The Fed Blinks On Taper, Bulls Buy The Dip Again

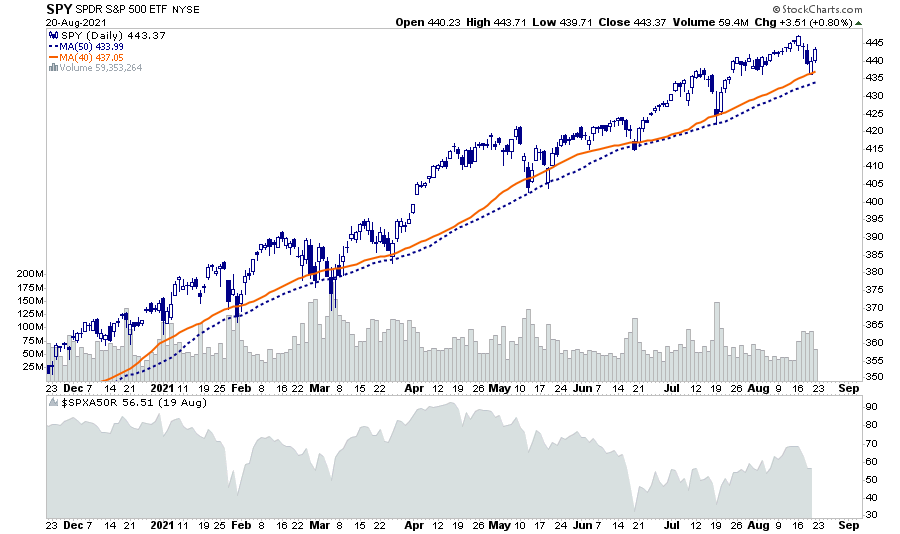

Last week, we discussed that further upside would remain challenging. As noted:

“Not surprisingly, the market didn’t make much headway this past week, given the current extended and overbought conditions. For now, ‘buy signals’ remain intact, which likely limits the downside over the next week. However, a retest of the 50-dma is certainly not out of the question.”

Such was again the case this week as concerns over the Fed tapering their balance sheet spooked investors. However, the Fed trained investors to “buy the dip.” Not surprisingly, they jumped in at the 40-dma to buy rather than waiting for a test of the 50-dma. (Although it was on lower volume and weaker breadth.)

The “buying frenzy” came following a near 2% “crash” in the financial markets forcing the Fed to “blink” on tapering. To wit:

“Dallas Federal Reserve President Robert Kaplan said on Friday he was watching carefully for any economic impact from the Delta variant of the coronavirus and might need to adjust his views on policy “somewhat” should it slow economic growth materially.”

We discuss below why we believe the Fed will still announce plans to taper as early as September.

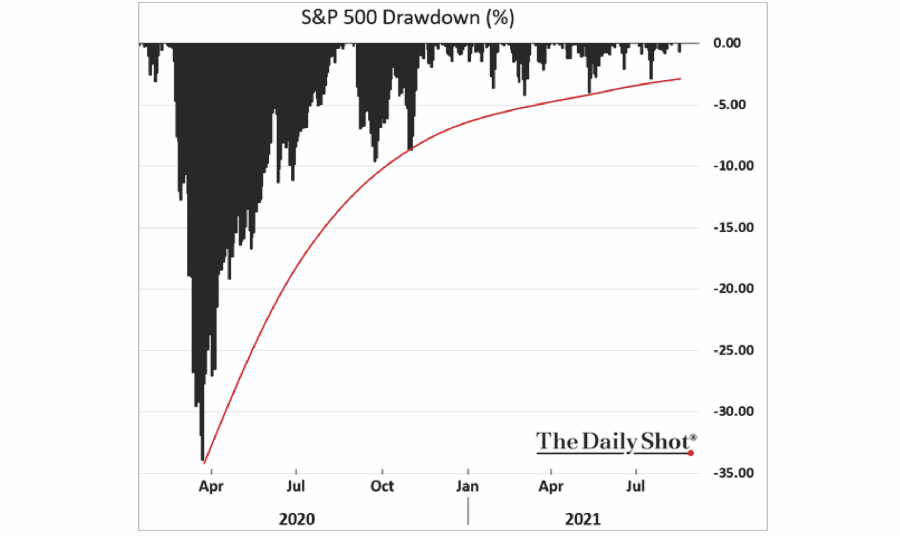

Nonetheless, the bullish bias remains. Since the “shutdown” lows of March, the QE fueled rally has led to increased levels of complacency. With the assumption of “no risk” in the markets, investors buy dips on an ever shallower basis.

