The Data Is In: Tax Cuts And The Failure To Trickle Down

Back in February, I discussed some of the early indications of what we were seeing following the passage of “tax cut” bill last December. To wit:

“The same is true for the myth that tax cuts lead to higher wages. Again, as with economic growth, there is no evidence that cutting taxes increases wage growth for average Americans. This is particularly the case currently as companies are sourcing every accounting gimmick, share repurchase or productivity increasing enhancement possible to increase profit growth.

Not surprisingly, our guess that corporations would utilize the benefits of ‘tax cuts’ to boost bottom line earnings rather than increase wages has turned out to be true. As noted by Axios, in just the first two months of this year companies have already announced over $173 BILLION in stock buybacks. This is ‘financial engineering gone mad’ and something RIA analyst, Jesse Colombo, noted recently:

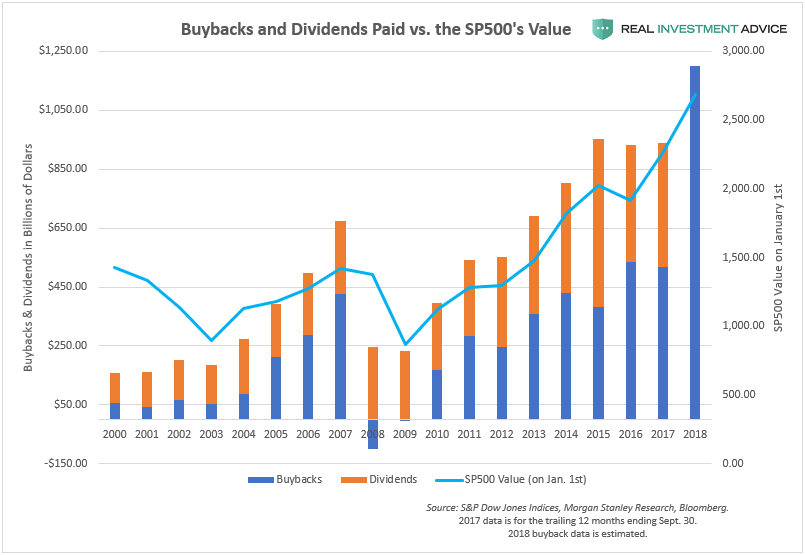

‘How have U.S. corporations been deploying their new influx of capital? Unlike in prior cycles – when corporations favored long-term business investments and expansions – corporations have largely focused on juicing their stock prices via share buybacks, dividends, and mergers & acquisitions. While this pleases shareholders and boosts executive compensation, this short-term approach is detrimental to the long-term success of American corporations. The chart below shows the surge in share buybacks and dividends paid, which is a direct byproduct of the current artificially low interest rate environment. Even more alarming is the fact that share buybacks are expected to exceed $1 trillion this year, which would blow all prior records out of the water. The passing of President Donald Trump’s tax reform plan was the primary catalyst that encouraged corporations to dramatically ramp up their share buyback plans.'”

“What is even more unwise about the current share buyback mania is the fact that it is occurring at extremely high valuations, which is tantamount to ‘throwing good money after bad.’”

And, in the time since that writing, there is scant evidence that wages, or employment, are improving for the masses versus those in the executive “C-suite.”

Nonetheless, while the markets have been rising, investors continue to bank on strong earnings going forward, but should they?

Jamie Powell tackles that question for the Financial Times:

“Zion Research Group, an independent consultancy focused on Accountancy and Tax based in New York City, have combed over last quarter’s earnings- sifting out the organic growth from the accountancy and tax shenanigans. Yet the degree to which it boosted profits may come as a surprise, particularly when broken down by sector.

First off, we should note that Zion Research limited its analysis to 351 of the S&P 500’s constituents, removing businesses whose first quarter did not end on March 31, and only keeping those whose effective tax rate was between 0 to 45 per cent as to, in its words, ‘remove whacky outliers’.

Here are the key findings:

‘On average, it appears as if tax rates dropped by 588 bps from 25.7 per cent in 1Q17 to 19.8 per cent in 1Q18 for the S&P 500 companies analyzed. We estimate that lower tax rates boosted GAAP earnings in the aggregate by 9%.

In the aggregate, we estimate that lower tax rates resulted in about $18.3 billion of incremental net income in 1Q18, accounting for nearly half of the $37.0 billion (17.6%) in year-over-year earnings growth for the 351 companies we analyzed.’

In other words, nearly half of the quarter’s earnings growth came from tax cuts for those selected companies. Furthermore, of the 351 companies analyzed, only 273 got a boost to 1Q18 earnings from lower taxes, while 63 companies had a “tax drag” due to write-downs of deferred tax assets.

