The Bond Rally Was No Surprise

Nathan Vardi recently penned an article for Forbes entitled “Surprise! The Late-Year Bond Rally.”

“In August, Jamie Dimon, CEO of JPMorgan Chase & Co. and the nation’s most prominent banker, predicted the yield on the benchmark 10-year Treasury note could reach 4% in 2018. He cautioned investors to prepare for 5% or higher.

Dimon’s call was not a contrarian one. It had become conventional wisdom on Wall Street that rates were headed higher and that the Federal Reserve would be tightening monetary policy for the foreseeable future.”

Jamie Dimon wasn’t alone. There were many venerable Wall Street veterans from Bill Gross, Paul Tudor Jones, Ray Dalio, and Jeff Gundlach were also calling for higher rates. But, these calls for higher rates and the “End Of The Great Bond Bull Market” have been flowing through the media since 2013.

- Bill Gross Says Bond Bear Market Confirmed

- Have We Entered The Bond Bear Market

- Has The Bond Bear Market Finally Started

- The Bond Bear Is Here

- The 3-Decade Bond Bull Market Is In Danger

And that was just from January.

Of course, those headlines are not the first time we have seen such calls made. One of the biggest problems with predictions of rising 10-year bond yields, since “bond bears” came out in earnest in 2013, is they have been consistently wrong. For a bit of history, you can read some of my previous posts on why rates can’t rise in the current environment.

You get the idea.

But what is it the mainstream analysis continues to miss?

Rates Are Low, So They Must Go Up

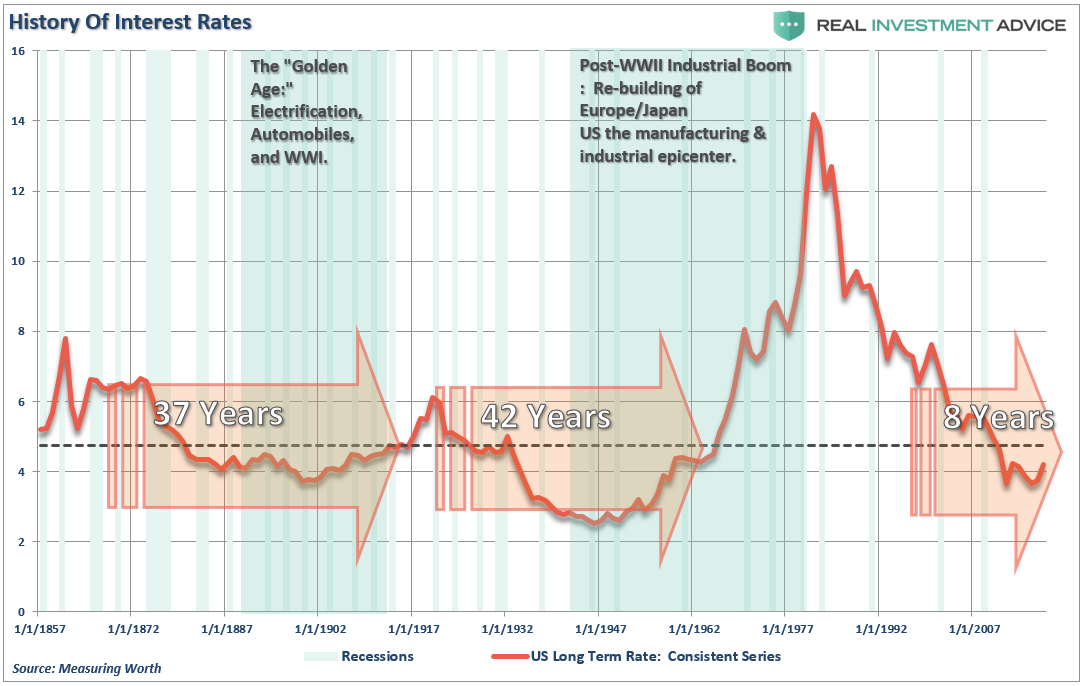

The general view as to why rates must rise is simply because they are so low. Looking at the chart below, such would certainly make sense.

However, it is important to note that interest rates can remain low for a very long time. The two previous occasions where rates fell below the long-term median they remained there for more than 35-years. We are currently about 8-years into the current evolution.

But here is the important point.

Higher interest rates are a function of strong, organic, economic growth that leads to a rising demand for capital over time. There have been two previous periods in history that have had the necessary ingredients to support a rising trend of interest rates over a long period of time. The first was during the turn of the previous century as the country became more accessible via railroads and automobiles, production ramped up for World War I and America began the shift from an agricultural to industrial economy.

