Technically Speaking: Predictions, Market Bounce & Risks

I love trolls.

One of my favorite things to do is read the comments from readers. Most of the comments are generally insightful, well-intentioned, contribute to the community and inspire thought particularly when they disagree with my own views.

Then, there are the “trolls.”

“Trolls” are anonymous posters who have nothing better to do with their lives than try to degrade the dialog, and the intellectual commentary and community, by posting diatribe which shows their own lack of intellect, experience and, human decency.

Generally, I don’t waste my time responding to them but a comment to last weekend’s newsletter showed a clear lack of understanding about portfolio management and the investing process as whole. (Notice the anonymous handle)

“5731311 – Every week I want to write an article crying wolf calling for a market crash, but actually stay fully invested. Then I will also offer 3 mutually exclusive scenarios for the near term. Then next week, I will say – see, I told you so, I was right on one of my predictions. I’m a genius.”

First, I have the “cojones” to analyze, write and publish on a very regular basis. “Trolls” hide behind anonymity as they don’t have the backbone to publish their own views and open themselves up for public scrutiny.

Secondly, if you actually read my articles you will already know that I have not been calling “for”a market crash, but rather pointing out that one is inevitable since such is part of the “boom/bust” cycle of the markets.

Lastly, yes, I absolutely offered 3-potential outcomes for the near term in this past weekend’s missive, to wit:

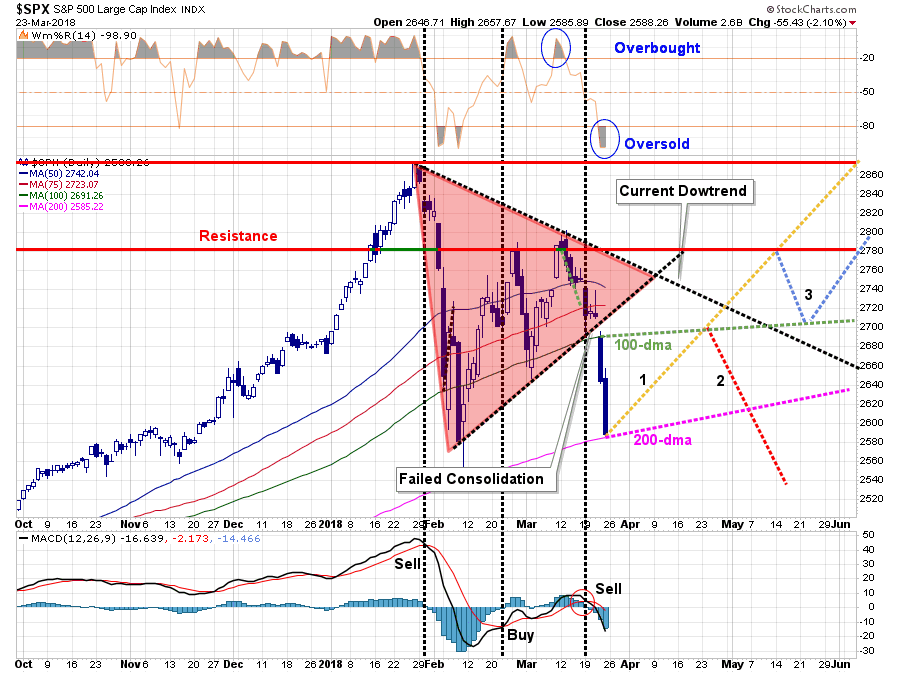

“Considering all those factors, I begin to layout the “possible” paths the market could take from here. I quickly ran into the problem of there being “too many” potential paths the market could take to make a legible chart for discussion purposes. However, the bulk of the paths took some form of the three I have listed below.”

- Option 1: The market regains its bullish underpinnings, the correction concludes and the next leg of the current bull market cycle continues. It will not be a straight line higher of course, but the overall trajectory will be a pattern of rising bottoms as upper resistance levels are met and breached. (20%)

- Option 2: The market, given the current oversold condition, provides for a reflexive bounce to the 100-dma and fails. This is where the majority of the possible paths open up. (50%)

- The market fails at the 100-dma and then resumes the current path of decline violating the current bullish trend and officially starting the next bear market cycle. (40%)

- The market fails at the 100-dma but maintains support at the 200-dma and begins to build a base of support to move higher. (Option 1 or 3) (20%)

- The market fails at the 100-dma, finds support at the 200-dma, makes another rally attempt higher and then fails again resuming the current bearish path lower. (40%)

- Option 3: The market struggles higher to the previous “double top” set in February, retraces back to the 100-dma and then moves higher. (30%)

Why all the options? Why not just draw a straight line down to zero, or up to 1 million, depending on your relative bullishness or bearishness?