More from Zion:

“98 companies [of the 258] relied on taxes for more than half of their earnings growth, including 35 where all the growth was tax related. At the other end of the spectrum, 41 companies actually saw a tax-related drag on earnings growth.”

Buyback Bonanza

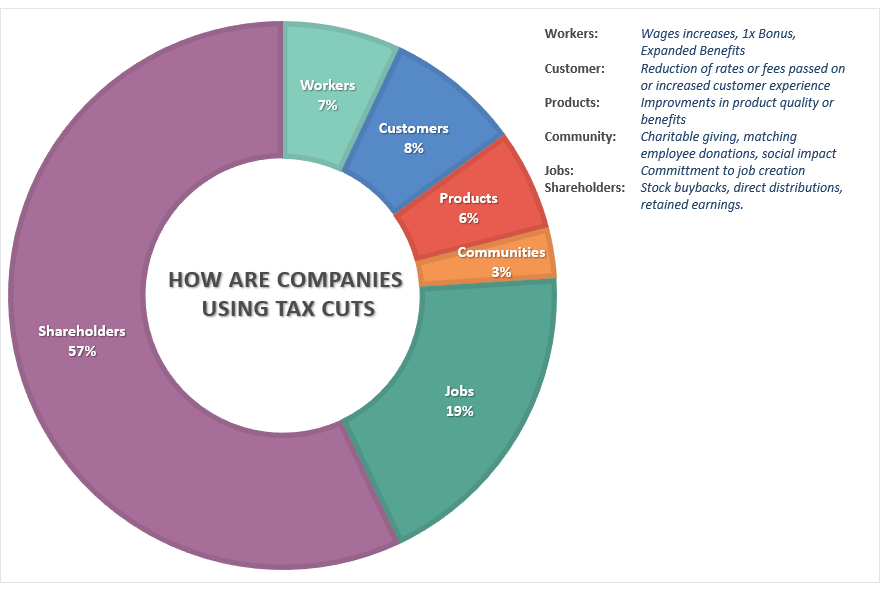

However, there is more to Zion’s story. While earnings growth was indeed derived from tax cuts, it was also the extensive use of buybacks used to boost bottom lines earnings per share that is important. While the mainstream media, and the Administration, rushed to claim that tax cuts would lead to surging economic growth, wages, and employment, such has yet to be the case. Instead, companies have used their tax windfall to buyback shares instead.

As Matt Egan noted for CNN Money:

“Corporate America threw Wall Street a record-shattering party last quarter. Flooded with cash from the Republican tax cut, US public companies announced a whopping $436.6 billion worth of stock buybacks, according to research firm TrimTabs.

Not only is that most ever, it nearly doubles the previous record of $242.1 billion, which was set during the first three months of the year.”

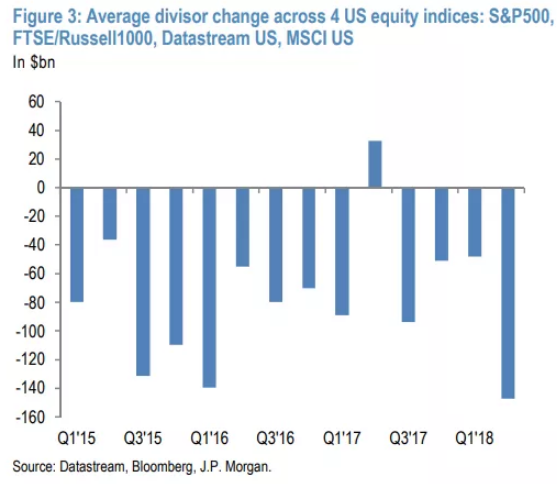

The Heisenberg Report looked at the divisor change in the major indices to confirm the same.

“There’s an argument to be made that if you’re looking to explain how it is that U.S. equities held up in Q2 amid all the headline risk, buybacks are a good place to start. I highlighted the following chart from JPMorgan in a previous post, but I’ll use it again here in the interest of backing up that contention:”

“Normative discussions aside, the corporate bid is in place and that’s a form of real-life ‘plunge protection’. You don’t need any conspiracy theories to employ the ‘plunge protection’ characterization. Recall that back in February, amid the equity rout, Goldman’s buyback desk had its second busiest week in history. Here’s a quote from a note dated February:

‘The Goldman Sachs Corporate Trading Desk recently completed the two most active weeks in its history and the desk’s executions have increased by almost 80% YTD vs. 2017.’