The second period occurred post-World War II as America became the “last man standing” as France, England, Russia, Germany, Poland, Japan and others were left devastated. It was here that America found its strongest run of economic growth in its history as the “boys of war” returned home to start rebuilding the countries that they had just destroyed.

It is important to note that interest rates are also a function of inflation. Inflation is a byproduct of money supply. This is the subject of an upcoming article for RIA PRO subscribers but currently it doesn’t appear the Federal Reserve is quite willing, at least not yet, to generate inflation via the printing presses.

The U.S. is no longer the manufacturing powerhouse it once was, and globalization has sent jobs to the cheapest sources of labor. Technological advances continue to reduce the need for human labor and suppress wages as productivity increases. Today, the number of workers between the ages of 16 and 54 participating in the labor force is near the lowest level relative to that age group since the late 70’s. This is a structural and demographic problem that continues to drag on economic growth as nearly 1/4th of the American population is now dependent on some form of governmental assistance.

These are issues are only going to become worse due to long-term demographic trends not only in the U.S., but globally.

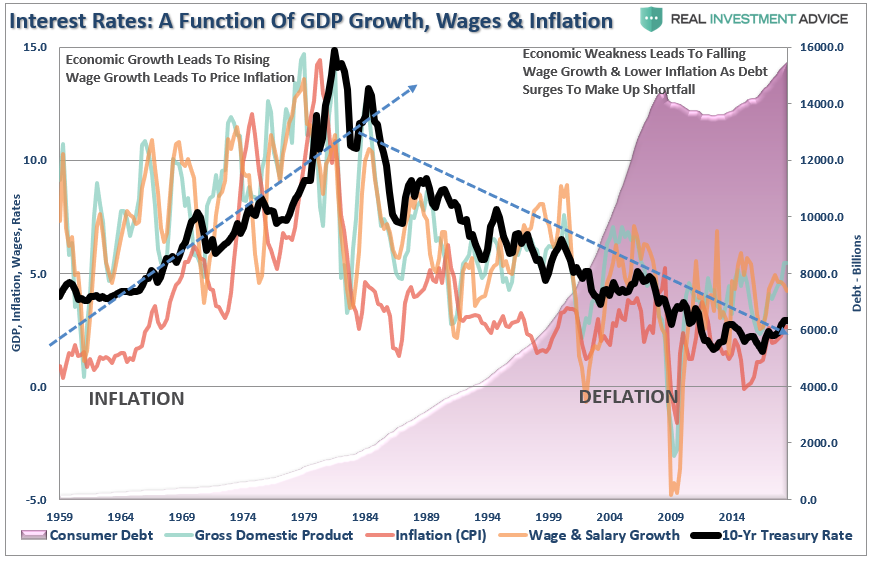

As shown below, the is a correlation between the three major components of the economy (inflation, GDP and wage growth) and the level of interest rates. Interest rates are not just a function of the investment market, but rather the level of “demand” for capital in the economy. When the economy is expanding organically, the demand for capital rises as businesses expand production to meet rising demand. Increased production leads to higher wages which in turn fosters more aggregate demand. As consumption increases, so does the ability for producers to charge higher prices (inflation) and for lenders to increase borrowing costs. (Currently, we do not have the type of inflation that leads to stronger economic growth, just inflation in the costs of living that saps consumer spending – Rent, Insurance, Health Care)

