecting this kind of 'lower for longer" oil price scenario. Bloomberg proclaimed "This $2.1 Billion Shale Deal Will Be the First of Many", and many believe there could be more M&As to follow after Noble/Rosetta deal, but that did not happen.

Mid and Small Cap Shale Players Keep Pumping for Cashflow

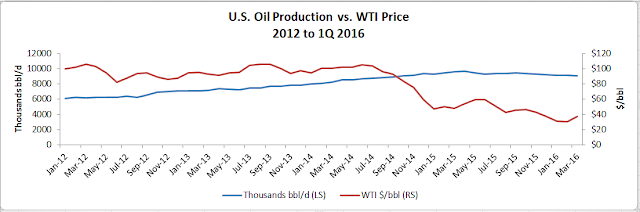

One thing peculiar about the current E&P bloodbath is that oil production in the U.S. has held up well compared to the much more drastic downturn of oil prices. One major reason for this is U.S. has too many small oil producers that need to pump for the cashflow to meet payroll and vendor obligations. This production-to-meet-cashflow-needs by smaller shale players actually has prolonged this oil crash and put a stop to potential sizable buyout in the oil upstream. Most Oil M&A's so far have mainly focused on selective asset acquisitions to enhance existing portfolio.

Meanwhile, with no suitable buyers willing to take on the risk, many of Rosetta's mid-cap peers who kept on producing and hung in there were dropping like flies -- Quicksilver (KWK), Magnum Hunter (MHR), Swift Energy (SFY), Energy XXI (EEXXF), Goodrich Petroleum (GDP), Ultra Petroleum (UPL), Lynn Energy, etc. all went into Chapter 11. Actually, Rosetta could face bankruptcy itself eventually if not for the Noble Energy deal.

Who's the Smart Shale Oil Player?

Low oil prices negatively impacted every E&P including Rosetta's leverage and balance sheet. In addition, Rosetta was also suffering from lower reserves and production prospect than other comparable mid-cap E&Ps. So Rosetta made a swift decision to grab the Noble Energy offer salvaging the best what the company had left before heading into bankruptcy itself.

Hindsight is 20/20, Noble Energy is probably kicking itself right now as it could have picked up Rosetta much cheaper, while Rosetta's Board and executives with golden parachutes are laughing all the way to the bank.

From this perspective, Rosetta did not sell itself too quick or too cheap, and could be at least one of the smartest guys in the E&P sector.

350,000 Energy Jobs Lost Worldwide

WSJ reported that during this worst oil bust in a generation, more than 350,000 lost energy jobs world-wide. About 90,000 of those layoffs have been in the U.S. and 40,000 in Canada. In May, the Texas Alliance of Energy Producers said Texas has seen 84,000 oil-industry layoffs.

The newly released June payroll report showed the number of people employed in "oil and gas extraction" hit its lowest level in five years. Bloomberg concluded that

"...at this point, the best hope for oil and gas workers at risk of losing their jobs is that America continues to hire outside of their ranks."

Surviving E&Ps Still Face Headwinds

Meanwhile, oil and gas debt offerings are drying up as investors look to de-risk and operators look to de-lever. According to WoodMac, the E&P bankruptcies have killed U.S. production of 1 million boe/d, or 6% of U.S. production, and taken $52 billion worth of debt (or asset valuation) off the market, that's 12% of total US E&P sector debt.

Wallstreet right now is unwilling to finance new E&P debt because of risk concerns, while E&P companies are also unwilling offer new debt because of leverage concerns, . Both equate to headwinds for the companies that actually escape bankruptcy. As WoodMac put it, "It could take years to right-size some balance sheets....." after the debt gluttony during the oil price bull cycle in the past 15 years or so.

Disclaimer: All of the content on EconMatters is provided without assurance or warranty of any kind. The opinions expressed here are personal views only, and ...

more

Not to say that Einhorn doesn't know what he is talking about, but he did highlight some names that will be around for a very long time. He was right, just incorrect about how big the "fallout" would be. At least he swung for for the fence.