The point here, is that when it comes to the ‘who will be the marginal buyer of U.S. equities?’ question, I’m not entirely sure it needs answering in the near term as long as buybacks continue and as long as earnings continue to come in strong. Additionally, you can expect the buyback bid to be even more pronounced in the event there’s a sell off.”

The “buyback bid” not only supports stock prices in the short-term but as I discussed recently in “Q1-Earnings Review,” there is evidence which suggests the economy is not as fully robust as may appear in headline data.

“Looking back it is interesting to see that much of the rise in ‘profitability’ since the recessionary lows have come from a variety of cost-cutting measures and accounting gimmicks rather than actual increases in top-line revenue. As shown in the chart below, there has been a stunning surge in corporate profitability despite a lack of revenue growth. Since 2009, the reported earnings per share of corporations has increased by a total of 336%. This is the sharpest post-recession rise in reported EPS in history. However, that sharp increase in earnings did not come from revenue which has only increased by a marginal 49% during the same period.”

“Furthermore, while the majority of buybacks have been done with ‘repatriated’ cash, it just goes to show how much cash has been used to boost earnings rather than expanding production, making productive acquisitions or returning cash to shareholders.

Ultimately, the problem with cost-cutting, wage suppression, labor hoarding and stock buybacks, along with a myriad of accounting gimmicks, is that there is a finite limit to their effectiveness. Eventually, you simply run out of people to fire, costs to cut and the ability to reduce labor costs.”

When Does The Party End?

While tax cuts have been and will be, fantastic for bottom line earnings in the first half of this year, the real question becomes who will be the marginal buyer of equities once the “windfall bonanza” for corporations subsides. There are two points of concern which should be considered.

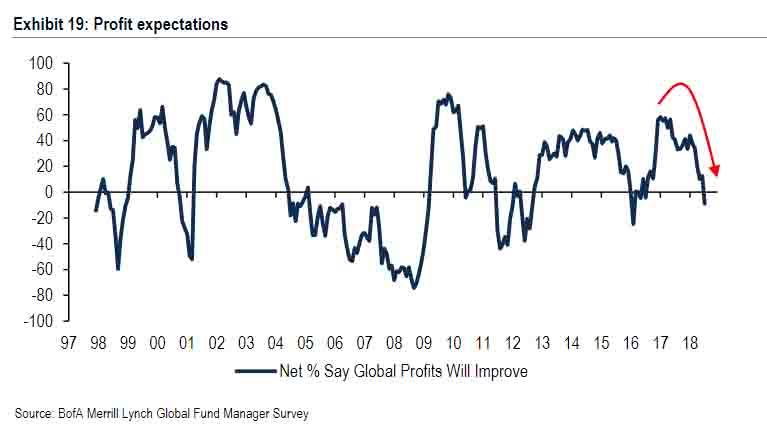

The first is those profit expectations are on the decline already as noted by BofA in a recent report:

“A a net -9% of respondents think global profits will not improve in the next 12 months, down 53ppt from Jan’18 and the lowest since Feb’16. This means that a majority of investors now believe that profits have topped out and will slide in the coming year.“

The second is margin expansion. Going forward increasing margins will become tougher as higher labor costs, rising energy prices, higher interest costs, tariffs and a stronger dollar weigh on bottom line profitability. More importantly, the dramatic surge in earnings growth in the first two quarters will dissipate quickly as year-over-year comparisons become more problematic.

As Eric Parnell recently penned:

“Share buyback activity is currently breaking records, perhaps in unsustainable ways. Eventually, this activity will slow. If history and logic is any guide, it will be when the U.S. economy falls back into recession and corporations need to circle the wagons and keep the cash that might otherwise be allocated to buybacks on their balance sheets instead. And if the forecasters along with the Treasury yield curve that are predicting an economic slowdown as soon as 2019 prove to be correct, this scaling back in buyback activity may be coming sooner rather than later once the tax cut sugar high finally wears off.”

While the key market trends remain decidedly positive for now, and portfolios should remain tilted toward equity exposure, understand that all cycles end. The only questions are “when” and “what causes it?”

As we have repeatedly written since last December, tax cuts were destined to only wind up in one place – in the pockets of shareholders and C-suite executives. But in an economy which is nearly 70% driven by the consumption of the bottom 90%, a fiscal policy which specifically targeted corporations (which are major political donors) was not likely the best strategy to promote a long-term increase in economic prosperity.

Unsurprisingly, with the data now in, we once again come to find out that “trickle down” economics never actually trickles.

Disclosure: The information contained in this article should not be construed as financial or investment advice on any subject matter. Real Investment Advice is expressly disclaims all liability in ...

more