Because that is not how portfolio management works.

The Best Forecasters On The Planet

A couple of years ago there was a study of a variety of forecasters – economists, financial experts, psychics, meteorologists, etc. The goal of the study was to determine the accuracy of forecasts that were given.

It turned out that meteorologists were the most accurate forecasters of the future.

How far into the future could the accurately forecast? 3-days.

“Even Punxsutawney Phil currently has an arrest warrant issued because ‘cold weather’ lasted longer than the six-weeks his shadow forecasted.”

So, for the “reading impaired,” or just the “investment illiterate,” it should already be readily apparent that no one can accurately predict the markets weeks, or months, in advance.

That is also not my job. Or yours.

In virtually every professional field there is “risk.”

In any given profession, those who fail to focus on, and recognize, the inherent risk, more commonly known as ” being reckless,” tend not to be around very long. What has always separated the “winners” from “losers,” are those that can avoid the catastrophic damage over time.

Think about Tom Brady who is one of the greatest NFL quarterbacks to ever play the sport. Yes, he is indeed extremely skilled and talented, however, if he is injured he can not play. Therefore, he has become quite famous over the last couple of years with respect to his personal training and nutrition regimen. He controls, to the best of his ability, the “risk” of injury by focusing on the things he CAN control – his health and fitness.

The control of “risk: is also the very essence of portfolio management.

My job, as a portfolio manager, is simply to take all of the relevant data at my disposable and begin to weigh possibilities and probabilities about potential future outcomes. Without such a thought process, how can determinations on allocations, exposure, controls, etc. be made?

For investors, understanding risk is an important concept as it is a function of “loss”. The more risk that is taken within a portfolio, the greater the destruction of capital will be when reversions occur.

When investors lose money in the market it is possible to regain the lost principal given enough time, however, what can never be recovered is the lost “time” between today and the required financial goal. In other words, the destruction of “time” is a permanent impairment to the portfolio.

Making absolute predictions about the future, bullish or bearish, is not only useless, but inherently dangerous with respect to portfolio management. What can do is make educated “guesses” about potential outcomes based on history, statistics, trends, etc. in order to better control risk in portfolios and avoid permanent impairment of capital.

Decisions To Make

In the newsletter I stated:

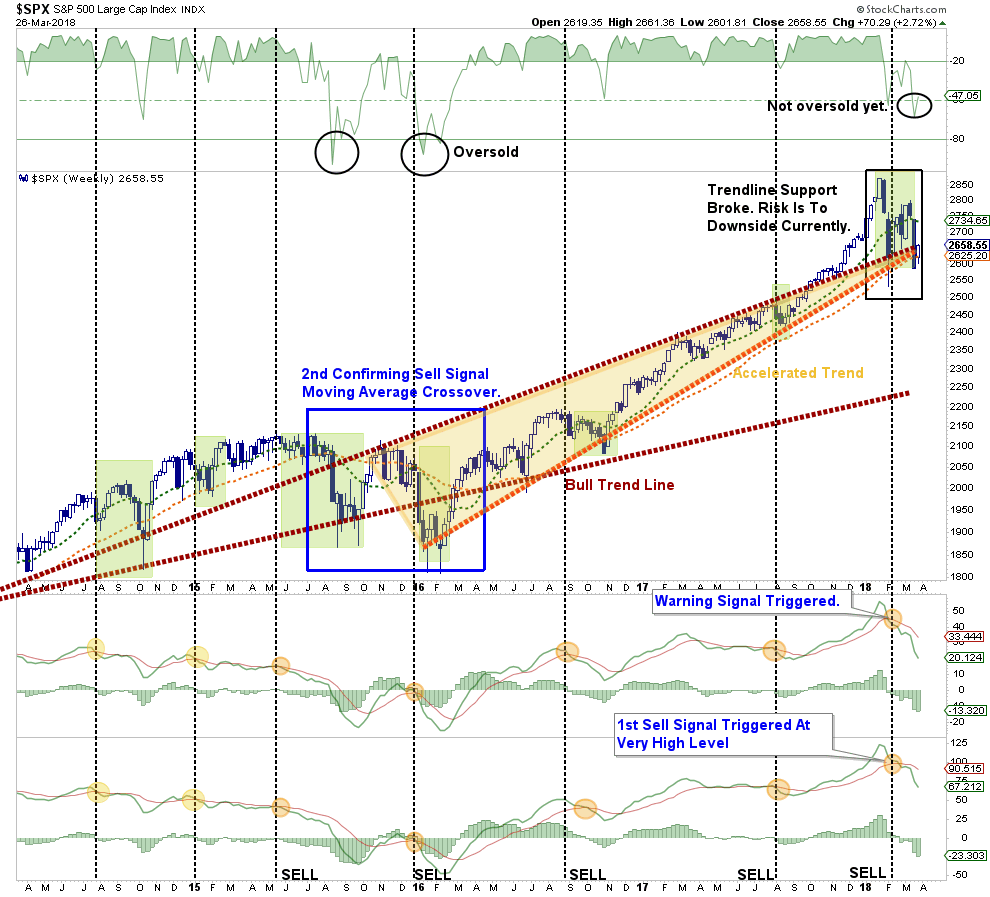

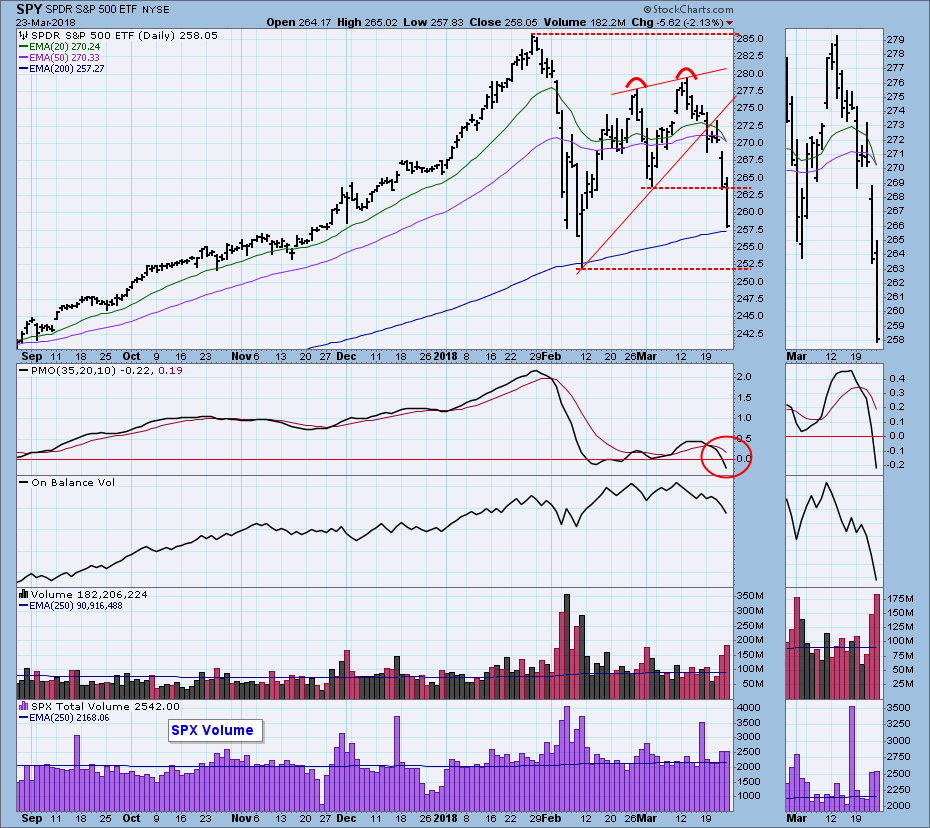

“As I noted above, the market is 2-standard deviations oversold and testing the 200-dma on a very short-term basis. This is not surprising, as by the time ‘sell signals’ are triggered on a weekly basis, the market is generally ‘oversold’ enough to elicit a ‘reflexive’ bounce.“

On Monday, the market did indeed bounce off of the 200-dma. However, that bounce does not change our stated objectives for rebalancing portfolios currently.

Currently, the market remains below the accelerated and bullish trend lines confirming both sets of “sell” signals currently registered.

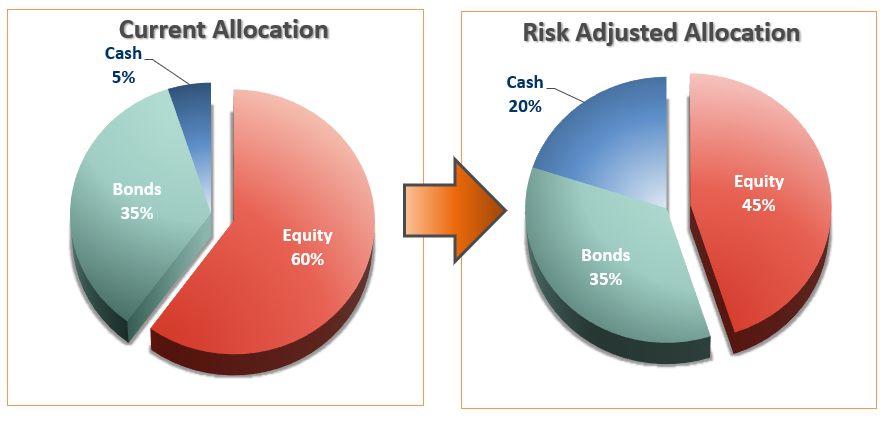

“This week, the markets broke on several fronts which have triggered confirmed ‘sell signals’ on several levels requiring a reduction in equity risk exposure. In accordance with the model adjustments above, begin reducing portfolio equity weighting by 25% on any failed rally attempts.”