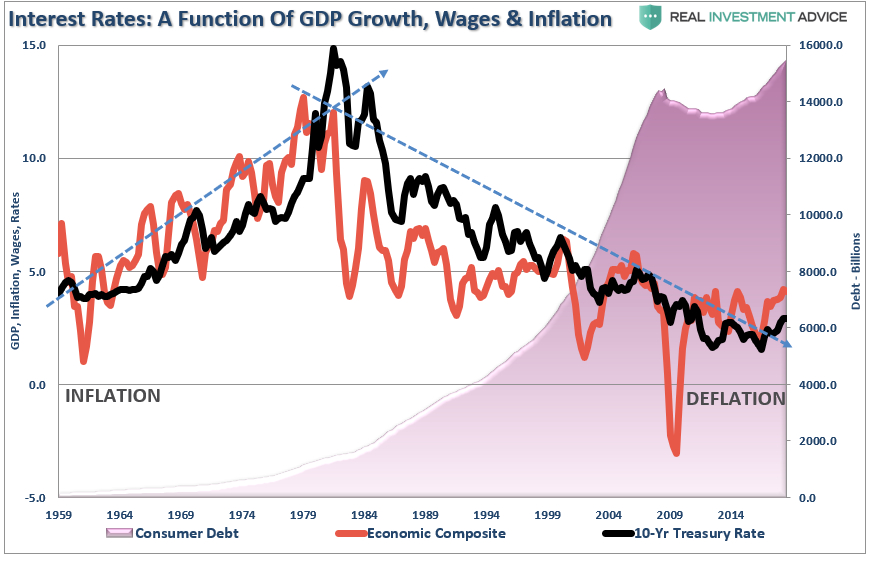

The chart above is a bit busy, but I wanted you to see the trends in the individual subcomponents of the composite index. The chart below shows only the composite index and the 10-year Treasury rate.

Let’s go back to Jamie Dimon for a moment. He stated that interest rates should be 4% which would align with economic growth rates earlier this year. However, that growth was not driven by organic factors of rising wages but rather a confluence of natural disasters. Furthermore, the increase in deficit spending also helped boost economic growth.

The issue is that the surge in deficit spending, combined with the pick up in short-term demand for construction and manufacturing processes, gave the appearance of economic growth which got both the Federal Reserve and the “bond bears” on the wrong side of the trade.

As I have stated previously, the impacts of these “one-off” inputs into the economy will continue to fade as we move into 2019.

While it is certainly hoped that the current economic expansion can last for years to come, a simple look at the last 40 years of fiscal and monetary policy suggests it won’t.

Why?

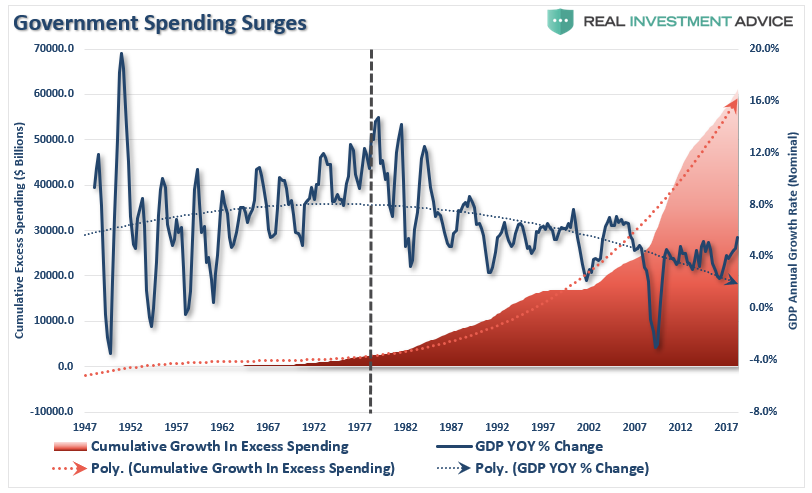

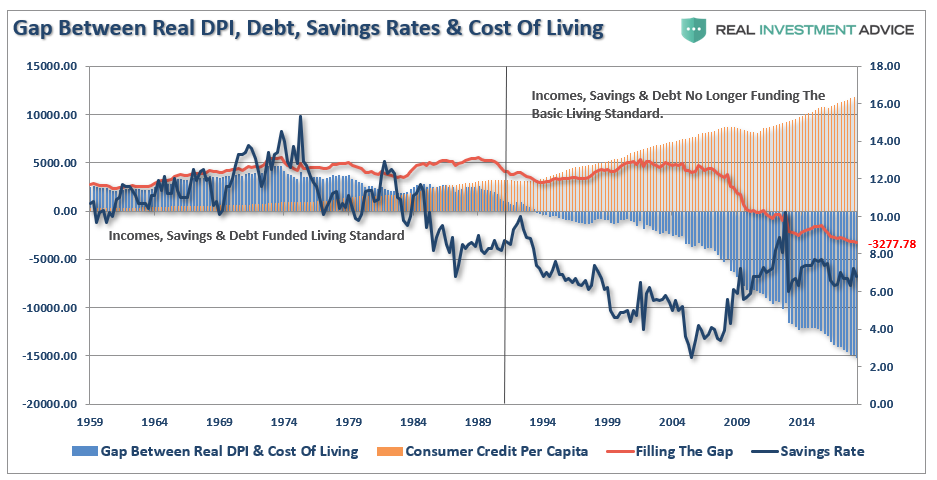

Because you can’t create economic growth when it is financed by deficit spending, credit, and a reduction in savings.