We noted the long stretch of the current advance without a 5% correction, a test of the 200-dma, and 6-consecutive positive months.

While such does NOT mean a more significant correction is imminent, it is without question such a correction will happen. It is only a function of catalyst and time.

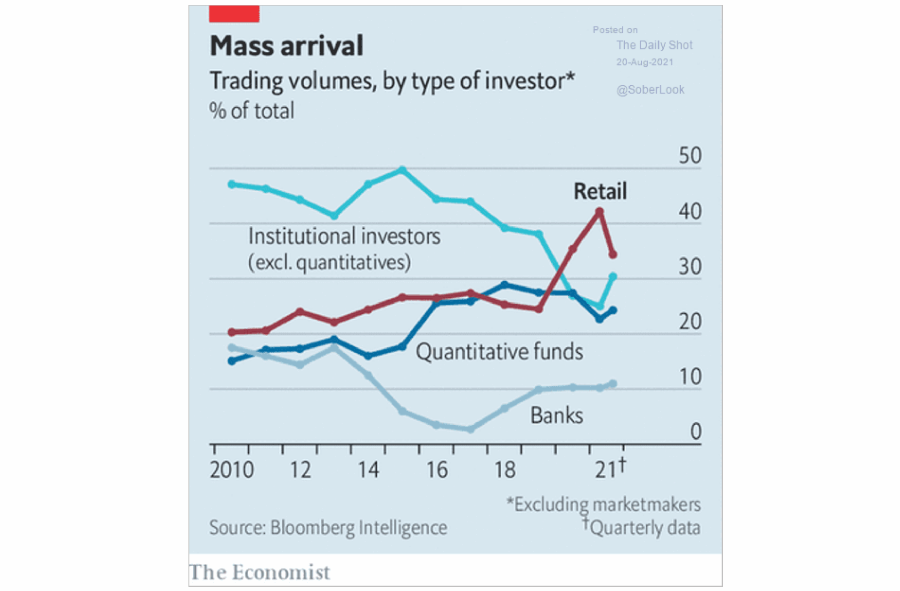

One warning sign is fading speculative interest.

Speculative Fervor Is Fading

Last week, we made some specific notes on the deterioration of market internals. To wit:

“As noted, the market rallied nicely to marginal new highs this past week, but market internals remain relatively weak.”

The basis of our sentiment is mainly due to declining volumes, narrowing breadth, and a decline in speculative activity.

As shown, the speculative surge in the markets, particularly in the “meme” stocks, has evaporated as market action became more muted.