“IMPORTANTLY – this does NOT mean go ‘sell’ everything Monday morning. As noted above in the main analysis, we are slightly reducing equity exposure on a rally to hedge risks of a further decline until the current volatility phase passes.

Importantly, as always, portfolio management is about making SMALL adjustments as evidence presents itself and should never be perceived as an ‘all or nothing’ issue. “

Read that last part again.

With the market oversold, we are looking for a rally to the 100-dma to further rebalance portfolio risks. (We have been doing this already over the last several weeks and have been underweight equity and overweight cash.)

However, my guess is we are not likely done with this correctionary process as of yet.

That “feeling” was confirmed by the recent analysis from Decision Point:

“I am assuming that we are in a bear market. Not all of the technical signs have been triggered, but market behavior has me convinced. I want to emphasize that the parabolic advance and breakdown in January/February was the first and most convincing event pushing me into the bear camp. Now the IT Trend Model for SPY has changed from BUY to NEUTRAL (soft SELL), and price action is uninspiring, to say the least.“

(A NEUTRAL signal is a ‘soft’ SELL signal because the position is cash or fully hedged, not short.)

“Obviously, the market is in the process of retesting the February lows. I can make a case for price finding support on the 200EMA and the bull market rising trend line, but, if I’m right about the bear market, that support won’t hold for long, if at all.”

Changing Facts

As I stated, portfolio management is about making small adjustments over time to “react” to what the market is doing.

So, what if I’m wrong?

What if the market just rockets immediately higher and reverses the current “sell signals?”

Well, then we simply invest capital back into the equity markets and take allocations back up to 100% of target.

What if the market breaks below the 200-dma?

Then we will reduce allocations further.

It’s not complicated.

It’s just a process.

There is an extremely high probability the market will not trace out any of my options listed above. But, as Nobel laureate, Dr. Paul Samuelson, once quipped:

“Well, when events change, I change my mind. What do you do?”

Our job as investors is to navigate the waters within which we currently sail, not the waters we think we will sail in later. Greater returns are generated from the management of “risks” rather than the attempt to create returns by chasing markets. That philosophy was well defined by Robert Rubin, former Secretary of the Treasury when he said;

“As I think back over the years, I have been guided by four principles for decision making. First, the only certainty is that there is no certainty. Second, every decision, as a consequence, is a matter of weighing probabilities. Third, despite uncertainty, we must decide and we must act. And lastly, we need to judge decisions not only on the results, but on how they were made.

Most people are in denial about uncertainty. They assume they’re lucky, and that the unpredictable can be reliably forecast. This keeps business brisk for palm readers, psychics, and stockbrokers, but it’s a terrible way to deal with uncertainty. If there are no absolutes, then all decisions become matters of judging the probability of different outcomes, and the costs and benefits of each. Then, on that basis, you can make a good decision.”

It should be obvious that an honest assessment of uncertainty leads to better decisions, but the benefits of Rubin’s approach, and mine, goes beyond that. For starters, although it may seem contradictory, embracing uncertainty reduces risk while denial increases it. Another benefit of acknowledged uncertainty is it keeps you honest.

“A healthy respect for uncertainty and focus on probability drives you never to be satisfied with your conclusions. It keeps you moving forward to seek out more information, to question conventional thinking and to continually refine your judgments and understanding that difference between certainty and likelihood can make all the difference.”

We must be able to recognize, and be responsive to, changes in underlying market dynamics if they change for the worse and be aware of the risks that are inherent in portfolio allocation models. The reality is that we can’t control outcomes. The most we can do is influence the probability of certain outcomes which is why the day to day management of risks and investing based on probabilities, rather than possibilities, is important not only to capital preservation but to investment success over time.

As I have stated before, as a portfolio manager, I am neither bullish or bearish. I simply view the world through the lens of statistics and probabilities. My job is to manage the inherent risk to investment capital. If I protect the investment capital in the short term – the long-term capital appreciation will take of itself.

For those that wish to remain “reading impaired,” there is always “hope” as an investment strategy.

Disclosure: The information contained in this article should not be construed as financial or investment advice on any subject matter. Real Investment Advice is expressly disclaims all liability in ...

more