You can create the “illusion” of growth in the short-term, but the surge in debt reduces both productive investments into, and the output from, the economy. As the economy slows, wages fall, and the consumer is forced to take on more leverage and decrease their savings rate. As a result, of the increased leverage, more of their income is needed to service the debt, which requires them to take on more debt.

Which is exactly what has happened.

(The chart below shows the shortfall between the inflation-adjusted cost of living and what wages and savings will cover. The deficit is the difference that has to be made up with debt every year.)

Given that nearly 70% of current economy is driven by consumption, it only requires small moves higher in interest rates before the negative impact to economic growth is realized as capital flows are reduced. (Since interest rates affect payments, higher rates quickly impact consumption, housing, and investment which ultimately deters economic growth.)

The problem with most of the forecasts for the end of the “bond bull” is the assumption we are only talking about the isolated case of a shifting of asset classes between stocks and bonds. However, the issue of rising borrowing costs spreads through the entire financial ecosystem like a virus. The rise and fall of stock prices have very little to do with the average American and their participation in the domestic economy.

Interest rates, however, are an entirely different matter.

The Next Crisis

Just recently, Janet Yellen discussed the issue of leverage in the economy stating that companies are taking on too much debt and could be in trouble should some unexpected trouble hit the economy or markets.

“Corporate indebtedness is now quite high and I think it’s a danger that if there’s something else that causes a downturn, that high levels of corporate leverage could prolong the downturn and lead to lots of bankruptcies in the non-financial corporate sector.”

Yellen also warned that the debt is being held in instruments similar to ones used to bundle subprime mortgages that led to the financial crisis a decade ago. Importantly, the investment-grade part of the bond market was $3.8 trillion at the end of October which was 6% higher than a year ago, and BBB-rated bonds accounted for 58% of the total,

In other words, with rates rising, economic growth slowing (debt is serviced from revenues), and the health of balance sheets deteriorating (BBB is one notch above “junk”) the risk of an “event-driven” crisis is real. All it will take is a significant decline in asset prices to spark a cascade of events that even monetary interventions may be unable to stem. As stock prices decline:

- Consumer confidence falls further eroding economic growth

- The $4 Trillion pension problem is rapidly exposed which will require significant government bailouts.

- When prices decline enough, margin calls are triggered which creates a liquidation cascade.

- As prices fall, investors and consumers both contract further pushing the economy further into recession.

- Aging baby-boomers, which are vastly under-saved will become primarily dependent on social welfare which erodes long-term economic growth rates.

With the Fed tightening monetary policy, and an errant Administration fighting a battle it can’t win, the timing of the next recession has likely been advanced by several months.

The real crisis comes when there is a “run on pensions.” With a large number of pensioners already eligible for their pension, the next decline in the markets will likely spur the “fear” that benefits will be lost entirely. The combined run on the system, which is grossly underfunded, at a time when asset prices are dropping will cause a debacle of mass proportions. It will require a massive government bailout to resolve it.

But it doesn’t end there. Consumers are once again heavily leveraged with sub-prime auto loans, mortgages, and student debt. When the recession hits, the reduction in employment will further damage what remains of personal savings and consumption ability. The downturn will increase the strain on an already burdened government welfare system as an insufficient number of individuals paying into the scheme is being absorbed by a swelling pool of aging baby-boomers now forced to draw on it. Yes, more Government funding will be required to solve that problem as well.

As debts and deficits swell in the coming years, the negative impact to economic growth will continue. At some point, there will be a realization of the real crisis. It isn’t a crash in the financial markets that is the real problem, but the ongoing structural shift in the economy that is depressing the living standards of the average American family.There has indeed been a redistribution of wealth in America since the turn of the century. Unfortunately, it has been in the wrong direction as the U.S. has created its own class of royalty and serfdom.

But most importantly, that is how interest rates remain low for a very long-time.

While there is little left for interest rates to fall in the current environment, there is no ability for rates to rise before you push the economy back into recession. Of course, you don’t have to look much further than Japan for a clear example of what I mean.

The “bond rally” was no surprise.

Disclosure: The information contained in this article should not be construed as financial or investment advice on any subject matter. Real Investment Advice is expressly disclaims all liability ...

more

Well thought out. Weak labor is a major problem in the USA but also so is the massive demand for bonds for use as collateral. Studies have shown that demand does impact yields.