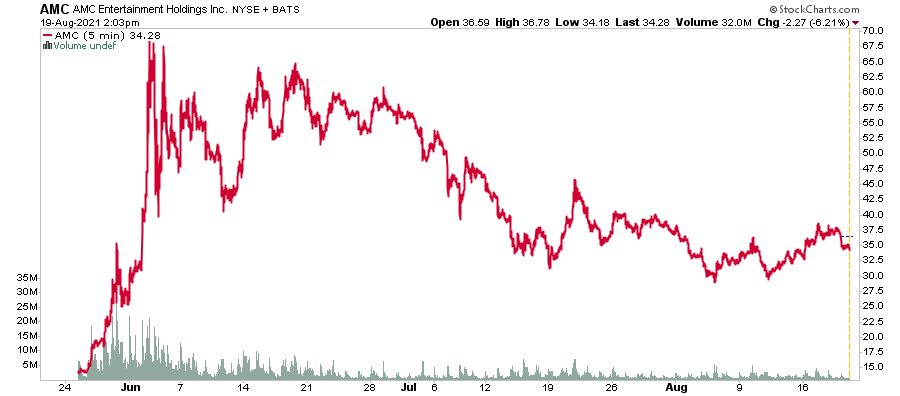

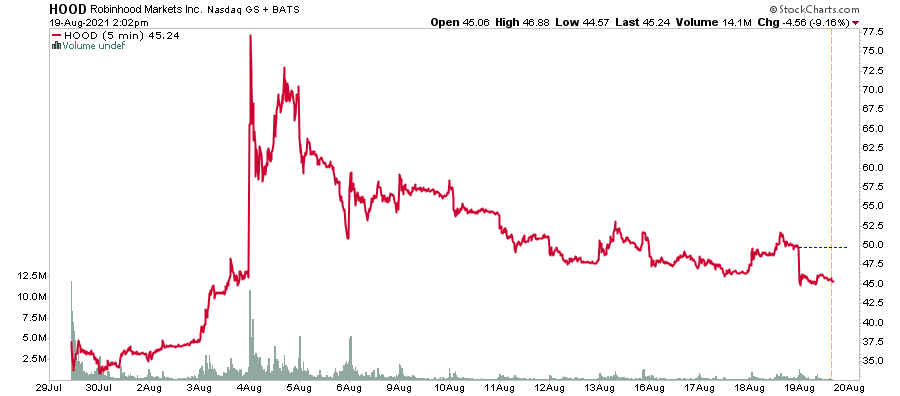

A look at some of the “meme” stock favorites is insightful.

AMC Entertainment (AMC)

Gamestop (GME)

Robinhood Markets

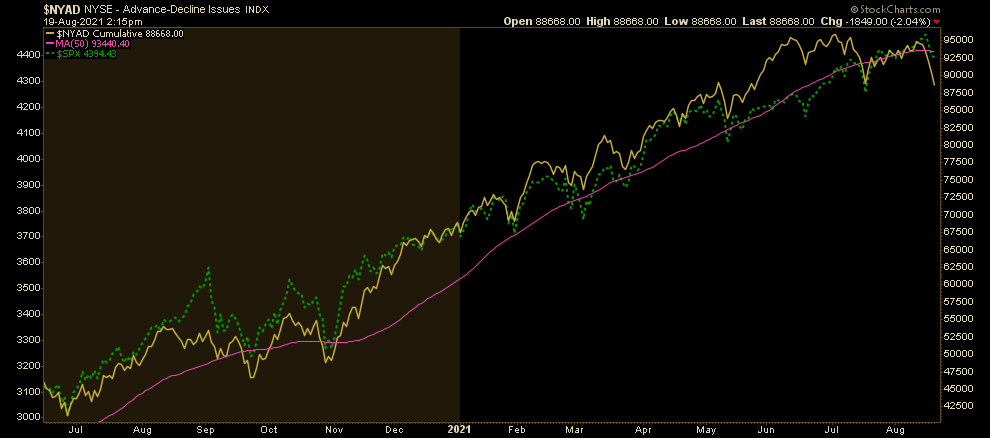

Last week, we also noted that despite a market trading at all-time highs, the number of stocks trading above the 50-dma was feeble. We also see this in the NYSE Advance-Decline line, which broke through the 50-dma this week.

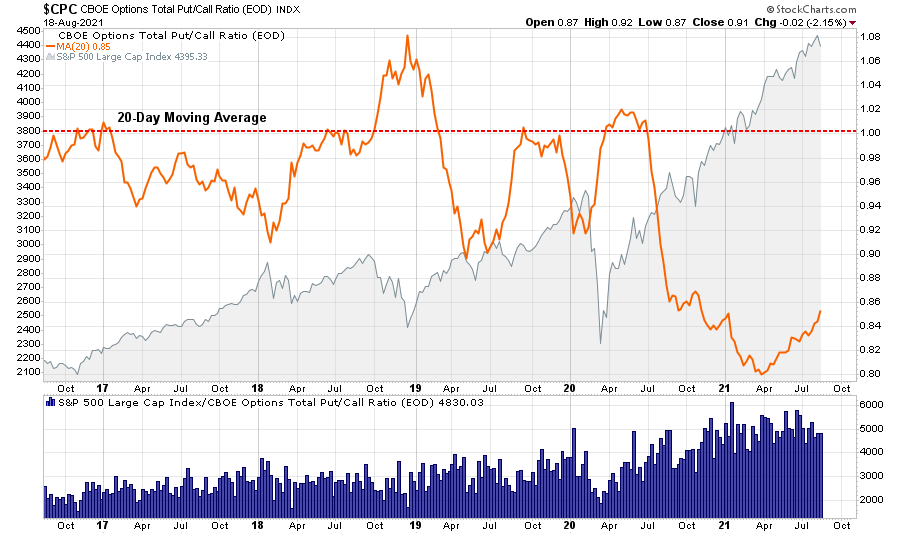

One of the market drivers over the last year was the constant “bid” of retail investors in both the equities and options markets.

