Gold is on the move as quantitative easing sweeps the world.

After calendar year 2014 brought the spot price of gold a 1.79 percent decline to $1,183.20 per ounce on the Chicago Mercantile Exchange, gold has started 2015 with a strong rally

Gold’s big problem throughout 2014 was the Federal Reserve’s move to taper its way out of the quantitative easing program. The weakness of the dollar which resulted from quantitative easing sent gold prices to their record highs during August of 2011. As the taper strengthened the dollar, gold prices fell.

The New Year has brought renewed fears of a European sovereign debt crisis with deflation in Europe and uncertainty over the future of Greece in the Euro Zone. By January 21, the six-month chart for the spot price of gold was wonderfully bullish, with a giant, inverse head-and-shoulders pattern as its most-striking feature.

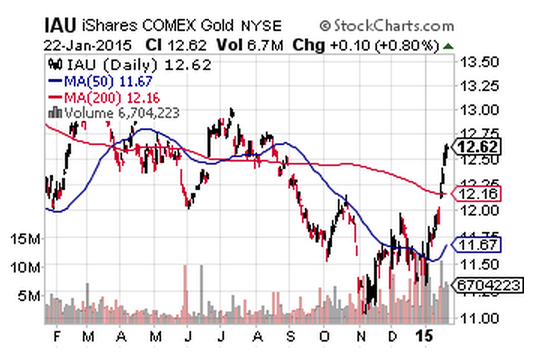

For ETF investors, iShares Gold Trust offers a look at the market and a way for gold bulls to invest.

In the chart we can see that the 50 day moving average is on the upswing and that the price has crossed above both the 50 and 200 day moving averages.

Other factors for gold’s renewed strength have included the plunge in oil prices. Although the price of gold usually declines with that of oil (because they are both commodities) a prolonged fall in oil prices can boost the “safe haven” appeal of gold, due to deflationary economic consequences of weak oil prices.

With deflation now a reality in Europe, the European Central Bank is feeling more pressure to provide an effective monetary stimulus regimen. On January 7, Eurostat reported that the annual inflation rate for the Eurozone in the month of December was negative 0.2 percent. As a result, the Eurozone economy has deteriorated from a state of disinflation to deflation.

The situation in Europe now has the European Central Bank following Ben Bernanke’s playbook and undertaking a quantitative easing program. Because the dollar weakness, resulting from America’s quantitative easing effort, increased the price of gold, the question arises as to what will happen to gold prices during an ECB-led quantitative easing program. Because the ECB plan would weaken the euro, the dollar would gain strength. This could be bearish for gold because gold prices are measured in dollars. An alternative scenario would involve a reinforcement of gold’s “safe haven” status, because of euro weakness and persistent doubts about whether an ECB-led QE program might actually become a fiasco.

Another wild card will be the state of the global economy. As we saw in the United States, quantitative easing can send the stock market higher, while the real economy doesn’t fare as well. The global economic slowdown could persist, regardless of what the ECB does for the European stock markets, and in that case, the demand for gold could continue to rise.

Overall, recent action in currency markets has added to gold’s luster as a safe haven. Canada surprised with a cut in interest rates last week along with moves by Denmark, India and the Swiss National Bank shock to currency markets. Mario Draghi is on the warpath for a substantially weaker Euro and as these currencies lose value, gold could continue to become more attractive and continue its recent bullish ways.

Comments

Log in or sign up to join the conversation.