Much of this speculation was due to the shift of sports betters into the financial markets. However, with sports betting back, the more muted returns of equities are less exciting. As shown, the put/call ratios have contracted markedly in recent months.

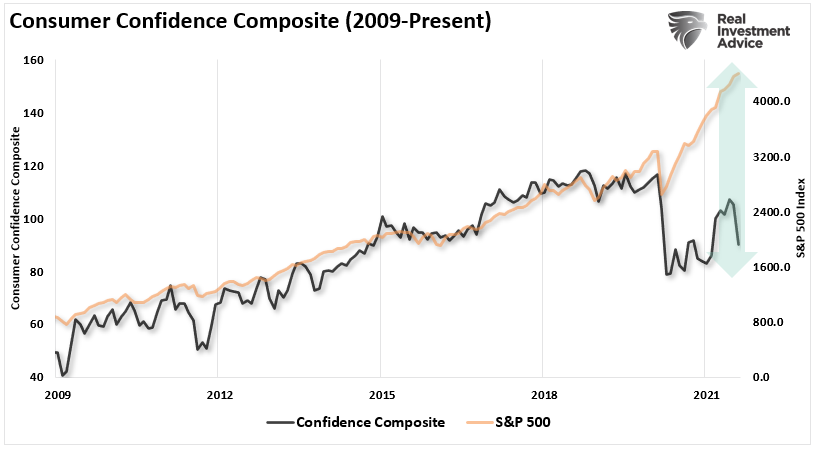

The decline in speculative sentiment also shows up in the collapse in consumer confidence which has a close correlation to markets historically. However, confidence failed to recover despite the Fed inflating a fourth bubble.

The risk to investors remains elevated, but there remains little concern as long as the Fed continues to inject $120 billion a month into the markets.

However, that may be about to change.

Fed Setting The Table For Taper

As noted in our Daily Market Commentary:

“The Fed shed little light in the July FOMC minutes on the schedule of Fed taper. While some Fed members seem eager to start as soon as September, others voiced concern about downward inflation pressures and market perception. We look to the Jackson Hole Fed conference late next week for more guidance.

Highlights from the Fed minutes from the July 28th FOMC meeting.”

- “Most participants noted that, provided that the economy were to evolve broadly as they anticipated, they judged that it could be appropriate to start reducing the pace of asset purchases this year.”

- “They are worried that accelerating plans to wind down the asset purchases could lead investors to question whether the Fed is in a hurry to raise rates or less committed to achieving lower unemployment.”

- SOME PARTICIPANTS REMAINED CONCERNED ABOUT THE MEDIUM-TERM INFLATION FORECAST AND THE PROSPECT OF MAJOR DOWNWARD PRESSURE ON INFLATION RESURFACING.

- “Several others indicated, however, that a reduction in the pace of asset purchases was more likely to become appropriate early next year”

- “Most participants remarked that they saw benefits in reducing the pace of net purchases of Treasury securities and agency MBS proportionally in order to end both sets of purchases at the same time.”

- “The staff provided an update on its assessments of the stability of the financial system and, on balance, characterized the financial vulnerabilities of the U.S. financial system as notable. The staff judged that asset valuation pressures were elevated. In particular, the forward price-to-earnings ratio for the S&P 500 index stood at the upper end of its historical distribution; high-yield corporate bond spreads tightened further and were near the low end of their historical range; and house prices continued to increase rapidly, leaving valuation measures stretched.”

Why Taper Matters

We believe the Fed is setting the table to begin the process of taper sooner than later. Employment is improving, jobless claims are dropping, and inflationary pressures are rising, particularly housing rents. Given their perceived mandates, we suspect they will discuss taper as soon as September.

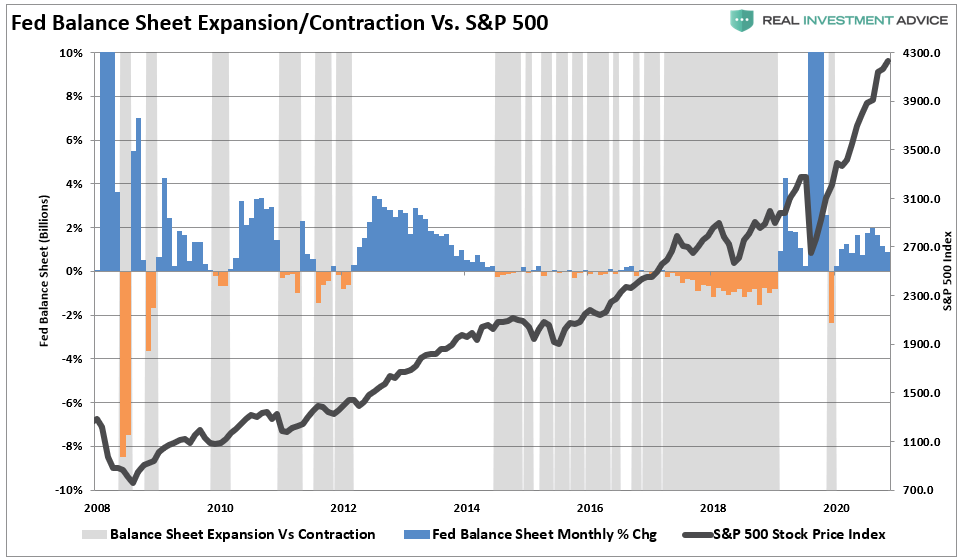

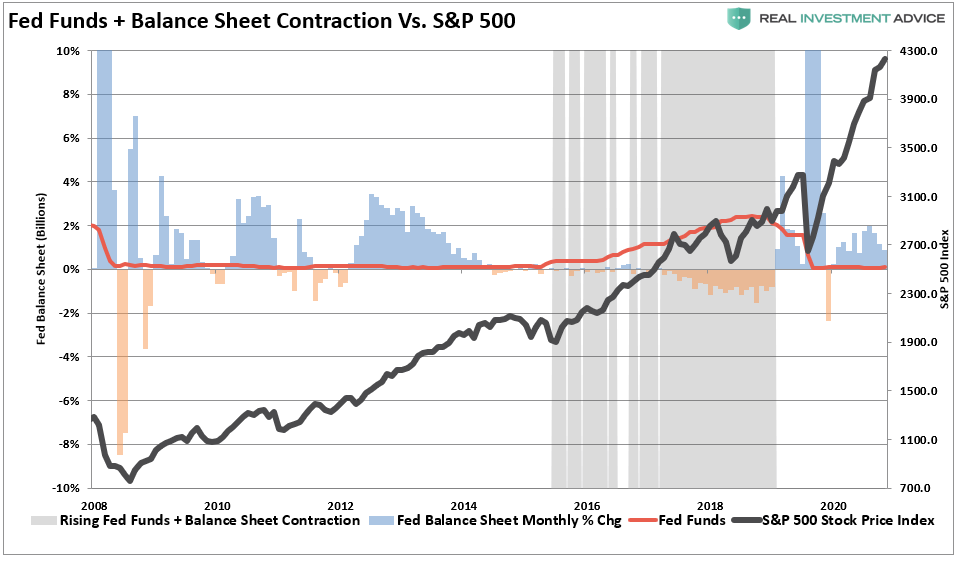

As noted in Fed Talks Taper, there is a not-so-subtle impact on asset prices when the Fed begins to taper assets. So while market participants may be ignoring the Fed short-term, the risk of a “taper” is rising. The grey shaded bars in the chart below show when the balance sheet is either flat or contracting.

That volatility increases markedly when the Fed also hikes rates.

There is a decent probability that with inflationary pressures above target levels and employment improving, the Fed may start tapering sooner than later.

Such is what the bond market is already predicting.

Disclaimer: Click here to read the full disclaimer.

It seems obvious to me that "The Fed" has primarily supporting the short term benefits for the financial sector as a primary goal. Hurting the remaining portion of the population does not seem to be a consideration. But this is not new, ie it?